Debate over the optimal level of competition to manage Australia’s hundreds-of-billions in default superannuation savings has been raging for years.

This debate has centered around evidence of superannuation funds gouging members with excessive fees, estimated at more than $20 billion a year.

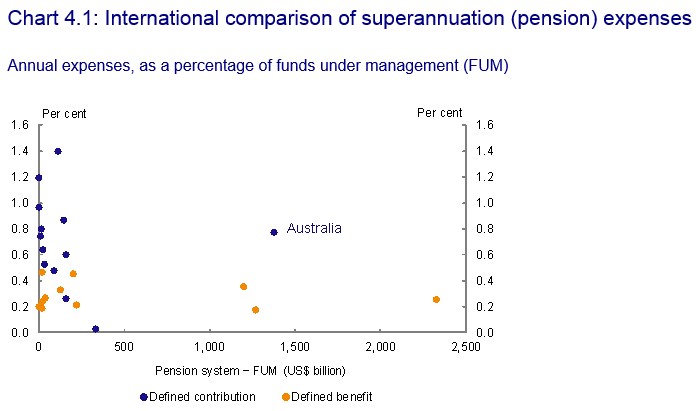

In 2014, the Murray Financial System Inquiry showed that the operating costs of Australia’s superannuation funds are among the highest in the world:

Advertisement

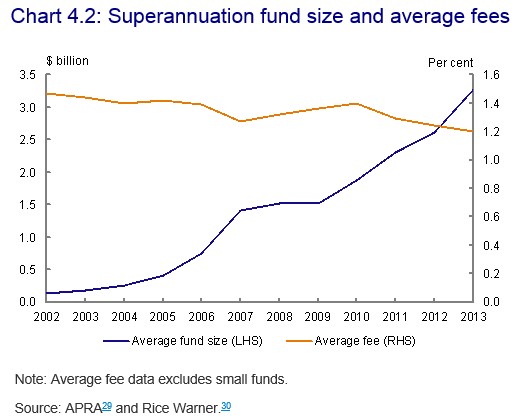

And that fees had not fallen in line with what could have been expected given the substantial increase in scale, which will dramatically reduce consumer’s retirement nest eggs:

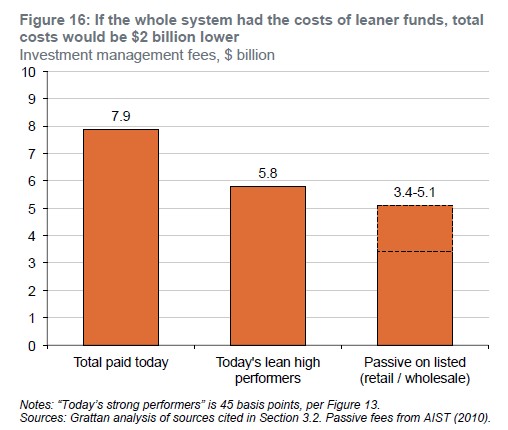

Then in 2015, the Grattan Institute released a report, entitled Super Savings, which argued that excessive fees are reducing retirement nest eggs by some $40,000. Grattan also recommended the Government reduce fees by running a tender to select superannuation funds to manage the accounts of the nine million Australians who choose a default fund through their employer:

Advertisement

Running a tender to select these funds would save $1 billion a year in fees, or $40,000 for each account holder…

“There are too many accounts, too many funds, and too many of them incur high costs,” says Grattan’s Productivity Growth Program Director, Jim Minifie.

“Australia has many high-performing but lean funds. If other funds charged what they charge, account holders could get the same performance, but pay $4 billion a year less in administration and $2 billion less in investment management,” he says.

“These are numbers big enough to make the difference between sausages and steak in retirement.”

“A stronger and fairer superannuation system will take the pressure off government pension payments and give older Australians confidence in the future.”

The Productivity Commission (PC) has since suggested limiting the number choices of default funds that would be offered to consumers from 110 to between four and 10, depending on how the system was devised.

Not surprisingly, the superannuation sector has pushed-back hard, calling for the sector to be opened-up to more competition, arguing that this would both spur innovation and could even lower member fees by $300 million a year.

Advertisement

However, this call for more competition has been rebuffed by Nicholas Barr, the professor of public economics at the London School of Economics, who today argues that allowing more competition would merely increase complexity in the system. From The AFR:

Professor Barr said that competition was appropriate in the case of products and services that were readily understood, such as mobile phones and clothing, and where the costs of making the wrong decision were low.

This, he said, was not the case with complex financial services products.

“Most people can’t make an informed decision or don’t have the time to,” Professor Barr said on the sidelines of the Annual Colloquium of Superannuation Researchers in Sydney. “The more complex the financial product, the less people understand and the less likely people are to make choices in their own best interest. Choice should be optimised, not maximised. This is an argument that gets overlooked or over-ridden for ideological reasons.

“This is not an ideological argument. It is a technical argument. Superannuation should be to secure an income in old age for all Australians. How you do it should be technical.”

The economist recommended the government limit the number of comprehensive retirement products that are expected to be offered to super fund members to try to ensure they do not outlive their savings.

Unfortunately, the high cost of Australian superannuation has a lot to do with it being compulsory, which has provided the industry with a “sheltered workshop” in which to operate.

Advertisement

With contributions legislated to rise year-in-year out, there is little incentive to run a lean business and a lot of opportunity to gouge.

The obvious result has been the massive fees and salaries paid for industry participants despite them delivering performance no better (or worse) than the sharemarket – something acknowledged by former Treasurer and Future Fund chair, Peter Costello.

Indeed, there are few better rent-seeking industries to be in than superannuation, which is why reforms to fix the underlying problems in the system (e.g. excessive fees, unequal distribution of concessions on contributions/earnings, etc) is critical before policy makers even consider raising the compulsory superannuation rate.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.