Employment came in well above expectations, rising by 42K in May, with upward revisions to prior months’ data. Full-time employment rose strongly by 52.1K, while part-time employment fell by 10.1K. The unemployment rate fell sharply to 5.5% from 5.7%, despite an increase in the labour force participation ratio.

Aggregate hours worked spiked by 1.9% over the month, taking year-ended growth significantly higher to 2.3% from 1.4%. By state, the gains in full-time employment were particularly strong in NSW. This is a welcome development in that:

1. NSW has been recording the weakest full-time employment outcomes in the country for roughly a year.

2. NSW households are the most heavily geared in the country.

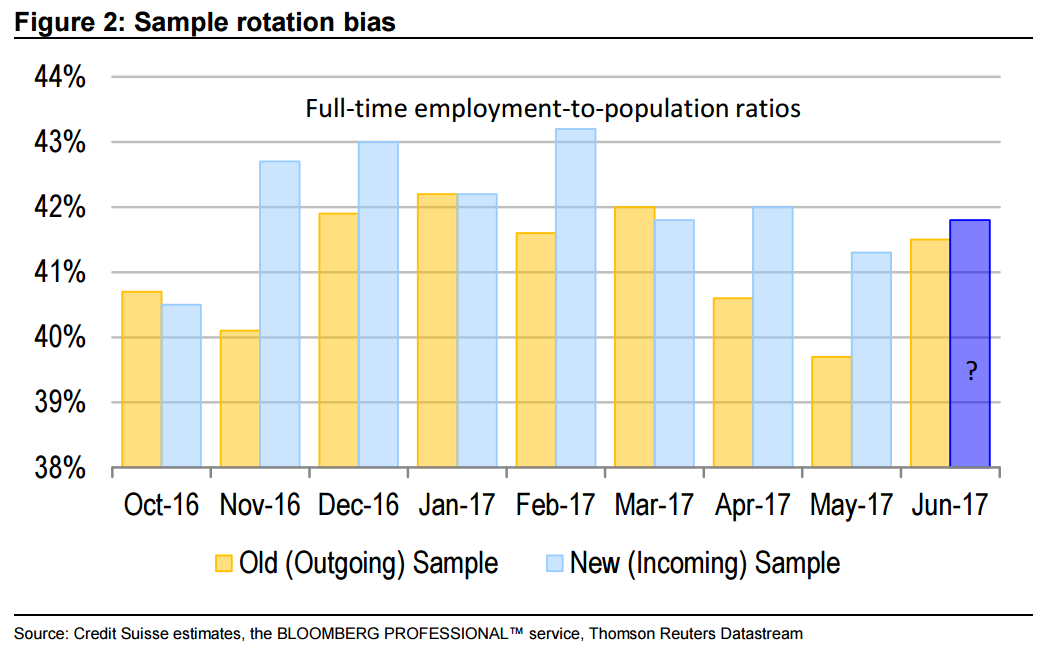

But beware the sample rotation bias

All of this said, the ABS has confessed that for the sixth time in seven months, it has rotated the sample in favour of higher employment-to-population cohorts. Officials report that this has had a material impact on the NSW employment outcomes.

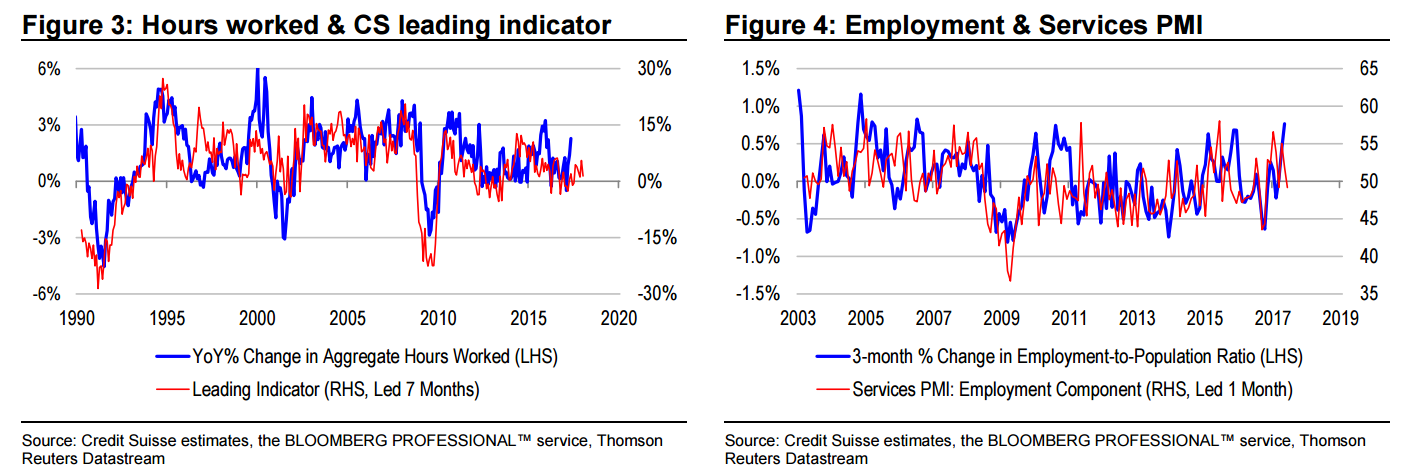

Indeed, the spike in aggregate hours worked looks quite unnatural given the much lower trajectory of our employment leading indicator, based on NAB business confidence, Westpac consumer confidence and trend growth in loan approvals. Also, the spike in employment appears quite far out-of-line with the employment component of the services PMI, which recently entered into contraction territory.

Investment implications

If we follow the data, the next move in interest rates is up, not down. However, there are serious problems with the data from a benchmarking point of view. Net of benchmark revisions, it looks like labour market slack is increasing – not decreasing. Nonetheless, the RBA has a strong macro-stability agenda, to which the flawed, but strong employment data speaks to. On the employment data alone, it is unlikely that the Bank will be cutting rates anytime soon. That said, the Bank is also paying close attention to marketbased signals, such as the slope of the yield curve and commodity prices. Also, weakness in housing indicators may prove more signal than noise. We remain of the view that the RBA will be cutting rates further this year

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.