by Chris Becker

The selloff in tech stocks overnight has not affected Asian bourses as much as expected, with real caution and volatility still surrounding the outcome of the UK election and the shenanigans in the US.

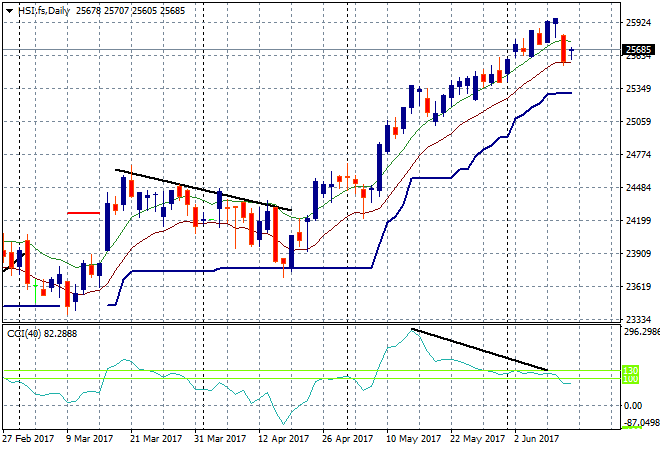

In mainland China the Shanghai Composite zoomed straight up after the long lunch break, reversing some of yesterday’s falls and currently up 0.4% going into the close at 3153 points, staying above key support at the 3100 point level. The Hong Kong based Hang Seng Index is also up, closing 0.3% higher to 25,975 points. The next target was the 2015 high at 28000, but this pause needs to hold on to the low moving average here or it could retrace to ATR support at just above 25,000 points quickly:

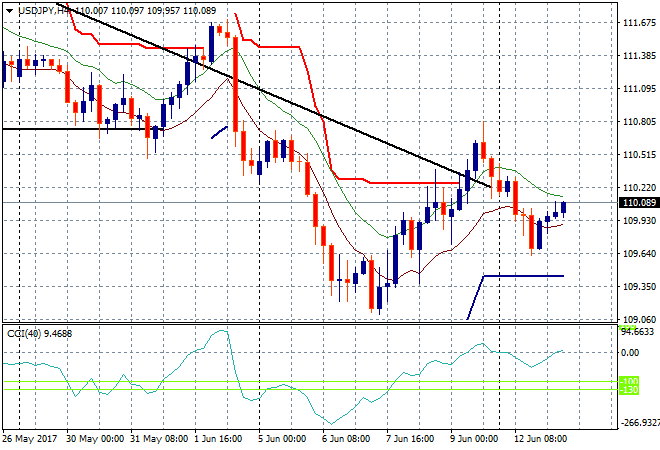

Japanese stocks were again mixed ever on a slightly retreating Yen, with the Nikkei 225 putting in a scratch session to remain below the 20,000 points level. The USDJPY pair is continuing its little bounce from last night and is currently just above the 110 handle, but not ATR resistance or the daily downtrend line. The next level to watch is support at 109.20 for another breakdown going into the FOMC Meeting:

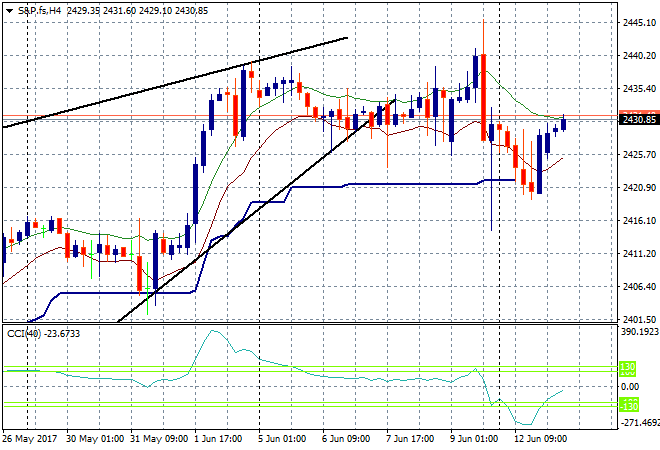

S&P futures are up slightly as traders don’t seem to care about domestic political imbruglios:

The ASX200 zoomed 1.7% higher on the re-open after the (unnecessary!) long weekend break, finishing at 5772 points. Gains across all sectors, except iron ore stocks with both Fortescue and RIO off, but financials going nuts all lifting at least 2% or more. This shows how closely watched the 200 day moving average is and how important the XXJ sector is to the rest of (read: less than 50%) of the “broader” (sic) market.

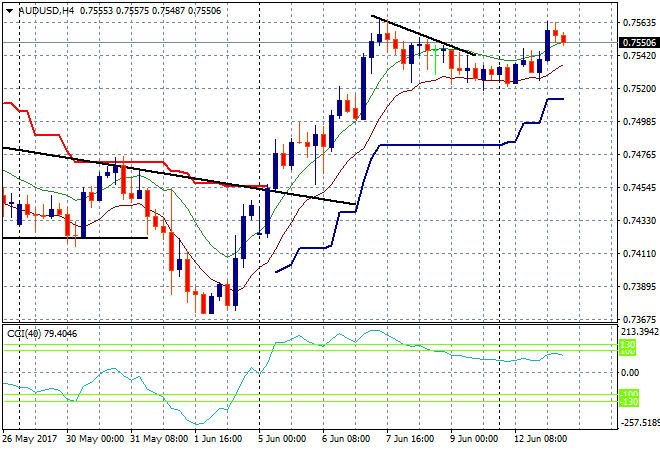

The Aussie dollar had a little go at breaking out higher, but is retracing below last week’s intrasesion high, currently sitting at 75.50 against the USD. I’m still watching the low moving average at the 75.20 level as a potential short on the downside here if USD strength regains:

The data calendar will be Euro focus again with the UK CPI print for May, then the important German ZEW economic sentiment survey.