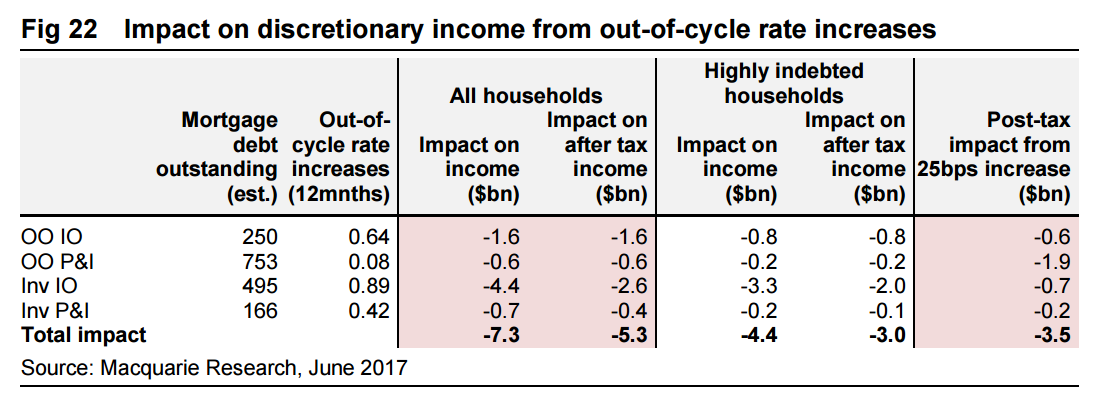

We estimate that out-of-cycle interest rate hikes announced over the last 12 months reduced overall households’ incomes by ~$5bn. Furthermore a gradual shift from IO to P&I would take off additional $5-10bn from discretionary incomes or savings. However, given the distribution of debt, we estimate that ~60% of the reduction in discretionary incomes will be absorbed by the 10% of most indebted households, leaving ~90% of households relatively unaffected. We also note that cash rate reduction in August last year provided ~$3.5bn offset to households income.

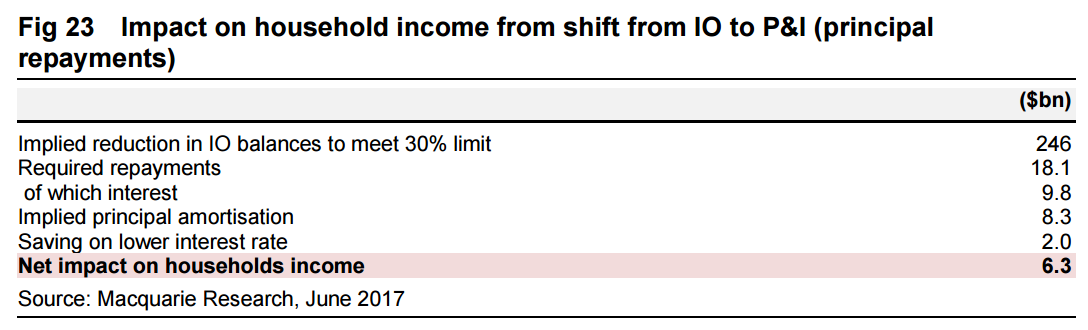

As the figure below highlights, we estimate that as banks rebase their IO flow to ~30% and ultimately outstanding balances also trend to ~30%, increased principal repayments would take off additional ~$6bn from discretionary incomes or savings. We note that historically P&I repayments exceed minimum requirements across the portfolio and we expect the actual impact on households’ income to be larger than the estimate below (ie. $5-10bn). While the full impact of this is likely to take 3-5 years to fully flow through, we note that it is likely to be skewed to earlier years as customers (who can afford this) actively switch to P&I and capitalise on a lower interest rate.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.