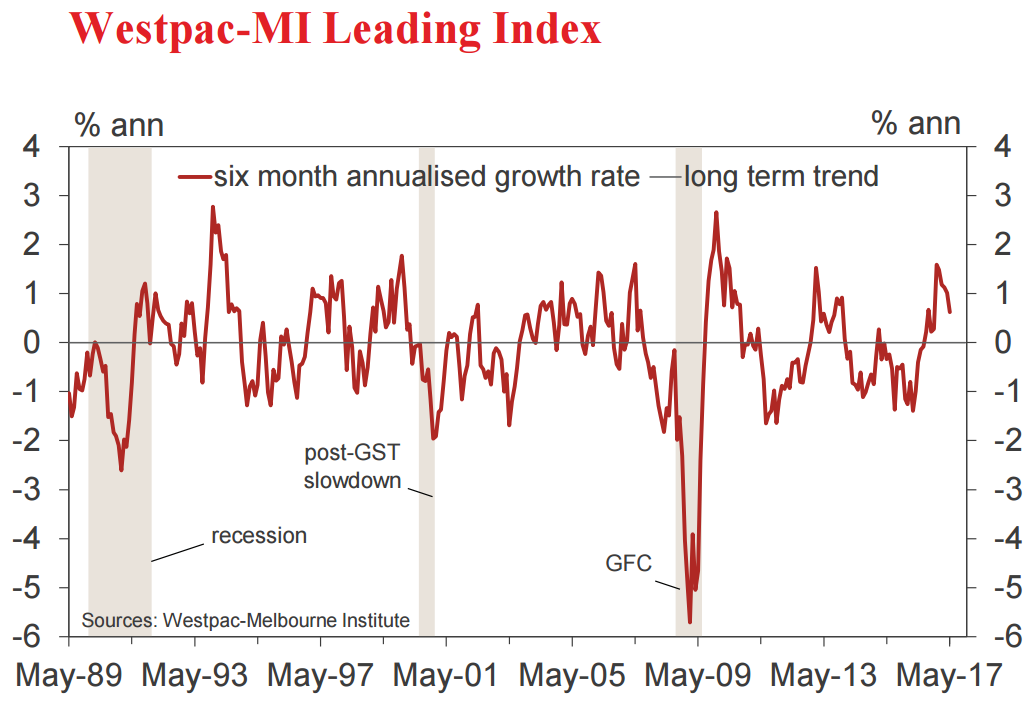

• The six month annualised growth rate in the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, eased from 1.01% in April to 0.62% in May.

The index is pointing to a clear slowing in momentum. While the growth rate remains comfortably above trend, the pace has eased markedly since the start of the year. The shift mainly reflects a less supportive backdrop for Australia’s commodity prices and in global financial markets.

The Leading Index growth rate has slowed from 1.59% in December to 0.62% in May. Two components have driven the slowdown: commodity prices and the yield spread.

After surging 44% between June and February, Australia’s commodity prices have declined 10% over the last three months. The turnaround has taken 1.17ppts off the Leading index growth rate since end 2016. Some of this reflects the unwind of temporary policy and weather-related spikes in coal prices. However, a strong rally in iron ore prices through much of last year has also moved into reverse since early 2017. Both moves look likely to be sustained.

The yield spread – the difference between the short and long term interest rates – captures financial market assessments of the economic outlook both locally and abroad (long term rates are heavily influenced by benchmark rates abroad). After widening significantly over the second half of 2016, the yield gap has narrowed sharply in 2017, led by lower 10yr bond rates as markets have pared back expectations for growth stimulus policies in the US. The move has taken 0.42ppts off the Index growth rate since December.

The other international component – US industrial production – has provided some offset over the same period, a lift in activity adding +0.28ppts to the Leading Index growth rate. 21 June 2017

Domestic components have boosted the Index growth rate between December and May although individual contributions have varied widely. The positive signals have been from dwelling approvals (adding +0.29ppts); and aggregate hours worked (+0.17ppts), partially offset by weaker reads from the S&P/ASX 200; Westpac-MI UE index and Westpac-MI CSI expectations index (a combined drag of –0.13ppts).

The Reserve Bank Board next meets on July 4. Recent comments indicate that policy is firmly on hold with the Bank expecting growth to increase gradually to an above trend pace. The Leading Index has been pointing to above trend momentum since late last year but the latest updates suggest the growth pulse is moderating heading into the second half of 2017 highlighting downside risks to the 2018 growth outlook. We expect the Bank to leave rates unchanged over the rest of 2017 and throughout 2018.

While I am not a huge fan of the index, with growth at 1.7% today and the leading index pointing to moderation, it ain’t a good look!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.