Via Domainfax:

Felicity Emmett, ANZ:

Some of the weakness in Q1 is likely to prove temporary, although a bounce in Q2 looks unlikely at this stage. More broadly, there looks to have been a sustained step-down in the pace of consumer spending growth as households adjust to the new world order of very low wage growth. On that front, wages growth actually picked up in the quarter, but growth in unit labour costs remains negligible, which suggests that inflation is likely to stay low. On this whole, this confirms our view that the RBA is on hold for some time.

Paul Dales, Capital Economics:

The small 0.3% q/q rise in GDP in the first quarter won’t worry the RBA too much as some of it was due to the temporary influence of the severe weather. Nonetheless, we believe that GDP growth will be weaker than the RBA expects both this year and next, although that probably still won’t prompt it to cut interest rates further. More generally, the 4.3% q/q rise in mining investment was the first since 2013 and is an encouraging sign that we are getting close to the end of the mining bust.

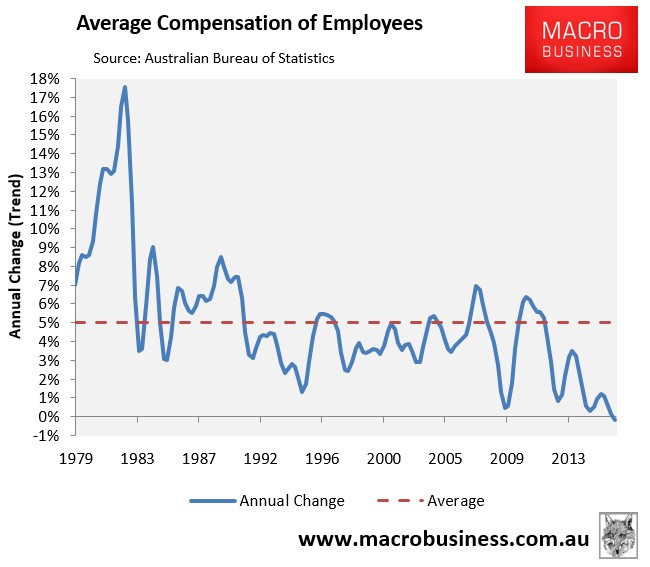

Paul Bloxham, HSBC:

The key challenge remains that, although corporate profits and nominal GDP have picked up, largely driven by the rise in commodity prices, this has yet to show up in wages growth. Compensation of employees rose in Q1, following a fall in Q4 2016, but is still running at a weak 1.5% y-o-y. At this stage there is little evidence of the boost to national incomes is flowing through to households. However, history suggests that it will. Yesterday’s decision to lift the minimum wage by more than in previous rounds may very well be the first sign of this starting to happen.

Rahul Bajoria, Barclays:

Despite the slowdown in growth, there are a few positive takeaways for policymakers in today’s GDP print. First, growth in household income, which has been a key focus, rebounded in Q1, despite a decline in hours worked and anemic wage growth. Second, private non-mining business investment expanded for the first time in more than 11 quarters, supporting the RBA’s view that the mining-related adjustment in capex is coming close to an end. Finally, the strong revival of nominal GDP growth is a positive for national income and should have positive spillovers for both the public sector and, eventually, households.

Su-Lin Ong, RBC Capital Markets:

Digging through the accounts, we would make a few observations. Firstly, the weaker real vs. stronger nominal/income story largely reflects upside surprises to commodity prices for much of the period since mid 2016 and is unlikely to continue. Secondly, the gain in national income remains very much skewed toward corporates. Thirdly, the composition of domestic demand in Q1 hints at a profile further into 2017 and more so in 2018, which likely shifts away from residential construction, which has been a key contributor to both growth and employment. Fourth, the wage, consumption, and household savings dynamics remain worrying. And finally, the persistently weak trend in unit labour costs, which are the key driver of non-tradable inflation and feed into the inflation outlook over the next 4-6 quarters, suggests that the risk lies in core inflation staying below the floor of the RBA’s 2-3% target range for longer.

Craig James, CommSec:

The Australian economy has had to contend with a lot of factors in the past year – geopolitics, weather events, the on-going unwinding of the mining construction boom and variable housing markets. So economic growth has trekked a zig-zag path. But importantly the record expansion remains on track. Especially positive is the health of the business sector with business conditions the best in nine years. The hope is that employment and investment will continue to lift, maintaining economic momentum.

Other more sane CBA economists:

On the monetary policy front, the market is correctly pricing in the chance of further policy easing. Today’s growth outcomes have significantly undershot the RBA’s expectations and it will take a heroic effort from here for GDP growth to meet their year-end forecast. However, we think that Governor Philip Lowe is desperate not to cut rates given it risks stimulating the housing market again. As such, we think that policy easing is off the table unless the housing market falters or the unemployment rate materially rises. The most recent employment reports suggest that things have improved a little more recently. But the dynamics at work in the economy suggest that any move in rates over the next year will be down and not up.

Ben Jarman, JPMorgan:

The 1Q national accounts add to the string of data on the activity side showing that the economy is below trend and will not be reducing excess capacity soon. With the household sector subject to further headwinds from rising interest servicing costs, the pressure on the RBA’s 3% and above GDP forecast continues to mount.

Riki Polygenis, NAB:

Today’s data are consistent with monetary policy remaining on hold. The RBA will look through the volatility in GDP, however mixed labour market outcomes and weak wages and inflation data will prevent any hike. Meanwhile, there is tentative evidence that macroprudential and policy changes are leading to a softening in dwelling price growth, which will help to mitigate economic risks associated with rising household debt levels should it continue.

Yeh, Bloxo, wages are going to magically pick up as the terms of trade crash:

Shakes head.