The common wisdom is that Fed tightening combined with tapering could lead to greater volatility. The reality is far more complex, it is more like a driver shifting gear to adjust his deceleration as he coasts to the red light. If he doesn’t he might just have to hit the brakes hard. An unexpected widening of rate differentials may lead the currency to jump without a follow through in terms of trends so that G10 volatility recedes quickly. An expected widening of rate differentials leads to pressure on EM reserves leading potentially to an eventual shift in their policy stance. This may counter-intuitively encourage inflows initially in some of these countries as their currencies remain stable versus the dollar. In a scenario of limited tapering, the shocks in G10 currency volatility are likely limited and of short duration.

Key points

Quantitative Easing flattens the US Treasury curve. As the curve stabilizes so does implied and then realized volatility before the economy eventually recovers. This forces investors to take on more risk and encourages interest rate to trend lower by encouraging strategies that implicitly sell the odds of a sharp set-back. Tapering on the other hand reverses the risk reward particularly if there is large issuance creating transient shocks higher in interest rates while the curve is driven by growth and inflation expectations over the medium term. Tightening has several impacts on currencies:

1. Quantitative Easing weakens the dollar as interest rates fall

Quantitative Easing discourages foreign reserves from investing in the USD. Initially, they increase their dollar reserves as Emerging Market countries benefit from Fed easing. However, the cost of doing so increases as the US Treasury curve flattens relative to the cost of financing these reserves domestically. As the Fed tightens policy and moves to Quantitative Easing, several scenarios are possible. A. Corporates owing dollars and with local revenues need to tap USD liquidity facilities. This drains foreign reserves especially so if the corporate has poor credit ratings and hence a weak access to international markets. B. In countries that benefit from US growth, the externalities lead to a tightening of policy via a stronger currency and or tighter monetary policy. Those that intervene in the currency market have a tendency to bid the dollar. As their reserves build up above a certain threshold, they are more likely to buy equities rather than diversify out of the dollar.

Foreign investors into the US fixed income market have an incentive to significantly increase their currency hedging ratios as long as the Fed policy stance is easy. The hedged return must also cover the cost of liabilities which is for example around 1 to 1.5% for a Japanese pension fund. As expectations of Fed tightening increase, the cost of hedging increases with it, leading investors to reduce their currency hedging ratios and lower the flow of fixed income investments into the US. This is of course if there is a better alternative. There is little evidence of it.

Should there be Quantitative Easing both at home and abroad, there is eventually little difference for a fixed income investor between the two markets. The differences are driven primarily by growth expectations, the distance to potential growth and the speed of repair of tainted balance sheets. In addition, fiscal measures can change this speed, initially worsening the crisis in the Eurozone while the reverse was true in the United States. When one central bank tightens ahead of the other, interest rate differentials only become relevant if the cost of hedging increases too much and if the market can detect a clear trend.

Ex ante the above mechanism, equity flows dominate currency movements as they are largely unhedged with typical hedging ratios around 20% for long-term investors. These flow to the country that is more advanced in its easing cycle to take advantage of cheaper valuation and the expected recovery in growth and earnings. These are initially driven higher by low wage pressure given slack in the labor market. These equity flows move naturally to the country with the higher growth rate.

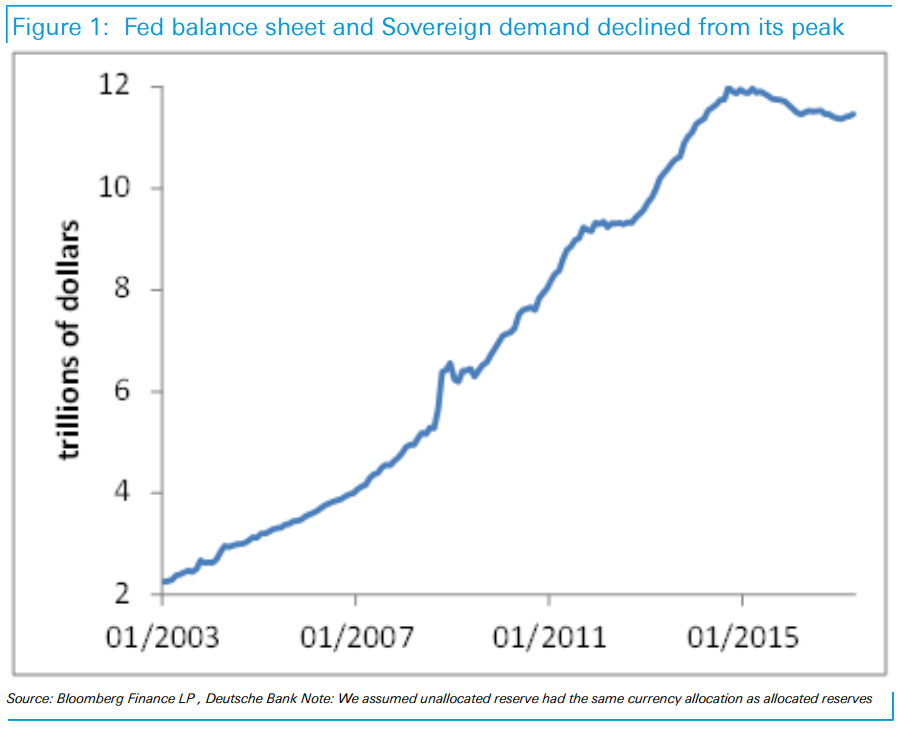

Foreign reserves are the last mechanism at play. In periods of large scale EM inflows, they cap the value of their currencies and their growing reserves flatten the US Treasury curve. However, this series of impulses eventually dissipates, as growth and inflation expectations still drive the US Treasury curve over the medium-term. Given that foreign reserves have been declining since September 2014, the impulse on the US Treasury curve has clearly been negative with little lasting impact (see Chart 1). As foreign reserves see outflows and keep a short duration, they are likely to concentrate their assets in dollars rather than diversify into other currencies.

2. Trends and ranges reinforce themselves. Given a rate differential between the two countries, currency trends will tend to form as the risk reward and particularly so if the central bank or a reserve manager skewed the risk reward by intervening. Interest rate differentials between the two countries lead to trends over time while in their absence range trading set in. This is reinforced by the selling of derivative structures whose hedging reinforces the existing spot range or trend. This increases the potential return and hence leverage needed by spot strategies to achieve the desired but declining return to risk ratio.

3. Trends and ranges reinforce themselves. Given a sufficiently wide interest rate differential between the two countries, currency trends will tend to form. This is particularly so if the central bank or a reserve manager skews the risk reward by intervention, QE or tapering. Interest rate differentials between the two countries lead to currency trends over time if the market does not anticipate it or jumps if it does. This is reinforced by the selling of derivative structures whose hedging reinforces the existing spot trend or conversely range. This increases the potential return of trend or spot strategies and hence the leverage needed to achieve the desired but declining return to risk ratio.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.