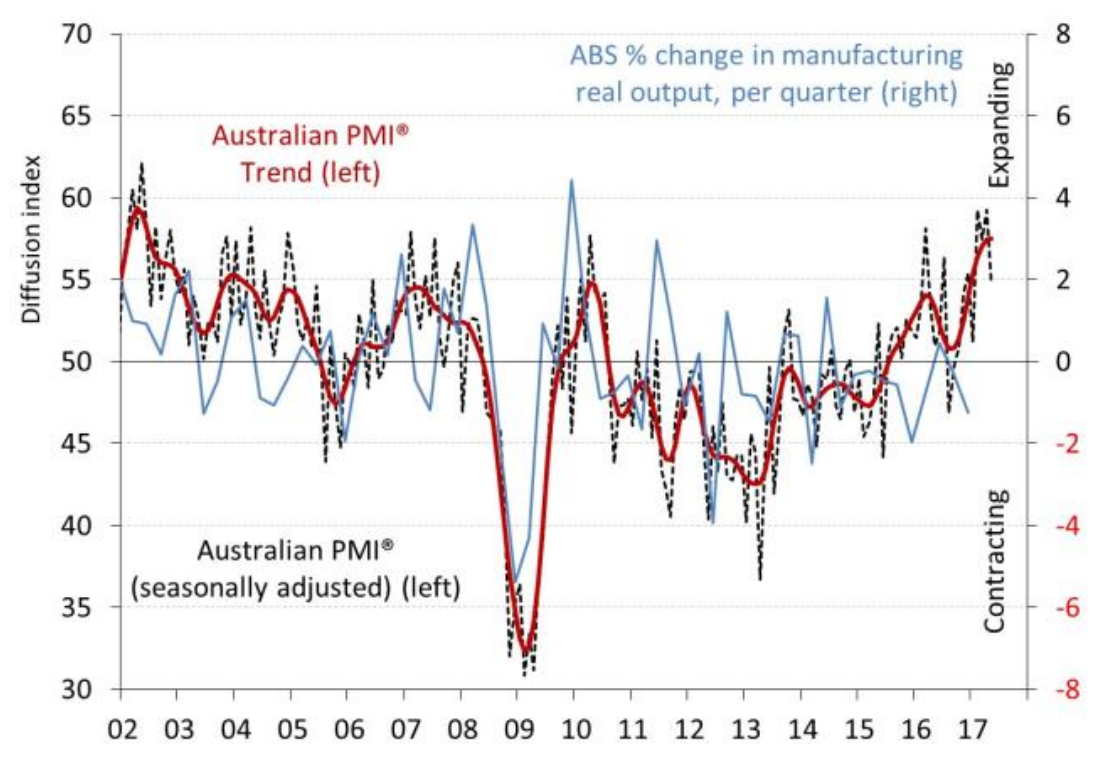

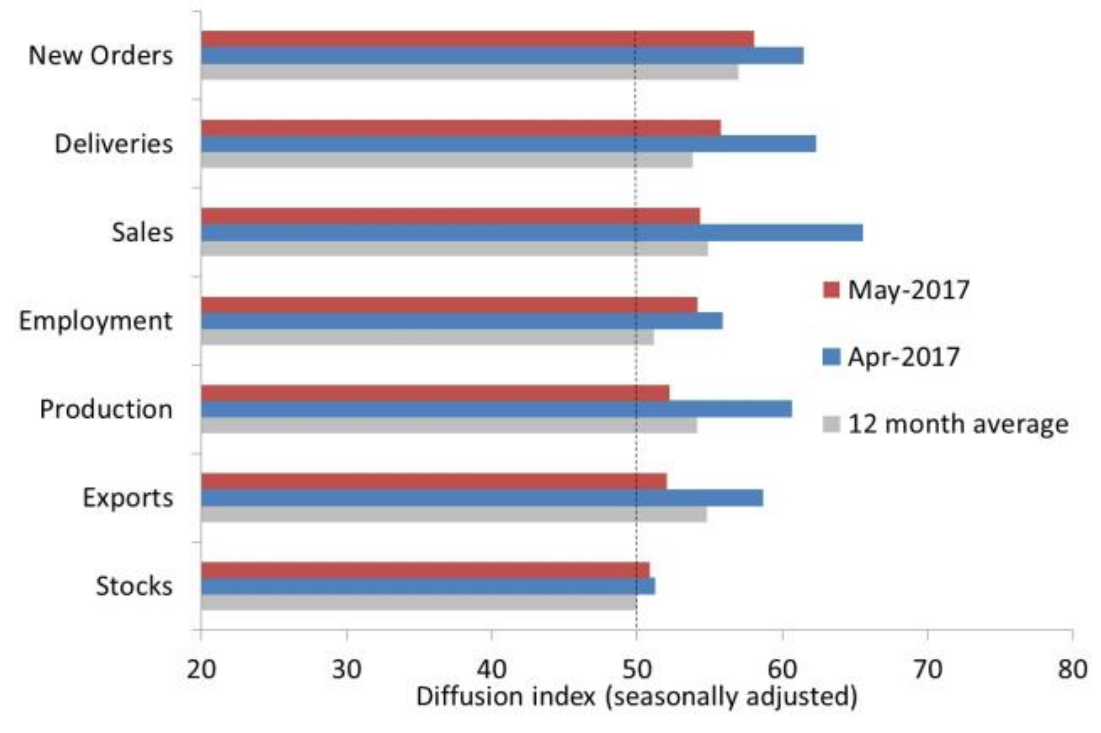

The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI® ) stayed in expansionary territory at 54.8 points in May, but it eased by 4.4 points and indicated a slower rate of growth (results above 50 indicate expansion with the distance from 50 points indicating the strength of expansion). This was the eighth month of expansion for the Australian PMI® . The last six months have averaged 56.2 points. All seven activity sub-indexes in the Australian PMI® expanded in May albeit at a slower pace than in April. New orders remained elevated (58.1 points), suggesting the current expansion has some way to run. Employment (54.2 points), deliveries (55.8 points) and sales (54.4 points) remained relatively strong. Exports (52.0 points) slowed but remained expansionary, as did production (52.2 points) and stocks (50.9 points). Seven out of eight sub-sectors in the Australian PMI® expanded in May, the same as in April (trend data). Expansions continued across all sub-sectors except textiles, clothing and other manufacturing (39.4 points). The recovery in wood & paper products strengthened (65.3 points) as did printing & recorded media (62.5 points), petroleum, coal & chemical products (56.7 points) and metal products (60.9 points). Other sub-sectors kept expanding but at a slower pace, including food & beverages (56.8 points), non-metallic mineral products (62.1 points) and machinery & equipment (58.9 points). Manufacturers reported slower conditions than previous months, although demand is still relatively elevated. Exports are a key source of growth with many manufacturers strongly focussed on export markets. Less positively, others are feeling the impacts of the exiting auto industry more acutely. Strong overseas competition remains evident and the Federal Budget has caused some unease. Slower retail conditions are also having some negative impacts for manufacturers, while slow capital expenditure by business is limiting demand for others. Elevated input costs are an ongoing challenge, particularly for raw materials and energy costs. Specialised labour shortages are posing challenges for some manufacturers.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.