Via Mark Samter and the superb gas team at Credit Suisse:

The month of June should, in theory, reveal plenty about the much-fabled (by us at least) East Coast gas market. If the draft legislation for the ADGSM is anything to go by, particularly if no shortage is found for 2018, then potentially plenty of questions are going to be left unanswered though. In reality of course, whilst we had hoped for the final clarity on the initial phase of dealing with the problem, it is of course just the start of an ever growing problem with the East Coast gas market anyway. It is perhaps just a damning indictment on our political nous, but we were rather hoping the legislation (admittedly this is just the draft) would provide a bit more clarity on everything. Our initial thoughts on what is obvious and what is missing are:

■ Santos Horizon contract seemingly counts as ‘own gas’, not third-party which will reduce the size of any net deficit for GLNG: ‘own gas’ for the purposes of determining a net contributor means gas produced from one or more tenements:(a) owned by the LNG Project; or (b) wholly or partly owned by one or more entities of the LNG Project, where: (i) the gas is contracted directly to supply the LNG Project; and (ii) the gas was primarily developed for the purpose of the export. At face value there looks like potentially only ~250TJ/d (~91PJa) that could even be up for debate of available to divert domestically. What exactly happens if the shortage is bigger than this?

■ Process seemingly rules out use for Winter 2017: under the draft, where possible the minister will declare that a forthcoming calendar year is up for consideration as a ‘shortfall year’ on or about 1 July but no later than October 1. The Minsters declaration of whether the forthcoming year is a shortfall year must then be made between 30 to 60 days after the declaration.

■ Mechanism will make it very difficult for customers to secure gas supply for greater than one-year calendar terms: clarity on the availability of gas supply for the next calendar year will not be known before the September prior, making it difficult for both intermediaries and suppliers to provide quotes prior to this. Let’s say you want to buy gas for 2019 and there is a shortage in 2019, a buyer finds that out now as it physically can’t source the gas. The required gas is however not physically going to be made available for sale (under the ADGSM) until September 2018. How can anyone sign a long-term contract under this environment?

■ Consideration of ‘past performance’ limits ability to curtail production in response to export restrictions: the draft allows for the minster to consider any projects past compliance with any conditions and any “gamin”: of the ADGSM. Seemingly this rules out curtailing production below forecast levels in response to export controls; as such any restriction to exports will result in the gas being diverted to domestic to market.

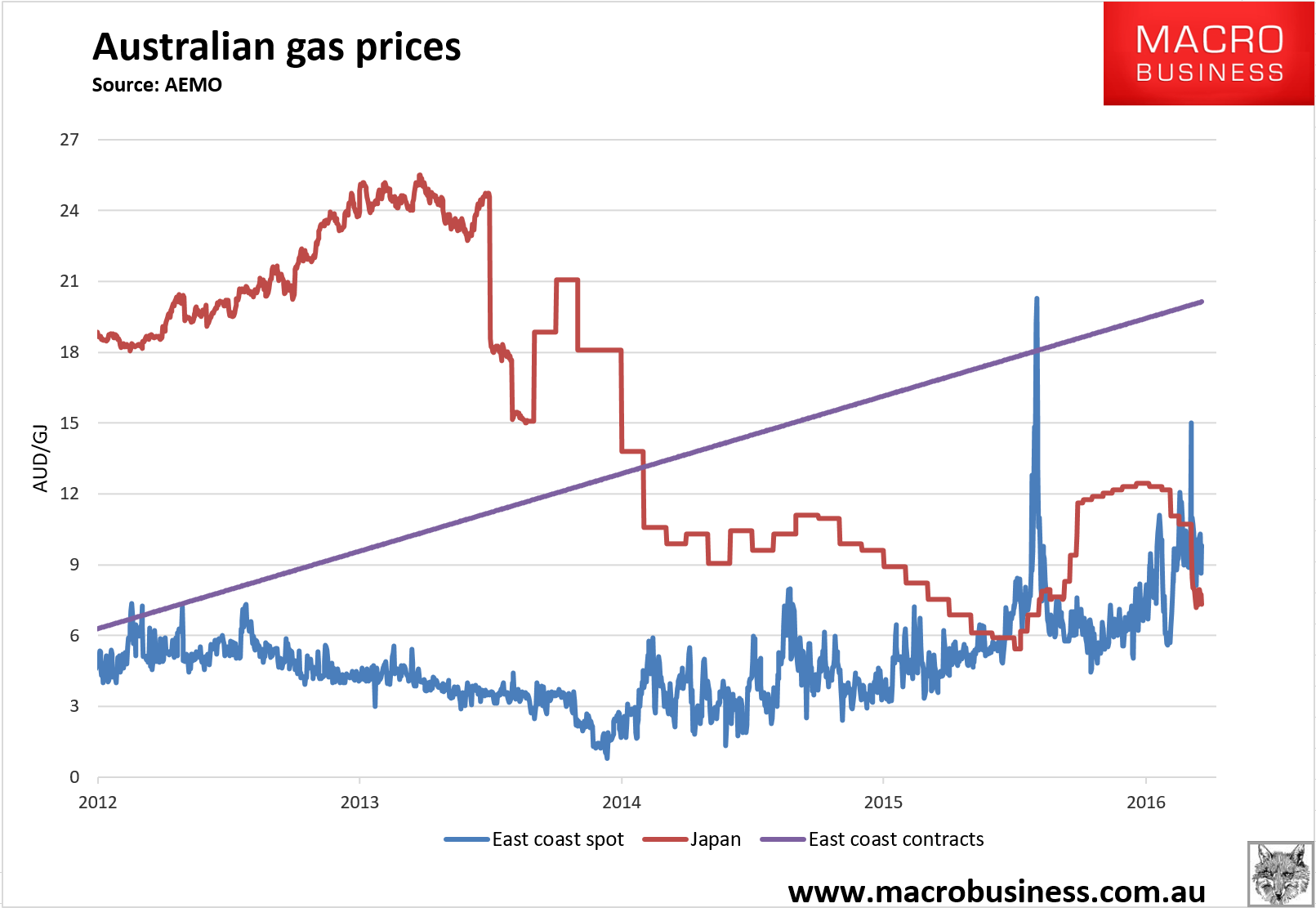

■ What does net-back actually mean? The shortage is to be assessed on the basis that the consumer pays no more than net-back pricing. It is unclear, if you believe in export price parity, what the reference point for net-back is. Is it Gladstone and then it is actually a net-plus price to deliver that gas to customers. Or a true net-back price. To put in context, the price differential for a Victorian customer between these two scenarios is a A$6–$7/GJ delta. Of course this can be solved with an import terminal… .Although, is this net-back price contract or spot? Again a $4–$6/GJ differential might exist

■ No clarity on price or physical obligation to actually sell the gas: Other than the above net-back price comment, which is seemingly just for assessing demand (and has wide interpretations anyway), there is no reference to a price mechanism for the ADGSM. There is also no clarity on what the obligations actually are for the volumes that are banned from export. Do they have to be sold, or just made available? One interpretation, when considering the reference to the “past performance clause” the gas just has to clear (i.e. forced seller). However, another interpretation is that you just have to make it clear at a net-back price and if it doesn’t clear then you can keep it in the ground.

Don’t be surprised if we see no “shortage” at first

The legislation says that the Minister will declare whether an upcoming calendar year is up for consideration as a “shortfall year” on or around 1st July (no later than October 1st). As such, in its virginal year, one would hope that we should get some clarity on whether 2018 is considered a potential shortfall year within the next few weeks.

There is absolutely every chance that we see no “shortage” for 2018 as determined by the collective arbiters. This can be brought about by a number of factors.

Firstly we, in the outside world, don’t know the commitments that the LNG projects have made for domestic volumes. Obviously the later the decision is made on when volumes have to be committed, the more the LNG projects will feel they have visibility (or a view at least) on spot LNG prices in the following year. This should logically influence the level of volumes they would be willing to divert.

Having said that, until we know what the obligation for GLNG is if the ADGSM is triggered, quite the opposite behaviour could start to get driven. For example, let’s assume there is no requirement for GLNG to clear that given volume, and all they have to do is make it available at their contract net-back price, then QCLNG and APLNG can just come in and price $0.01/GJ below this.

GLNG won’t compete on price if it doesn’t have to (as it is less profitable than exporting, remembering all its volumes are contract unlike the others, and if it doesn’t have to sell the gas it can keep it in the ground/storage and export it the following year), but the other projects could be realising multi-$/GJ higher prices than if they were selling those volumes on the LNG spot market.

As highlighted by EnergyQuest in the past week, which highlighted that ex-LNG fuel gas, demand was down ~16% in 1Q17 (we do think this number is volatile), there is of course also the risk that it is already too late to prevent material demand destruction.

Of course, in our minds at least, a mechanism that never gets triggered because demand does all of the balancing can hardly be claimed as a success for the broader country. The question also needs to continue to be asked, what is a shortage? Is it a physical availability of gas or a shortage of affordable gas. With spot prices in the past few weeks at times above net back LNG prices (if not net-forward) that would suggest a shortage to us. If, as we are seeing at the moment, industrial customers still can’t get offered 2019 volumes and are, in many cases, getting offers of close to A$20/GJ for 2018, that again for us is indicative of a shortage. Does it necessarily mean there is a physical inability to provide gas for the volume required though? Not necessarily.

Market will need signals on medium-term fix

We are firmly of the view that both the equity and gas markets will need to see some kind of move towards a more sustainable fix. At first take this legislation has not provided this. As much as the 2018 shortfall, or not, may get the headlines the debate is more about what actually happens over the next couple of years (and decades).

Clearly, with prices of A$15–$20/GJ seemingly still the norm for industrial buyers to receive for 2018 (for smaller buyers we understand prices haven’t fallen, perhaps large buyers can still get around A$8–$10/GJ), there is something that is not all quite right in the system. But what about 2019?

It seems almost impossible for buyers to get volumes, at any price, offered for 2019 and beyond. Yet, what seems clear (if anything is clear with the mechanism) is that, if there is a shortage in say 2019, the volumes to make up the shortage will only be “released” under the mechanism at some stage between July–October 2018.

So how do industrial buyers manage their supply in this environment? If there is a large shortage then clearly at least a portion of buyers will continue to be unable to physically secure 2019 volumes pre the enactment of the mechanism, but can they afford to wait for it to be put in place in mid-2018 for 2019 volumes?

Assuming the ADGSM stays away from price (which is still entirely unclear), how will they know what price they can be expected to be offered and accordingly how can they make investment decisions that keep their businesses open through this period?

How too can bigger capital investment decisions be made when a buyer will now potentially be learning about what gas price it will be paying three to six months before the start of the year, seemingly with profoundly more volatility in that price from year to year?

At this stage we are still a bit baffled about the short-term band aid; what this all makes ever clearer to us is that gas buyers will need confidence in the medium-term fix if any can be expected to invest capital through this transition phase.

We get the balance between making gas affordable now and incentivising future supply to come to market. Whilst it is not an easy task, we suspect there is more of a middle ground than is sometimes made out as all sides fight for their position in the battle.

As we look to the longer-term picture for the gas market though, what the ADGSM has surely taught everyone involved is that prevention is the best form of medicine. Clearly the inoculation was needed four to five years ago to prevent the challenges now, it should not be overlooked that the decisions today are sowing the seeds of the challenges faced four to five years forward though.

LNG imports becoming more likely

‘Net-back for all consumers’ unlikely to be achieved with ADGSM due to southern supply decline

While we received little clarity regarding the price mechanism – or lack thereof – within the ADGSM, one takeaway was that net-back parity pricing was seemingly enshrined as the guiding principle; AEMO and others when forming estimates of whether or not the market is in shortfall were instructed to develop those forecasts:

■ “…using a reasonable price which reflects that Australian gas consumers should, on average, pay no more for their gas than the value of that same gas if sold for export (for example, net-back price).”

The unfortunate reality however is that expectations of a decline in output from nonQueensland basins (Cooper, Otway, Gippsland) make it likely that consumers in the southern states will face export net-forward pricing, not net-back. Numerous reports of $15–$20/GJ gas prices quoted to large industrial users suggest this is already the case. Further, when referring to Australian consumers, we would point out that the vast majority of consumers are located in the southern states, and thus the vast majority (not average) may face prices higher than net-back.

The underlying cause of net-forward versus net-back pricing is the self-sufficiency or otherwise of the Southern Markets. In a market where the southern market is largely selfsufficient, the balance of power rests with the consumers who can demand net-back pricing. In a market where the southern states are not self-sufficient, the power rests with the sellers. The ACCC referred to these scenarios as “Alternate Seller” versus “Alternate Buyer”

When one considers the much discussed pipeline tariffs to get gas from Queensland to the Southern Markets, the difference between a net-back and a net-forward price is going to be in the A$4–$6/GJ range.

Hence, if we are an LNG net-forward price, if the cost of liquefaction, shipping and regas for imported LNG comes in under that A$2–$3/GJ net-forward transportation cost then it is economically rational to import the gas.

Even off the same LNG contract price, at say a US$65/bbl oil price, we believe LNG from say WA would cost ~A$1/GJ in cash liquefaction costs, A$0.50–$0.75/GJ to ship and let’s say A$1/GJ or regasification (we would like more clarity on what this cost would be, particularly if you do smaller FRSUs at more than one import location). As can be seen, this should deliver gas cheaper than the pipeline network.

There are two obvious additions to the benefits of importing other LNG, from a delivered cost perspective. If we assume the net back price is the GLNG contract volumes (as this seems to be the targeted gas) then that is on a ~14x slope. One would suspect that you can secure new contracts now on a 12–13x slope, a ~A$0.85–$1.70/GJ price differential versus the GLNG contract.

In the shorter term too, an importer would be able to arbitrage the huge disconnect between spot LNG and contract prices.

Whilst some press commentary about importing LNG suggests it wouldn’t pass the ‘pub test’, in many ways perhaps the best use of government funds (certainly rather than building a pipeline from WA to the East Coast) would be spent on building/assisting with import facilities. Australia would not be Robinson Crusoe as an LNG exporter turned importer.

LNG imports are a direct substitute for pipelines

As we outline in the downside scenario in our bull & bear case APA’tite for destruction: Bull & bear, LNG imports are a direct substitute for gas delivered by pipeline. Put simply, the more gas that is imported/produced close to the major demand nodes, the less volume that needs to be transported from distant basins; i.e. from Queensland via APA’s network. It will be extremely interesting to see how the economics evolves of smaller scale FRSUs at more than one demand centre in the Southern states. With such a large part of demand in the large metropolitan areas in those states, direct imports to multiple demand centres would paint a very different picture for pipeline utilisation down the track.

Stock implications frankly still unknown

It would be hard to make too definitive a call on how this all ultimately plays out from a stock market perspective. One assumes that at some stage the unanswered questions, either directly or by implication, will be answered.

However, at first take (and we aren’t just saying this because of our upgrade on Santos this week) the doomsday scenario for the E&Ps doesn’t seem to be playing out. Whether this is the right thing for the broader economy is another question mind you, so any upside to our call on Santos might be a somewhat pyric victory from a more holistic perspective.

On the Santos front, again with a modicum of ambiguity, it appears that the Horizon contract in particular will be excluded from the calculations on net contribution (given the contract was signed pre-FID). With the other factor removing gas from consideration being if the gas was only sanctioned in order to supply LNG, we suspect the only volumes really that GLNG could be forced to divert are the Origin and AGL contracts.

This would equate to only ~90PJa (falling to ~70PJa post-2020 when one of the Origin contracts rolls of), plus any gas GLNG has been buying on the spot domestic gas market. This, in theory, mitigates the scale of loss for GLNG even if they are forced to sell volumes at a lower price domestically.

What it doesn’t address is the risk that something more draconian happens, impacting all of the stocks, as, when and if the ADGSM doesn’t have access to enough gas to fill the shortfall as we head into the turn of the decade.

So it is still a wait and see on it all from a stock perspective unfortunately. This is all ultimately going to play out one way or another, no matter how long people try and kick the can down the road. The challenge for us in the equity market is working out where that can, and the buck, stops.

It looks more and more like a fake domestic reservation mechanism to me, governed by an idiot with no framework to guide him over too long a time frame for it to matter. The gas shortage is very obviously right now given contracts are being negotiated today that extend into any physical shortage period:

If it is not used when contracts are being negotiated at $15-20 (double anywhere else in the world and 500% higher than the US) then when will it be?