Friday night saw more DXY weakness:

Driven largely by EUR strength:

The Aussie pulled back against both:

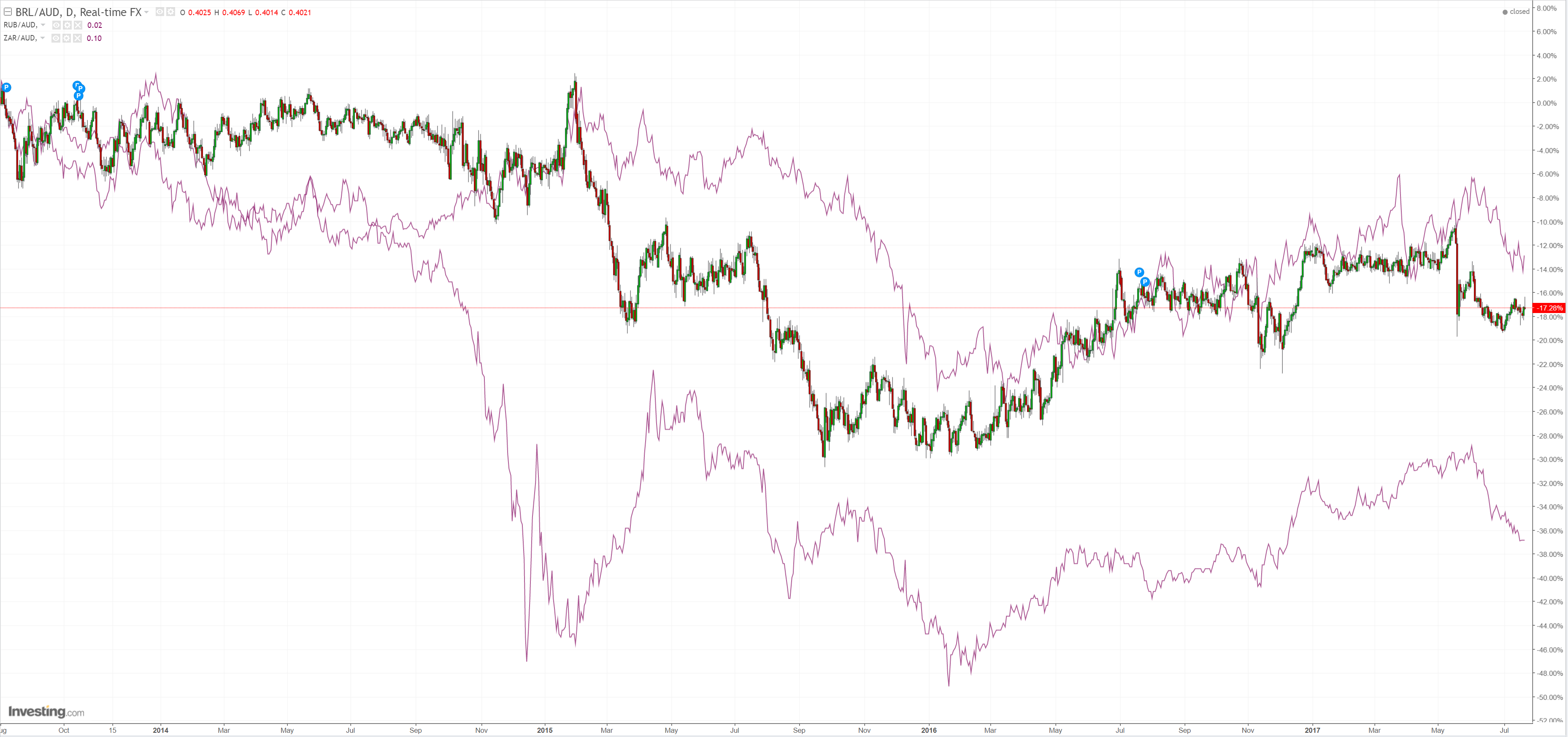

And EM forex:

Gold took off, reaffirming more USD weakness:

Brent was pounded:

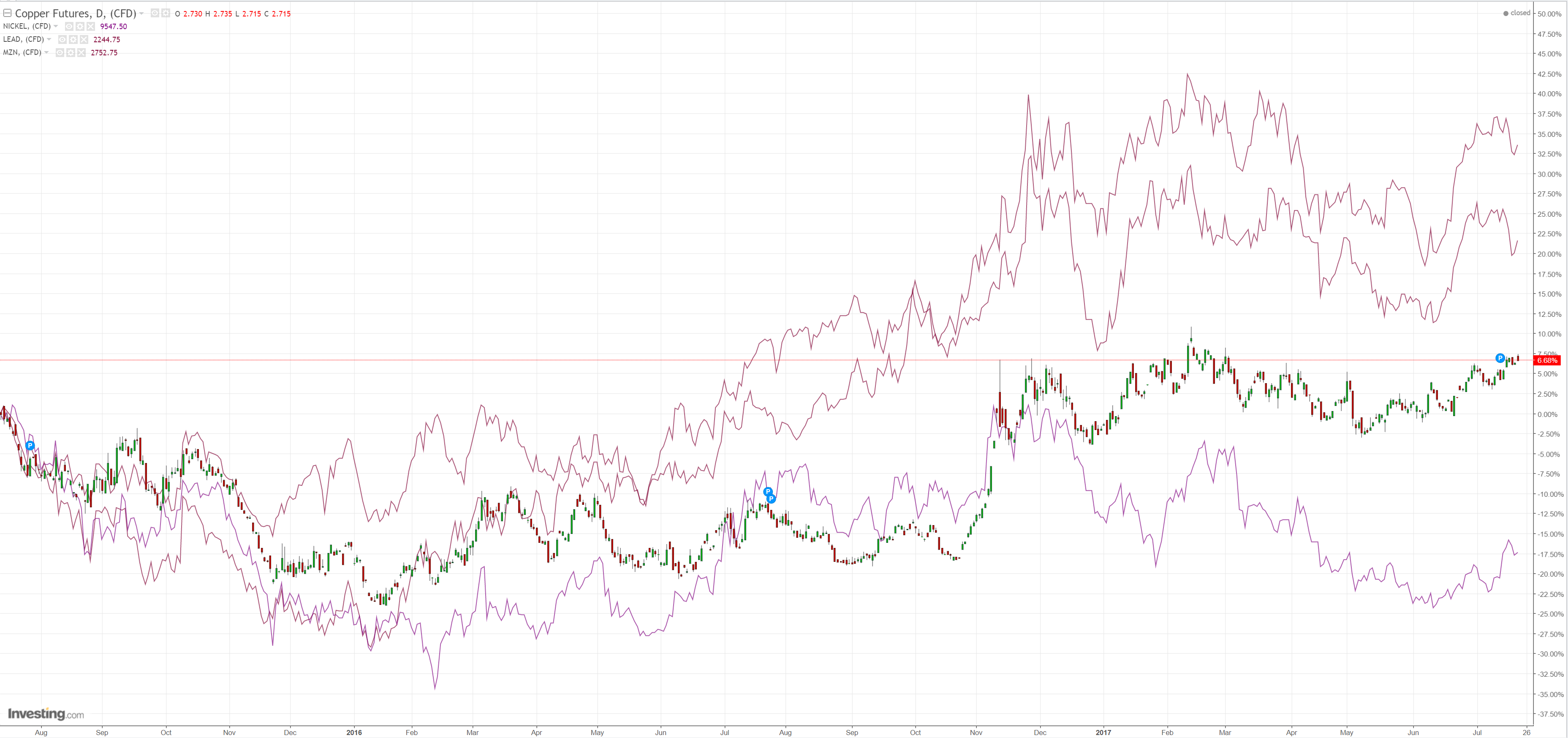

Base metals held up:

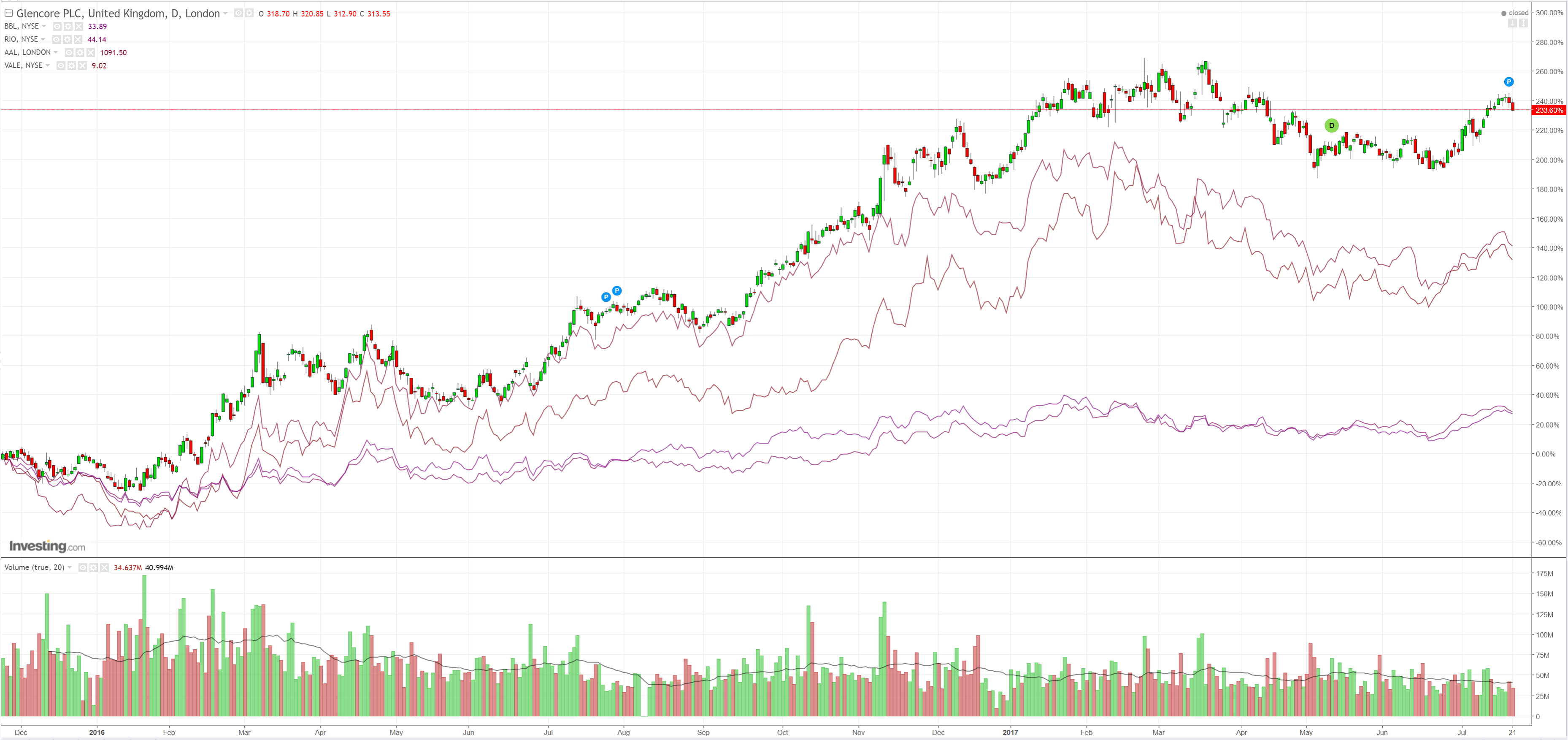

Big miners didn’t:

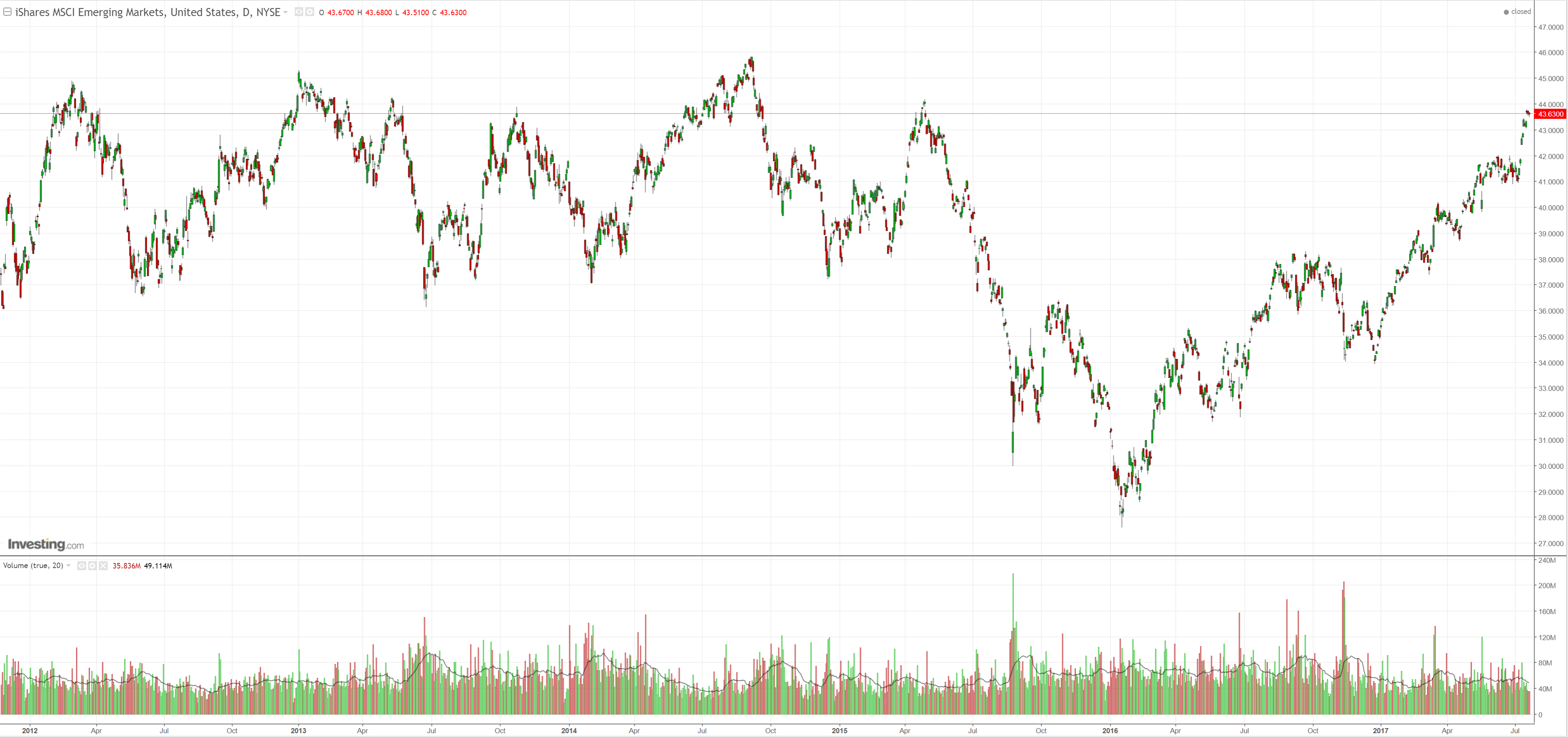

EM stocks sold:

But high yield rallied:

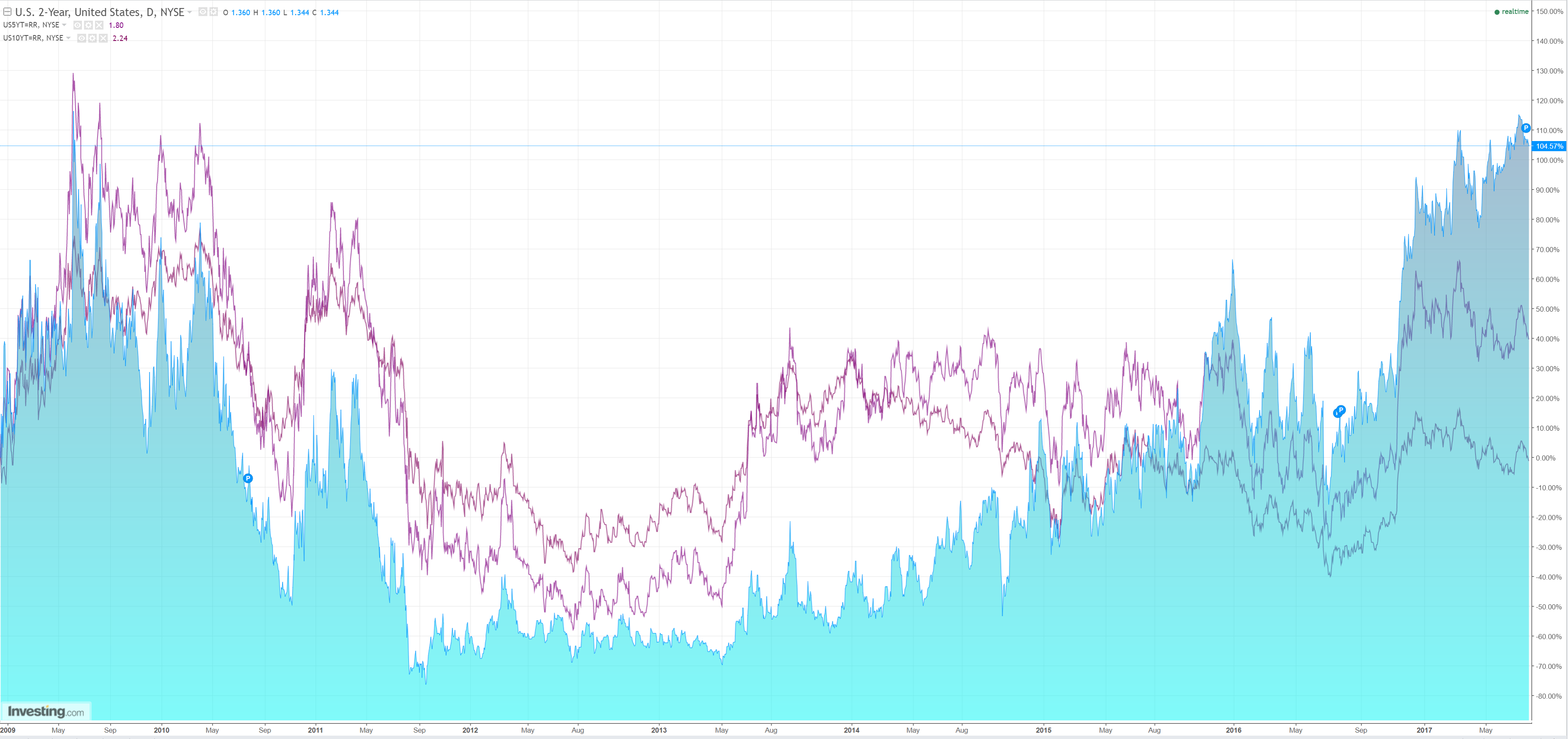

US bonds were bought:

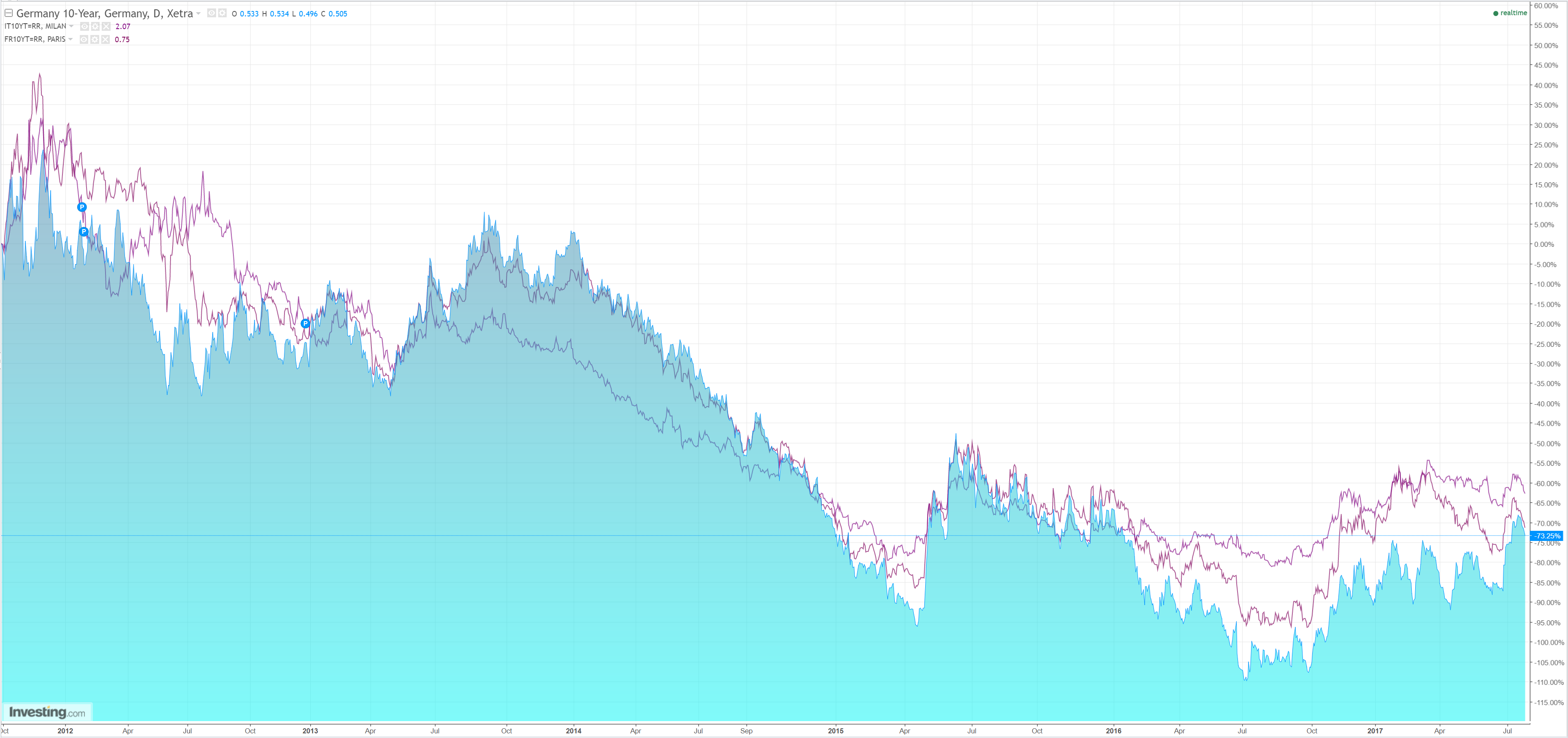

And European:

Stocks eased in the US and look at risk of breaking down in Europe as the EUR rockets:

So, has the Aussie dollar peaked already? There are two reasons to think it may have.

First, the RBA clearly has no intention of hiking unless absolutely forced to to quell house prices. The recent hawkish signals in the minutes were pure incompetence. Before it even considers tightening, MP2.0 has to play out and APRA has another chance to tighten later this year when it adjusts risk-weights. That pushes us out until mid-next year when the RBA will be facing all manner of renewed economic headwinds.

Second, the iron ore rally also looks close to exhaustion. I don’t think it will fall like a stone for a few months yet but $70 appears the ceiling for the restock.

These are big supports knocked out from under the Aussie rally.

But, there is one other very strong updraft. The weak USD looks set to continue as it rebalances against a resurgent EUR. Policy convergence is the narrative de jour and as US political risk rises while European falls, that will continue. This will be exacerbated by weak oil prices and disinflation. Another 5-10% swing to the EUR looks plausible.

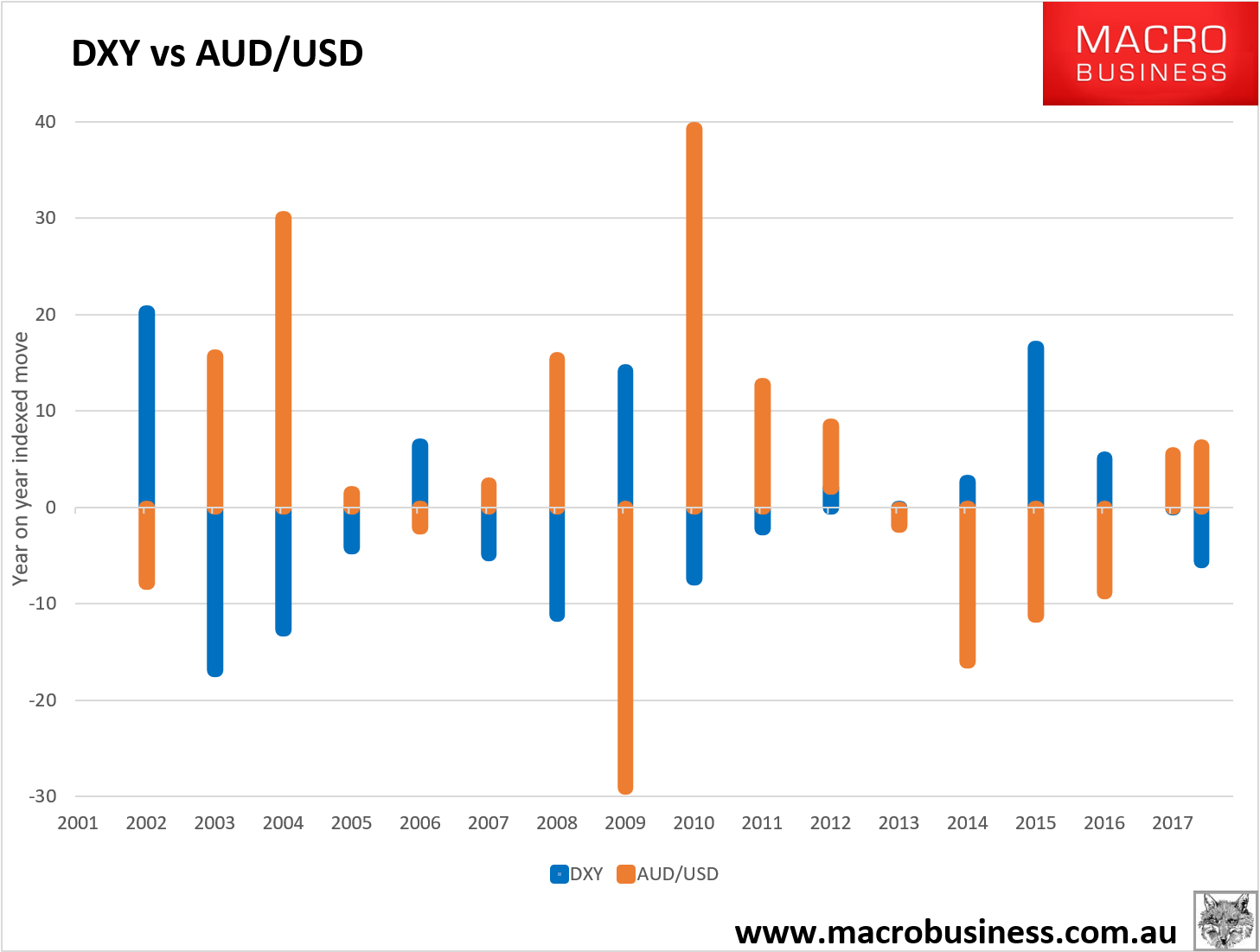

I’ve created the following chart to help us fathom how USD specific versus AUD specific forces are acting upon the Battler over time:

Note that at the Millennium, DXY (the USD basket) was booming along with tech America. But post-tech bust that reversed and DXY was consistently weak (other than the GFC) right through until 2012 as it fought off deflation with low interest rates. That reversed powerfully again until 2016 as tapering began.

The Australian dollar specific forces ebbed and flowed with Chinese strength. Up from 2003 through 2012. Then down as China began its great rebalancing process. However, since China hit the accelerator in 2016 there has been more strength in the China proxy play.

The past six months has seen both DXY weakness and AUD strength in equal measure as US prospects dimmed while China stimulated. For the period ahead, at least through this quarter, the odds favour this being sustained. Market positioning is overbought but there is room for more buying of the AUD yet:

But, by Q4, I expect the Aussie specific variables to be in fast retreat. China ought to be slowing at the margin and iron ore headed to $40 or below. As well, it ought to be more clear that China is embarking on another round of reform that will slow growth in 2018 (as recent news flow has confirmed).

As well, the oil shock will be at its deepest in Q4, holding back the Fed. But markets should at least begin to be able to look past it for 2018 when the US economy will still have by far the tightest labour market of DMs, certainly much more so than Europe. There is also still a decent chance that Republicans manage to agree at least on tax cuts. Timing this USD/EUR swing is not easy but seems a reasonable prospect by Q1 next year.

In short, I still reckon there’s a better than even chance that the Aussie gets through 80 over this quarter but the odds also suggest a bigger story of a fast retreat just beyond that.

A temporary spike in the currency is an attractive entry point into international assets given the currency is structurally weak for the longer term.

Disclosure: I’m the strategist for the Macrobusiness Fund which is currently overweight international stocks. We also run an international equities fund. Both of these will benefit from a falling Australian dollar and so I am definitely talking my own book.

Register your interest in the fund and we’ll be touch.