Cross-posted from Investing in Chinese Stocks.

According to CASS data:

The median price of the above cities (Beijing, Shanghai, Guangzhuo) in May were 61685 yuan per square meter, 54458 yuan, 22,273 yuan, respectively, compared with April decreased by 3.2%, 0.4%, 0.5%. Another first-tier cities in Shenzhen, the median price of 50423 yuan per square meter, up 0.5%.

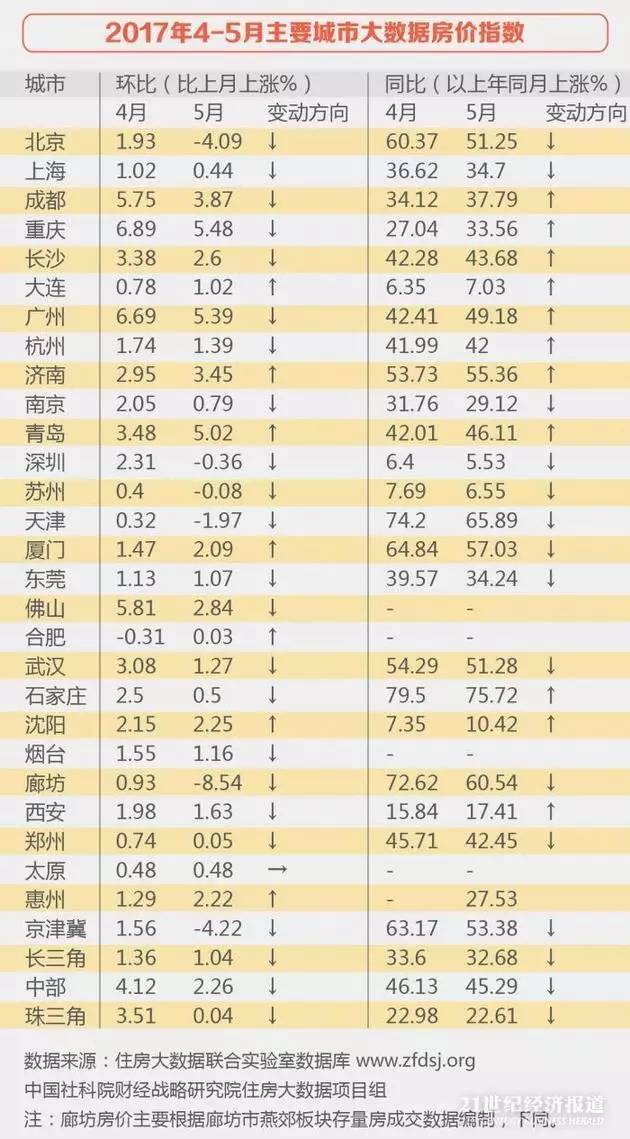

According to this table, Beijing prices are down 4.09 percent, nearby Langfang’s average price fell 8.54 percent. The table also shows year-on-year prices are still upwards of 50 percent in many areas.

Media prices declines are also ugly in surrounding cities:

Some cities in the surrounding areas prices are also declining. In May Tianjin, Shijiazhuang, Foshan, Langfang median home prices were down 4.2%, 0.48%, 9.1%, 8.4%.

This next chart is a plot of home price changes since the start of the year (X-axis) against sales area (Y-axis). The first tier cities are all in the bottom except Guangzhou, while both Shenzhen and Guangzhou prices are down YTD. Many of the “hot” second-tier cities are in the bottom left quadrant: falling sales and falling prices. Other second-tier cities are in the upper right. Sanya is the outlier city with sales growth of almost 100 percen sales and prices down more than 10 percent; Nanchang has soaring prices, but flat sales. The chart is from China Index Academy and Tianfeng Securities Research Institute.

From the current indications, 2017, the mortgage market and then 2016-like surge in the probability of almost zero.

“At present, the national financial and real estate industry regulation, interest rate difference and market demand are playing with each other.As a whole, this year the total amount of bank lending compared to last year, the increase will be shrink.”

Supervision of the year, the market year. Last year, the property market hot, loose credit environment is the main reason. And now mortgage interest rates raised, resulting in increased purchase costs, or will become the development of the property market this year, a key factor in the development.

In fact, because the central bank to tighten liquidity, the bank to obtain capital costs are rising, if you continue to maintain mortgage discount, the bank will be unprofitable. So, if the central bank does not relax monetary policy, the future will be more and more cities to raise mortgage rates. The property market or facing a new era, is the real estate speculators “warm boiled frog.” If you this time, but also hope that the next two years, housing prices rose, and accordingly investment, is likely to fall into the trap of liquidity crunch.

Is this time really different? Maybe for developers. Maybe.

This time is not the same, will developers have a bad second half?

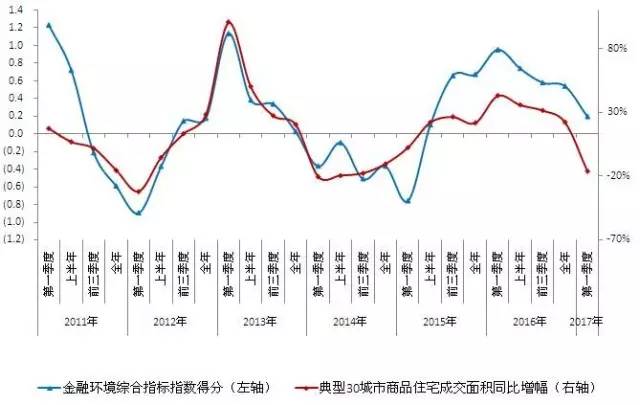

Yiju Property Research Institute has developed a quarterly report to build a China real estate financial environment index. Which includes nine sub-indicators, can generally reflect the real estate industry is facing the monetary policy and the degree of tightness of the capital side.

The real estate financial environment index in China in the first quarter of 2016, is a loose section, then down, the first quarter of 2017 has dropped to normal range, Yi Ju Real Estate Research Institute Vice President Yang Hongxu Is expected to slide in the second half of the tight interval.

The chart of this index from E-house (Yiju) runs from loose (red) to tight (blue). Q1 was normal.

This next chart compares a financial conditions index (green) with sales growth in the top 30 cities (red).

Evergreen real estate Yang Hongxu that the past two rounds of short cycle of experience, the financial environment indicators are not bottomed out, the sales growth will not rebound, or will not be achieved by the negative positive. The past two rounds of sales growth continued for five quarters. This round is expected to last longer may be longer.

Buying restriction could kill the market until 2021:

“In fact, the sale is the property market ‘to the lever’ policy, so that buyers must be for their own purpose for the allocation of funds, or in accordance with the 4-5 year trading cycle, is unlikely to attract highly leveraged high-cost funds to enter.” Central Plains real estate chief analyst Zhang Dawei said bluntly.

Even if the sale of new homes in the restricted cities, may be the first to 2021 before it can be listed on the transaction. A number of industry insiders believe that the sale of a clear blow to speculative investment demand, reduce the investment properties of the real estate market, affecting the real estate speculators the possibility of short-term profit. “For the leveraged investors, the risk is growing.”

The article concludes with a reference to a leaked document from Vanke which definitively says the golden era of real estate is over.

Vanke said the same thing in 2015.

The restrictions are far tighter this time and China’s debt levels all the larger though, so maybe this time really is different. We’ll know in the second-half when the real pain starts hitting. Will governments hold the line or ease at the first sign of major trouble?

iFeng: 楼市爆大消息!这次不一样了 这些人受益最大

Finally,

Hai Tong Securities macro bond analyst Jiang Chao believes that mortgage interest rates soared mainly because the “bank without rice pot.” According to the study, “in 2016, the bank can be in the financial markets through the same industry deposit at 2.8% interest rate, so the 4.9% loan interest rate, even if the mortgage interest rate hit 8 fold is also profitable to the first quarter of this year Interbank deposit rate rose to 4.5%, so the bank mortgage interest rates began to play 9 fold, 95 fold to make up for the cost rise. But in April and May after the bank’s interbank deposits are made, the banks themselves have no money, then how to issue mortgages?”

Jiang Chao believes that the rise in lending rates, loans to shrink, means that the impact of financial leverage will be transferred from the financial market to the real economy. “Credit contraction is the biggest risk in the second half of the year.” In the first half of 17 years, although the economy appears to see signs of falling, but only slow slowdown, because the financial leverage is only in the financial market, mainly for the currency and bond interest rates rise Commercial banks are still expanding, lending rates and loan payments remain stable, but with the shrinking distribution of interbank orders, which means that commercial banks began to shrink, lending rates rose sharply, and the payment of loans began to shrink, which means that The impact of financial deleveraging will be transferred from financial markets to the real economy, and credit contraction will be the biggest risk of the economy in the second half of the year.

A publicly traded bank insider told reporters that the bank mortgage interest rates rise, not only because of the national real estate macro-control factors, may be because “the banks really have no money.” “Banks are still more likely to lend to buyers because mortgages are among the lowest risk classes in bank loans, with low default rates and bad debts, which are fundamentally high quality assets.”

The above-mentioned joint-stock bankers believe that the situation of financial deleveraging, interbank deposit, outsourcing business are in recovery, plus the central bank MPA assessment, the major banks are tightening. “Mortgage rose the fastest, roughly the financial business and interbank deposit business done better bank.”

iFeng: 银行真没钱了 北京首套房贷已基准利率为主优惠绝迹