Following a sharp selloff of US tech shares, concerns about a NASDAQ bubble 2.0 are climbing. Via Societe Generale:

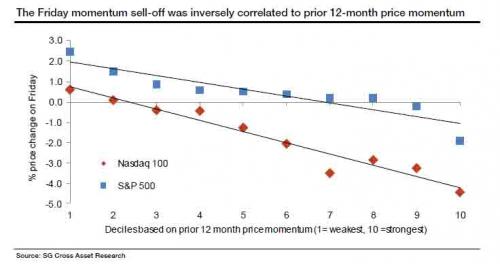

The sell-offs themselves are not particularly unusual, but the uniformity of the prices moves all on the same day indicates a market driven by price chasing momentum, with investors heading for the door all at the same time.

Indeed, those S&P 500 stocks which sold-off on Friday were almost all from the strongest performing decile over the previous 12 months (the r-squared on the S&P 500 line in the chart below is 85%). Within Nasdaq the relationship is even stronger at 95%.

Such a uniform sell-off strikes us as systematic, especially as the relationship weakens once you look at the broader and less liquid Nasdaq composite. For price chasing investors, Friday’s plunge serves as a warning; when it’s time to head for the door, you better move fast.

The chart is striking:

But, via Capital Economics, the valuations are not:

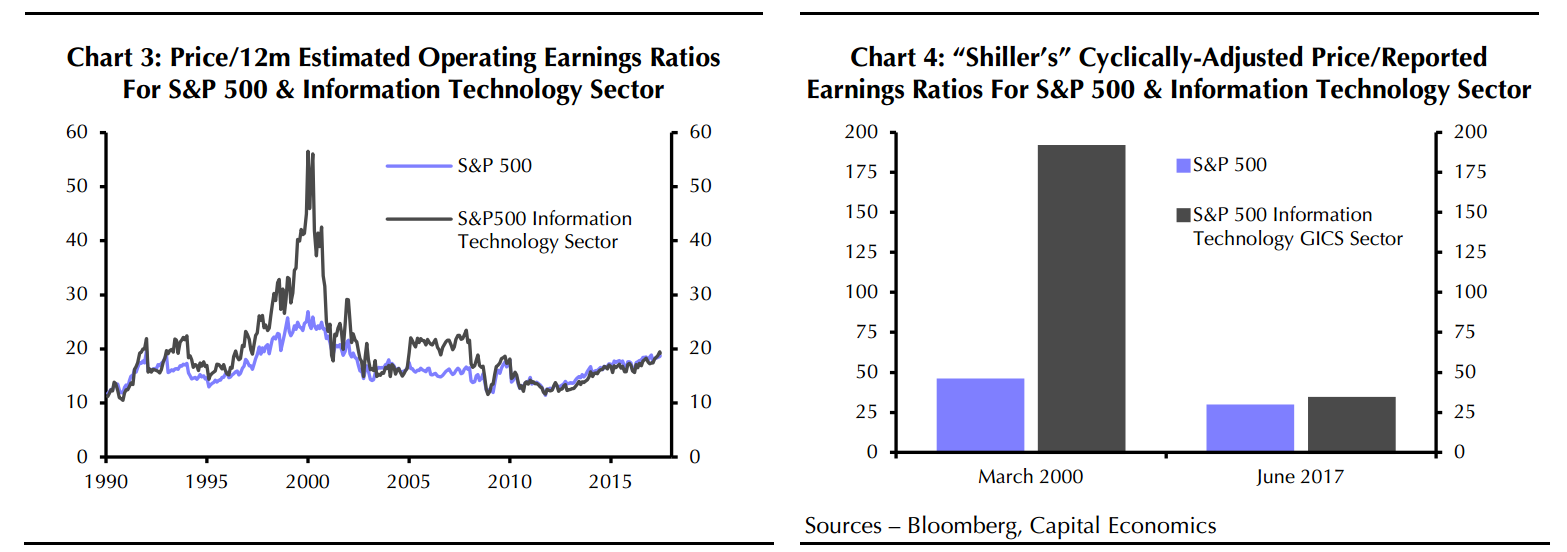

• Some investors are bound to be feeling nervous after Friday’s near-2.5% drop in the NASDAQ 100, given the rout in technology shares during the bursting of the dot com bubble. However, the technology sector is nowhere near as overvalued now. So it is less likely to fall sharply and contribute to a recession.

• Admittedly, the NASDAQ 100 hit a record high last week before its slide, while the S&P 500 technology sector came close its March 2000 peak. What’s more, shares in that sector had previously been performing better since the financial crisis than those in the broader market, just as they had during the late 1990s. This trend had also continued since President Trump was elected.

• Nonetheless, the valuations of shares in the technology sector do not seem to be stretched relative to those in the broader market, based on a comparison of their price/estimated operating earnings ratios. This is quite different to the situation before the dot com bubble burst, when the valuations of technology companies often appeared to have little to do with their ability to generate income. (See Chart 3.)

• Of course, the bears would argue that a price/estimated operating earnings ratio is useless. Better to use a cyclically-adjusted price/earnings ratio, which draws on a decade’s worth of trailing reported earnings, adjusted for inflation. Yet this approach doesn’t lead to a substantially different conclusion. (See Chart 4.)

• To be clear, we are not bullish on the US stock market. On the contrary, our current end-2017 forecast for the S&P 500 of 2,400 is slightly below its current level. But the main reason we expect the market to struggle is cyclical pressure on profit margins. In our view, its valuation is not as stretched as many seem to think.

• If we are right, the stock market is unlikely to collapse under its own weight and contribute to an economic downturn in the way that it did early this century. Instead, we suspect that the next big correction in the stock market will occur in response to the growing risk of a recession. We forecast this correction to be in 2019, when tighter Fed policy should be taking a toll and any fiscal stimulus should have run its course.

I agree. Valuations are a little rich but technology earnings have a terrific tailwind in the secular stagnation context given productivity gains are key to rising profits so what capex there is is likely to headed the way of tech.

That’s not to say that the NASDAQ could not deflate but, again, it would take deteriorating external conditions to do it, such as too much Fed tightening or the Trump fiscal hand-off never coming.