by Chris Becker

The mixed lead from US and European stocks has not translated into doom and gloom in Asia with most stock markets rising, although today’s Chinese manufacturing PMI saw Chinese stocks and the Aussie dollar take a tumble.

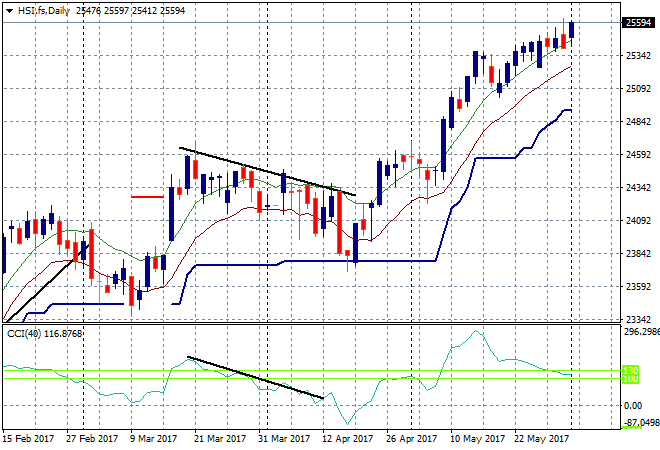

In mainland China the Shanghai Composite fell over 0.5% due to the PMI print, finishing at 3101 points, right on key support and pushing aside – for now – potential breakouts above that level. The Hong Kong based Hang Seng Index went the other way, lifting 0.5% to be at 25787 points, taking another legup in the current reflation trade:

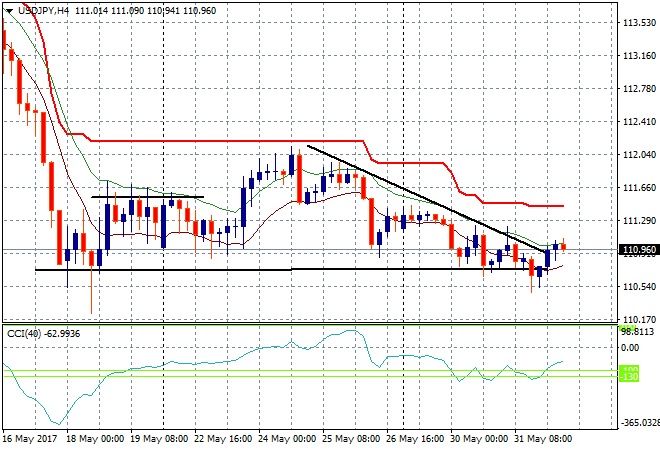

Japanese stocks finally had a good day as Yen weakened slightly, but mainly on good capital spending figures with the Nikkei finishing up 0ver 1% to 19860, still below key resistance at 20,000 points. The USDJPY pair remains somewhat depressed here, but lifting up slightly to the 111 handle and possibly breaking the short term downtrend here:

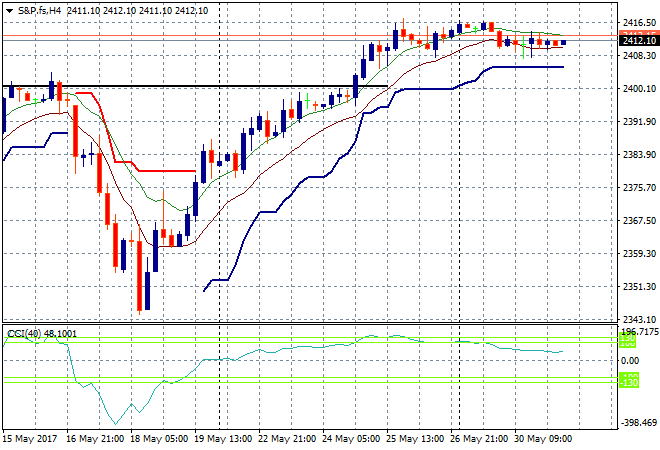

S&P futures are again off slightly and treading water here just above the 2400 point level:

The ASX200 had another poor showing today, barely putting in a scratch session by lifting 0.2% to 5738 points, still well below local resistance at 5800 points. Iron ore stocks took the brunt of the falls on the red side of the list due to the falls in Dalian, with Fortescue off by nearly 4% while financials were relatively stable.

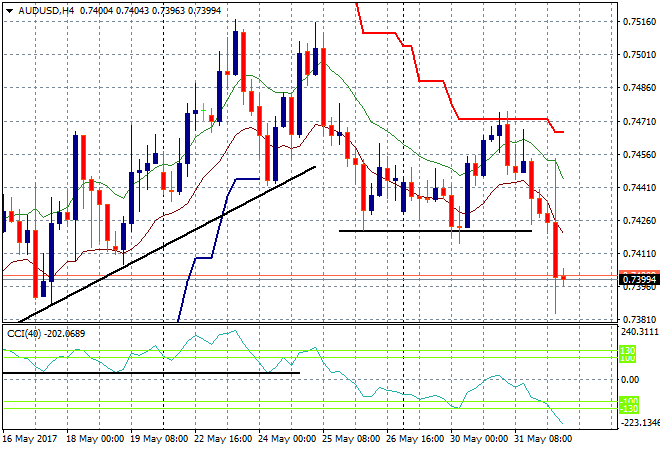

The Aussie dollar had a significant breakdown, flopping straight through the 74 handle and setting up for a potential rout here when the City opens, as realisation crystallises that Australia’s relationship with China is not all one way:

The data calendar tonight includes the US ISM Manufacturing print for May, the preview of tomorrow nights NFP print with initial jobless claims and then DOE crude oil inventories.