by Chris Becker

The less than impressive local GDP result sure impressed Aussie buyers, send the local currency up to its previous high in May while stocks and bonds were non-plussed. Outside the domestic arena, the real focus is macro – the UK election, the Qatar and growing problems in the Middle East, the Twit-in-Chief, terrorism etc etc. A flight to safe havens including Yen and gold, now approaching $1300USD per ounce again underpin that caution.

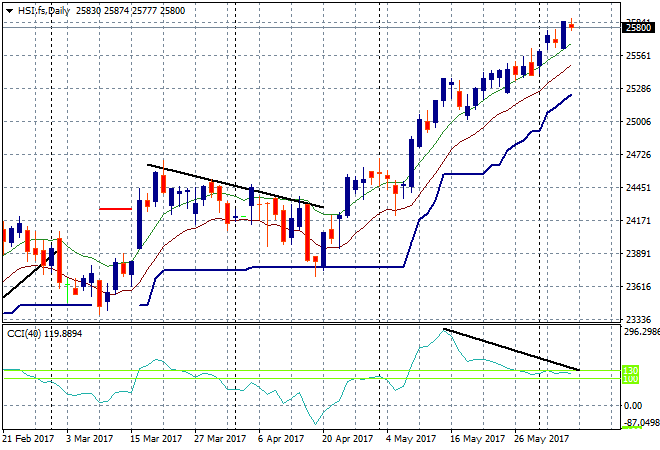

In mainland China the Shanghai Composite is up 1% going into the close at 3133 points, trying to build on its breakout above key support at the 3100 point level. The Hong Kong based Hang Seng Index is off a little after a surge yesterday, down 0.2% to be at 25955 points as momentum tapers slightly. The next target remains the 2015 high at 28000:

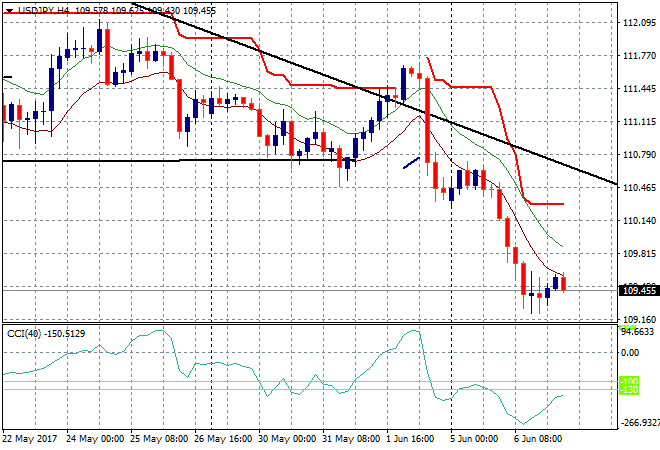

Japanese stocks did okay given the rising Yen, with both major markets putting in a scratch session, the Nikkei 225 settling just below the 20,000 points level as caution reigns. The USDJPY pair had a tiny bounce on the open but has given that all back and remains below the 110 handle with eyes on the previous session lows at the 109.20 level for another breakdown:

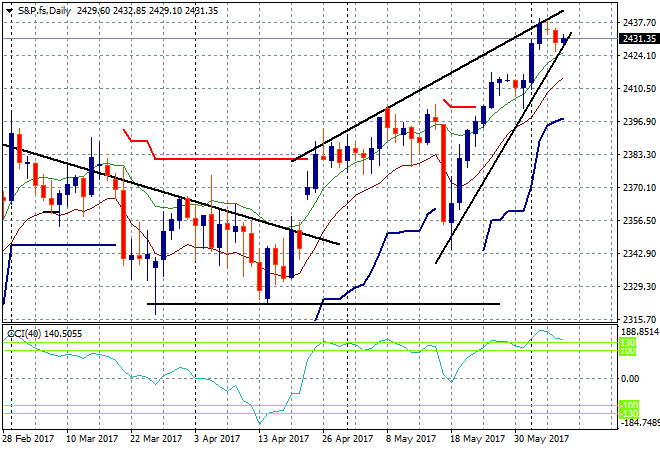

S&P futures are up slightly but I can’t help but see a bearish rising wedge on the daily chart here:

The ASX200 also had a stodgy day after absorbing the GDP print, finishing up 5 points to 5672, as traders weighed up yesterday’s selloff. Banks saw some short covering as they jumped around 0.5% or so across most divisions of Megabank, while commodities sold off to balance out the scratch session.

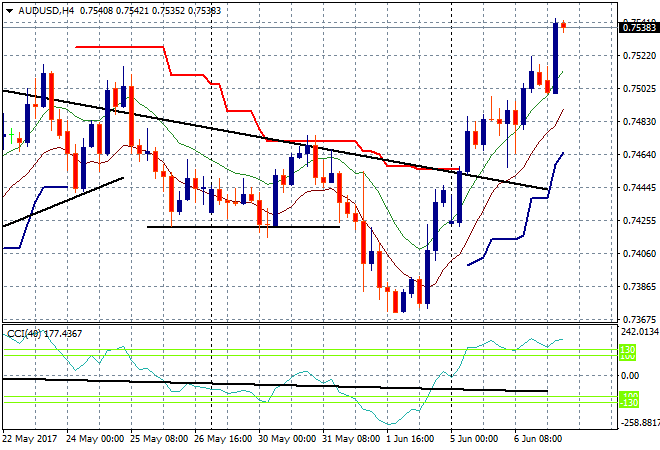

The Aussie dollar is back at its May high well above the 75 handle, with traders loving the RBA hold and the subsequent GDP print, but this is slightly overdone. However, I would not be surprised if the City decides to double down here so 76 or higher is a possibility:

The data calendar starts to ramp up again as we head into the UK election and in Asia tomorrow, the Chinese trade figures. Tonight its relatively calm with German factory orders and the OECD printing its European economic outlook, plus another round of DOE oil inventories.