by Chris Becker

A mixed end to the week for Asian shares with the Yen falling on the BOJ continued stimulus position, while Aussie and other markets sold off going into the close to end a lacklustre trading session.

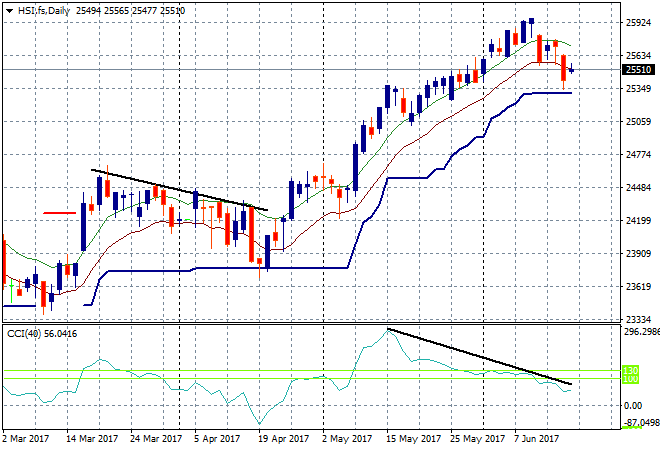

In mainland China the Shanghai Composite is down going into the close, off approx. 0.2% to 3126 points, still clinging above key support at the 3100 point level. The Hong Kong based Hang Seng Index however is doing better, currently up 0.3% 25648 points, bouncing off ATR support just above 25000 points which needs to hold before a retracement goes further:

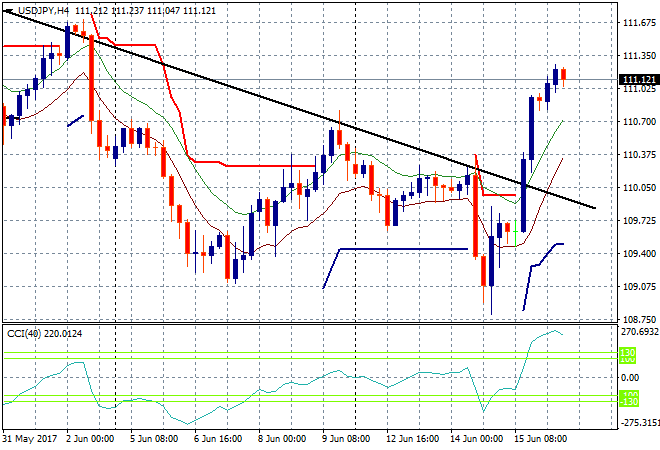

Japanese stocks were the highlight as the Yen fell against the USD overnight as domestic traders caught up and the BOJ continued the stimulus water taps. The Nikkei 225 gained over half a percent to close a smidge below 20,000 points erasing the earlier losses in the week. The USDJPY pair is hovering above the 111 handle, lifting slightly in the Asian session after the big overnight moves. The next target here is the former high at 111.70 or so:

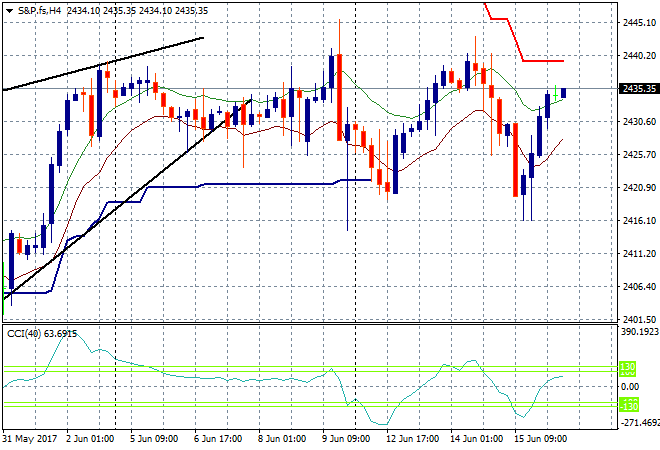

S&P futures are up slightly as traders maintain the cautious mood:

The ASX200 put in a light session to finish the week, up 0.2% to 5774 points. Financials saw modest gains as did the energy stocks but iron ore extractors fell slightly.

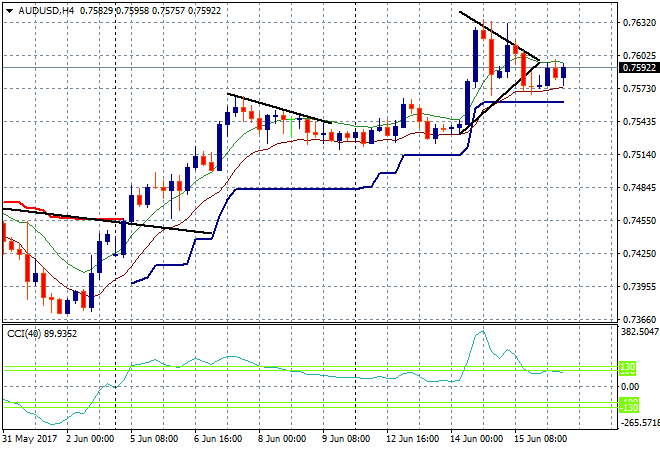

The Aussie dollar is very steady here and looking bullish going into the end of the week trading. The break below the lower side of the pennant/symmetrical triangle as not translated into further falls with ATR support fully respected so I’m watching for another break above the 76 handle soon:

The data calendar closes out the week with a few notable US releases, namely housing starts and another oil rig count, with the big one to watch the University of Michigan consumer confidence survey.

Until next week, havagoodweekend!