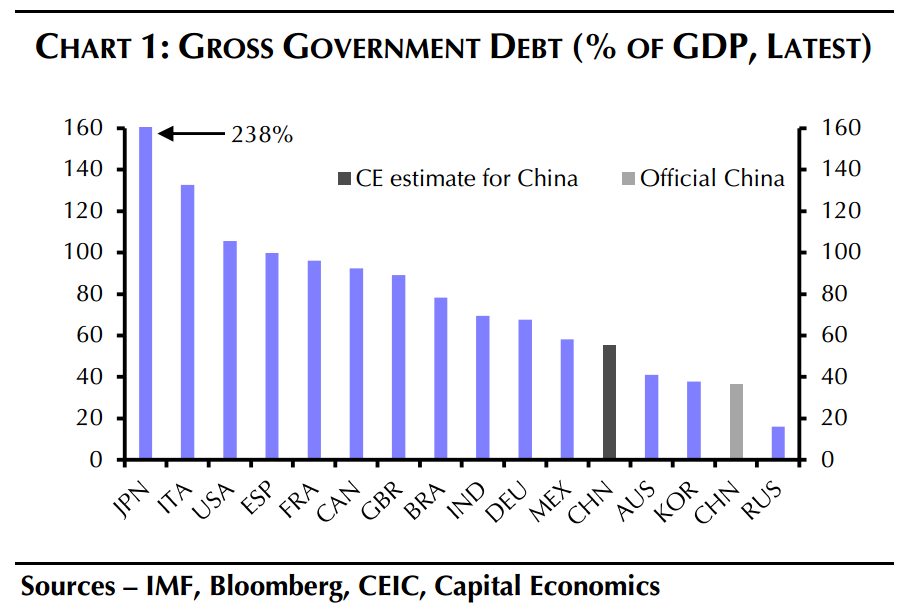

Efforts to curtail off-budget borrowing by local governments have recently helped slow the rise of China’s public debt ratio. But a further rise in government debt is almost certain in future as it eventually foots the bill for the still-rising bad debts of state-owned firms. When Moody’s cut China’s sovereign credit rating last month, the Ministry of Finance (MoF) was quick to point out that, at 36.7% of GDP at end- 2016, China’s public debt remains low by global standards. For our part, we think the public debt ratio is more like 55% of GDP after adding in the contingent liabilities of local governments. Nonetheless, even this is lower than in most other major economies. (See Chart 1.)

While it is true that China’s government debt ratio is still low, it has nonetheless risen by over 20% of GDP since the Global Financial Crisis. Concerns over this rapid increase, which was mostly driven by off-budget borrowing via local government financing vehicles (LGFVs), have prompted policymakers to take steps to restrict government borrowing in recent years.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.