The expected arrival of Amazon in Australia in late-18 will challenge many retailers (see Q-series). Given retail is Australia’s 2nd largest employer, it will probably have enough impact to influence the broader economy. Overall we find total jobs growth may be marginally slower than otherwise, but the largest impact is likely retail price disinflation.

But the trend of retail sales and employment growth have already slumped

There are concerns Amazon’s entry could lead to a slump of retail sales for incumbents, which then hurts employment. However, we highlight the retail sector’s share of consumption already declined for decades to a record low under ~⅓ (Figure 2). More recently, this reflects a cyclical slowdown in retail sales to a trend of around ~3% y/y, which is only ~half of the pre-GFC trend. Indeed, retail employment has already been broadly flat since 2007, and is currently falling ~3% y/y, the worst decline on record.

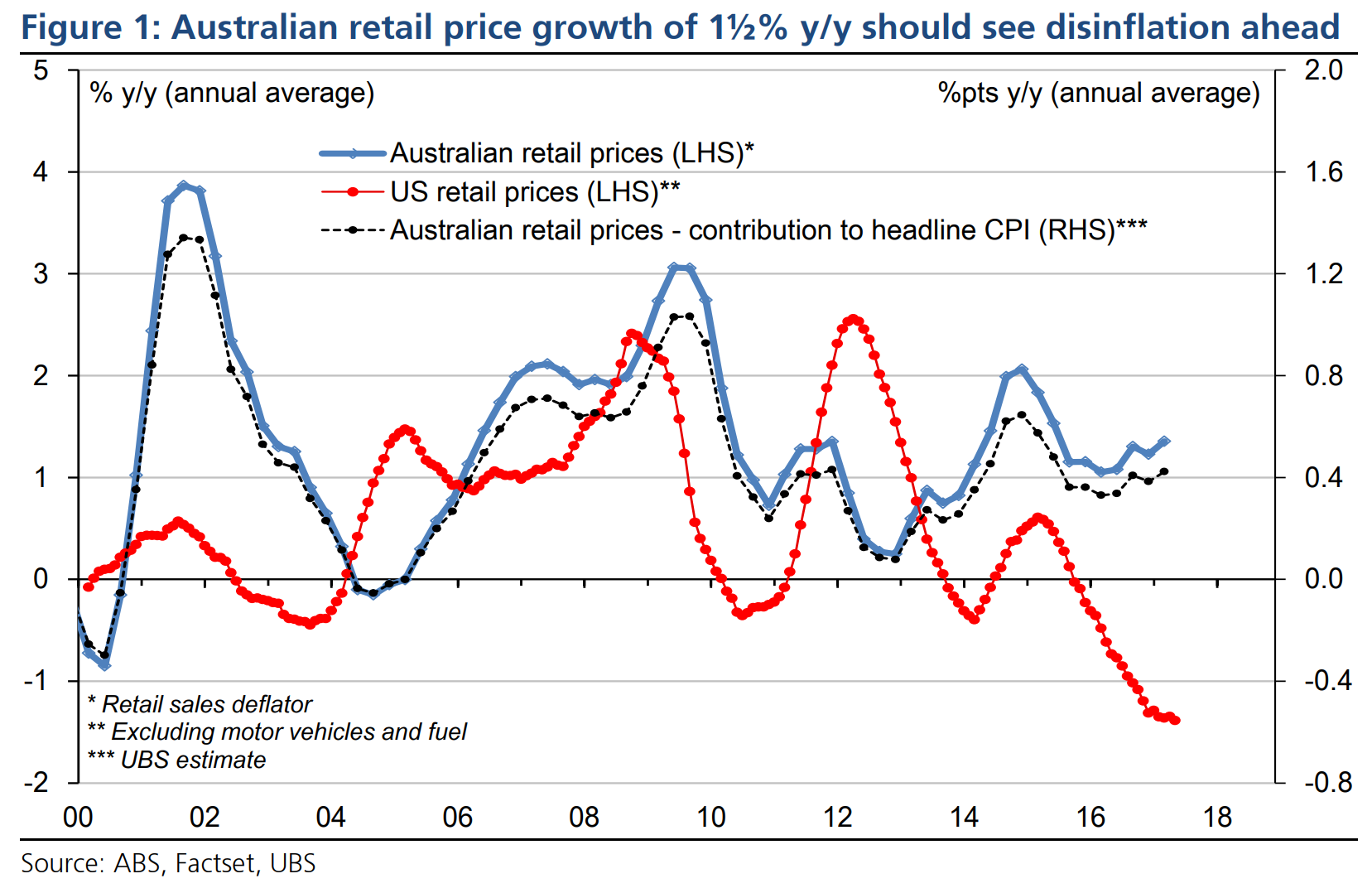

Amazon should slow retail prices, & subtract up to ~¼% from CPI (over time) Amazon will likely intensify retail price disinflation pressure.

In the US, since 2008 retail prices (ex-autos & fuel) averaged <½% y/y, far below 1½% in Australia. Indeed, current retail price growth in Australia is 1½% – contributing ~0.4%pts to headline CPI (albeit driven by food) – and is now even further above the US where retail prices are falling. We estimate that each ½%pt slowing of Australian retail price growth would reduce CPI by ~0.15%pts. Hence, if Australia converged to the post-GFC trend in the US, it would cut up to ¼%pt from CPI, albeit likely adjusting over more than one year.

Overall, this looming disinflation impact from Amazon on the retail sector (along with a ~¼%pt technical drag on CPI from reweighting) aligns with our ‘low inflation’ thesis, despite positive lead indicators and a backdrop of better global growth. Importantly, this pressure on the retail sector through 2018 is colliding with an unfolding housing correction and ~record low household cash flow (as banks re-price mortgage rates higher). This would likely limit the RBA’s willingness to join global central banks hawkish tilt, and raises the risk of a delay to our late-2018 start to RBA normalisation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.