The PMI climbed back into positive territory in June, with firms noting slightly stronger increases in production and new orders. This prompted companies to increase their purchasing activity, albeit only slightly.

However, relatively muted client demand overall led manufacturers to reduce their inventory holdings and trim their workforce numbers again. At the same time, optimism towards the business outlook edged down to its lowest level in 2017 to date. After declining in the previous month, both input costs and output charges increased at the end of the second quarter.

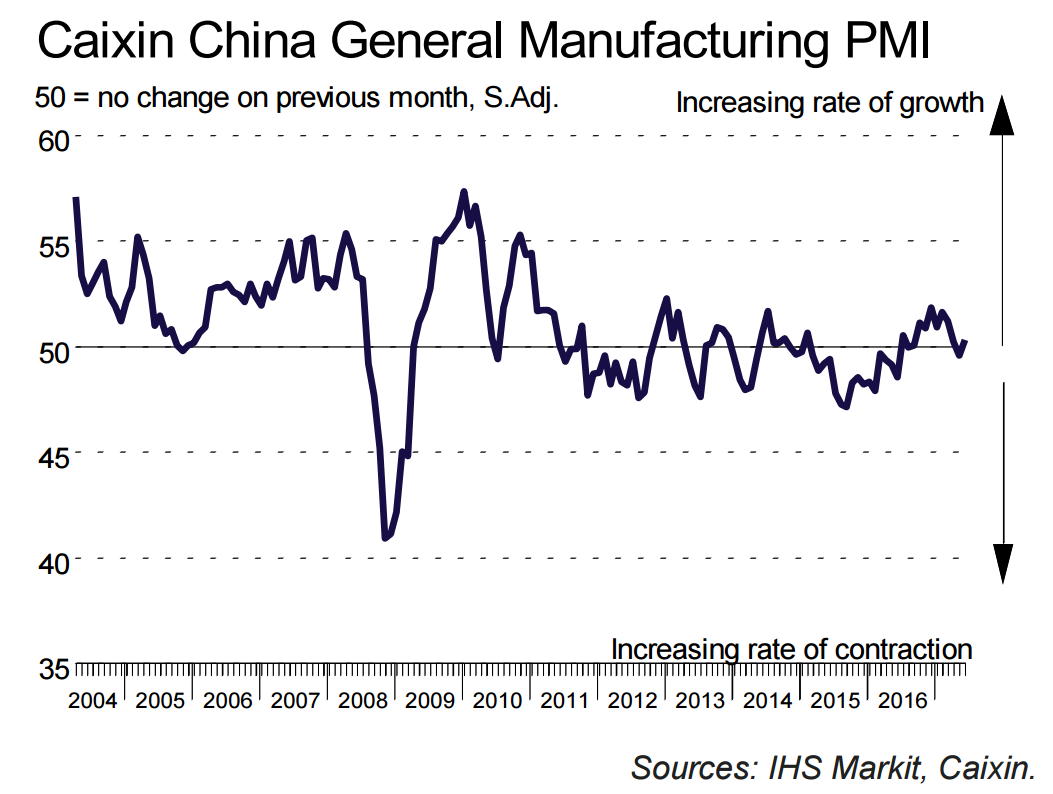

That said, the rates of inflation were much slower than seen at the beginning of the year. At 50.4 in June, the seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – moved back above the 50.0 no-change mark. This was up from 49.6 and signalled an improvement in the health of the sector after a marginal deterioration in May.

Operating conditions have now strengthened in nine of the ten past months, though the latest improvement was only slight. Helping to lift the headline PMI was faster growth in new order books. Though only marginal, the latest increase in new orders was the quickest seen for three months.

New work from overseas also rose only slightly in June, as panellists noted relatively subdued demand both in domestic and international markets. As a result, production rose at a slightly faster (albeit still marginal) pace at the end of the second quarter. Relatively subdued customer demand also weighed on optimism towards the 12-month business outlook, with confidence edging down to a six-month low in June.

Efforts to cut costs and boost efficiency were partly behind a further fall in staff numbers in June. That said, the rate of job shedding eased to a modest pace that was the weakest since March. Subsequently, firms signalled further strain on operating capacity, as highlighted by a sustained increase in backlogs of work. The rate of accumulation softened slightly since the previous month and was moderate overall. After a decline in May, purchasing activity undertaken by manufacturers in China increased slightly at the end of the second quarter.

However, companies adopted relatively cautious attitudes towards their inventories, with both stocks of inputs and finished items declining in the latest survey period. The time taken for inputs to be delivered continued to lengthen in June. Though only slight, the rate of deterioration was the fastest seen for four months. Average input costs faced by Chinese manufacturers increased during June, following a slight reduction in May. According to panellists, greater cost burdens largely reflected higher raw material prices. The rate of increase was modest, however, and much weaker than January’s recent peak. Output charges followed a similar trend, and rose slightly after a decline in the previous month.

Probably the worst result for the bulks short squeeze. Banana Man can hope for neither better growth nor liquidity…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.