At the AFR:

The most dramatic three-month surge in job creation in 12 years is stoking speculation the long post-boom era of sluggish wages growth, which has helped support hiring at a time of falling national income, will eventually near its end.

Former Reserve Bank board member Warwick McKibbin said the figures confirm that official interest rates should be higher than the current 1.5 per cent benchmark rate, but conceded it would be difficult for the central bank to hike while inflation remains low.

“I can’t imagine a story where the Reserve Bank would be cutting interest rates in the next six months, unless there is an international crisis,” Professor McKibbin told The Australian Financial Review.

“We’ve definitely got loose monetary policy in an economy which is getting close to full employment.”

“There is investment strength right across the board. Incomes [from the terms of trade via company profits] are rising and the nominal GDP numbers and forecasts are quite strong. The big uncertainty is how consumers will respond.”

…Workers may also be curbing wage claims because of concerns over the growing impact on work from robots and artificial intelligence. “Perhaps workers aren’t pushing for higher wages because of the uncertain future for jobs.

“The pressures of technology and pressures of trade make it very hard for people to be pushing for wage increases except in categories which are highly specialised and can compete in the world market.”

“That’s showing up in the data and the income distribution.”

“The bottom line is that monetary policy can’t deal with those questions. It comes to the big issues of energy reform, tax reform, flexibility in the economy, to deal with these transformations that are coming along. That’s where the answers are – not where interest rates are next week.”

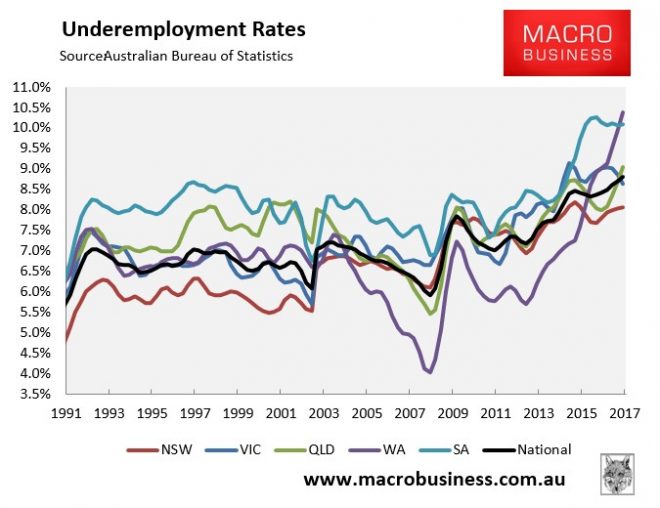

With respect, is this approaching full employment?

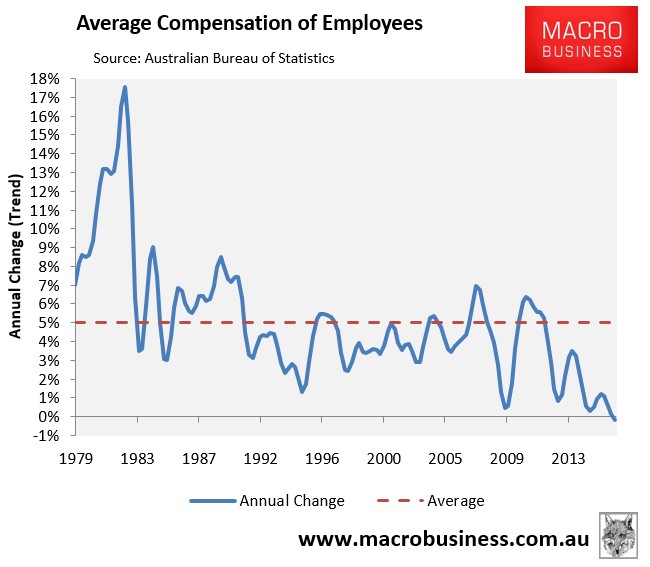

Is this rising income:

Is this rising investment?

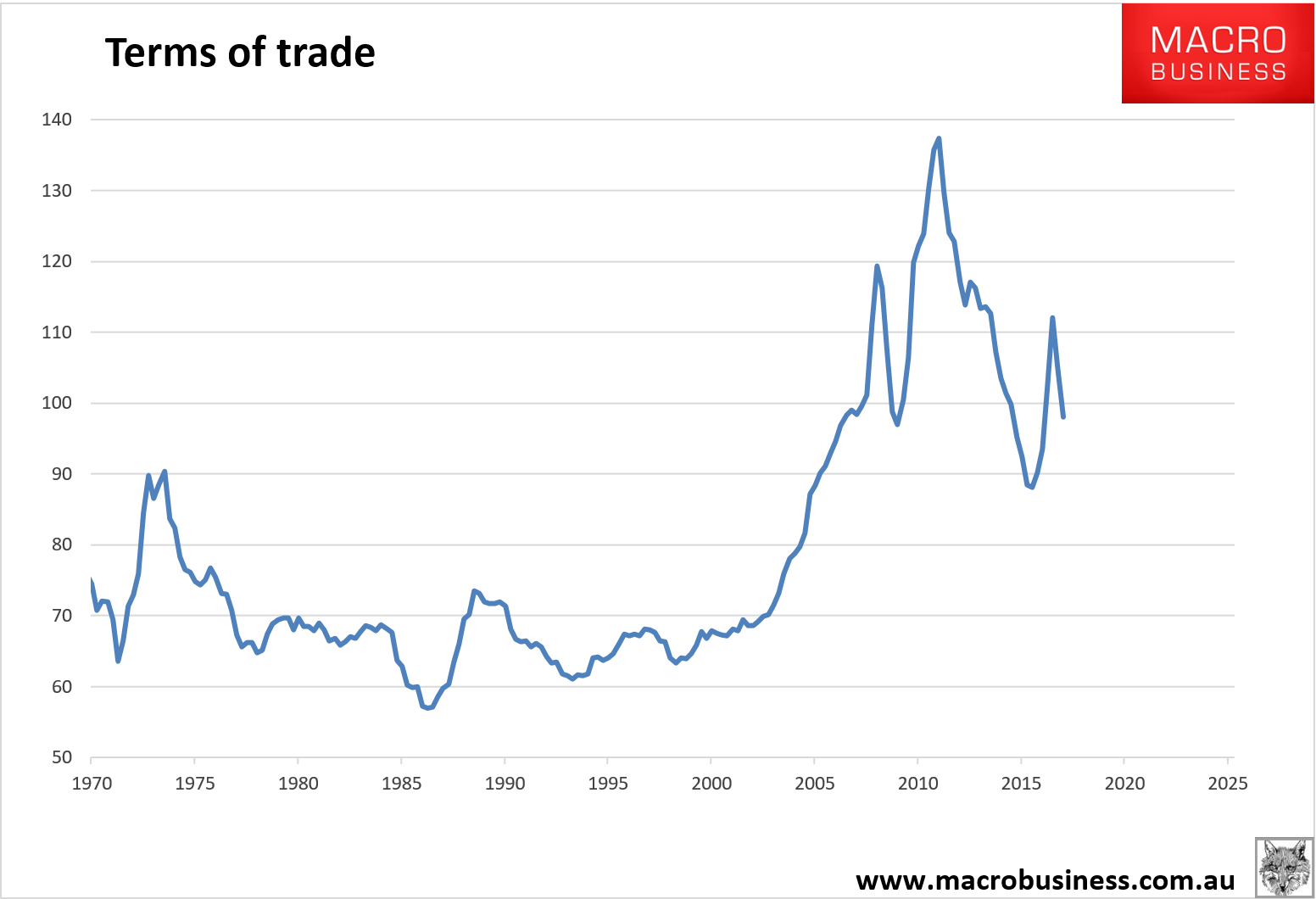

Is this a rising terms of trade?

We’ve had a brief rebound in commodity prices on the way down. Mining knows it which is why it is still slashing investment. The terms of trade will be at new lows next year barring some new convulsion in Chinese stimulus. That will combine with:

- the car industry shuttering;

- more falls in capex;

- a worsening gas shock;

- rolling dwelling construction;

- a sovereign downgrade;

- stalling house prices, and

- an immigration flooded labour market.

To punish income even more next year.

While the structural factors discussed by Professor McKibbin may be influencing wages, does a punter really stop and wonder if his job is about to be taken by a computer? Or, does he look around at his underemployed mates, choked with debt, overrun by cheap foreign labour, and think to himself, geez, I had better hang onto this job?

I can’t see an RBA cut this year, either. But banking on recovery is folly and the cut is coming. Monetary policy can contribute to structural repair, by lowering the currency.