Canada has started; the US has been on the path for some time; the ECB’s tone has shifted and so has that of Norway and Sweden. Australia? Soon, but not yet. In our view, the key two factors that forced the RBA to cut to a very low, 1.50%, cash rate setting are now both receding. First, was the massive resources cycle, with very low rates needed to rebalance growth to the non-mining sectors as mining investment and commodity prices fell. Second, extraordinarily low global interest rates meant that a low cash rate was needed to keep the AUD down, again, to rebalance growth. Now, with the mining downturn around its trough and global rates rising, Australia may not need a record low cash rate for much longer. But, unlike with the other central banks, don’t expect forward guidance from the RBA. You’ve got to watch the data. We expect a hike in Q1 2018.

The global economy is currently experiencing its most synchronised upswing in a number of years. The US, which has been leading the recovery, is continuing to show positive growth momentum. European activity indicators have had a run of upside surprises. Global trade has been lifting, supporting growth in Asia. Notwithstanding still benign inflation pressures in most countries, a number of central banks have turned less dovish recently, as a result of lifting economic activity and tightening labour markets. Some are lifting rates, others suggesting cuts are now unlikely and still others, hinting that they may slow asset purchase programmes.

For Australia, this episode has been a bit unusual. Australia’s central bank is often one of the first to start lifting rates in global upswings. But there are a few differences this time around.

First, commodity prices have not been lifting. This may reflect that the recent lift in global activity indicators has been most significant in the developed economies, with most of the upside surprises in Europe, so there has been less upward momentum in metals prices than if China’s investment was leading the way. Developed world growth tends to be less commodity-intensive than China’s growth. The lift in global trade has also allowed China scope to tighten local financial conditions, to help deal with some of its own imbalances, again, softening growth in housing and infrastructure investment.

Second, local wages growth and underlying inflation are low, although we expect that both are at or past their troughs. We see the slowdown in wages growth as partly the result of the long, drawn out, downturn in the mining industry, as high paid mining jobs were lost and replaced by lower paid services jobs. Wages growth has been showing some signs of stabilising and we expect growth to edged higher in H2 2017. As a result, underlying inflation is below the RBA’s 2-3% target band, although it looks to be past its trough. The RBA will need to be convinced that wages growth is past its trough to start hiking.

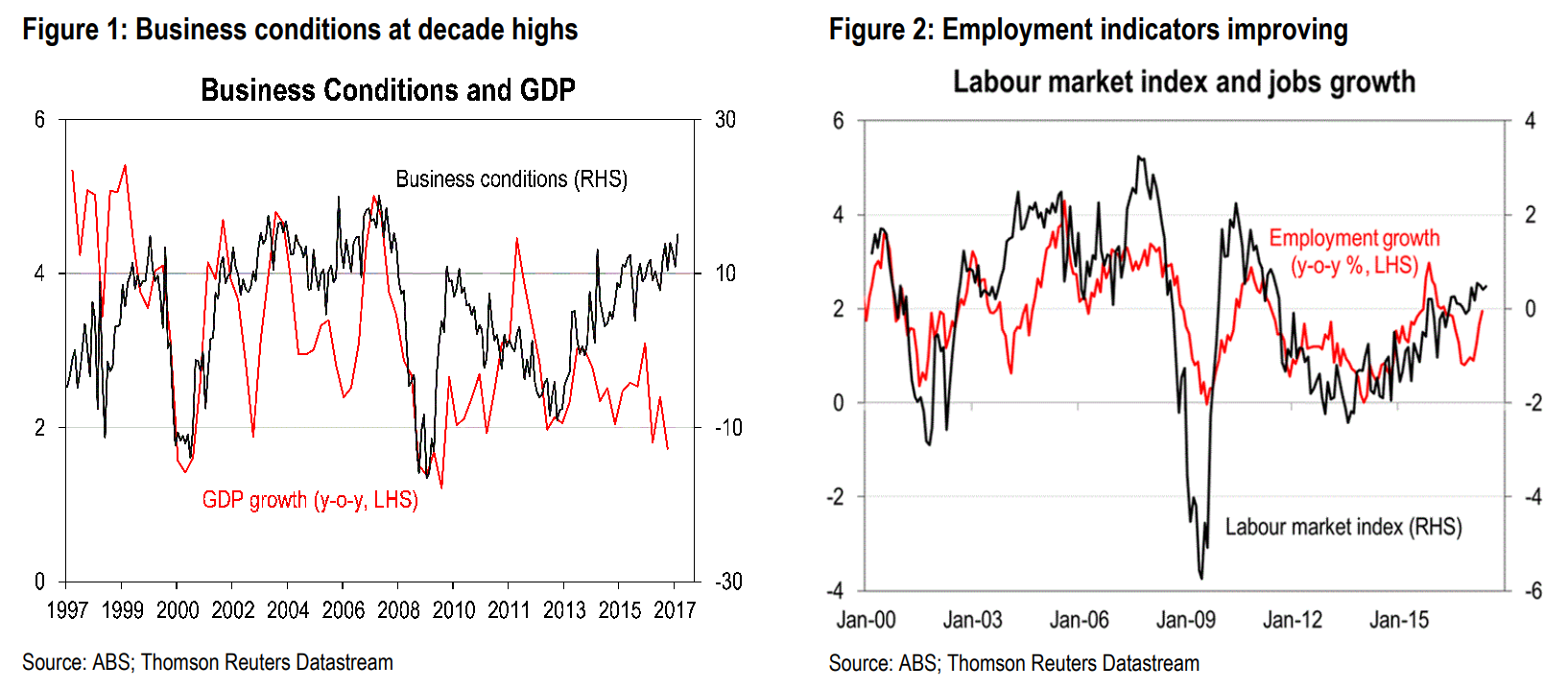

Third, there have been some measurement challenges recently, which have made it harder to get a clear view of the economic momentum. Q1 GDP growth, which ran at a below trend rate of 1.7% y-o-y, was held back by wet weather on the East Coast and the impact of Cyclone Debbie. Measures that are better at abstracting from the weather-related effects, such as surveyed business, which forms part of it conditions, are at around decade-highs, implying much stronger growth (Chart 1). Measurement issues in the labour force survey have also meant that momentum may have been understated. However, the official labour force numbers for the past three months have started to come back into line with other timely labour market surveys (Chart 2).

Our overall view is grounded in the idea that the biggest factor driving the RBA to cut all the way to 1.50% had been the massive cycle in the resources sector, and that this is now over. The boom and downturn was at least three times larger than anything Australia had previously seen. In addition, global interest rates have also been at historical lows, which has impacted local policy through the currency. With the mining downturn now stabilising and global rates lifting, we doubt the RBA will need its very accommodative setting for much longer. Besides, the low cash rate is also causing unwanted exuberance in the Sydney and Melbourne housing markets (auction clearance rates are still around 70% in both markets).

Nonetheless, the market seems reluctant to price in RBA hikes over the next 12 months. The market is currently pricing that the RBA is unlikely to lift its cash rate until mid-to-late2018, with OIS 50:50 priced for a 25bp hike by May 2018. This may partly reflect some of the issues with commodity prices and local measurement issues that we have raised above. It could also reflect that markets have become used to central banks, including the ones we discussed above, providing forward guidance before they take action. Keep in mind, the RBA does not do this.

Consider:

dwelling construction boom rolling over right now;

bulk commodity prices to fall again into year end;

mining and wider capex still falling all next year;

car industry closing;

income growth structurally stuffed by mass immigration being used to support the above,

Budget at imminent downgrade risk;

house prices set to slow as banks already hike rates, and

dollar to the moon.

Nothing would give me greater pleasure than seeing the RBA hike rates into the dumb bubble but it ain’t going to happen.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.