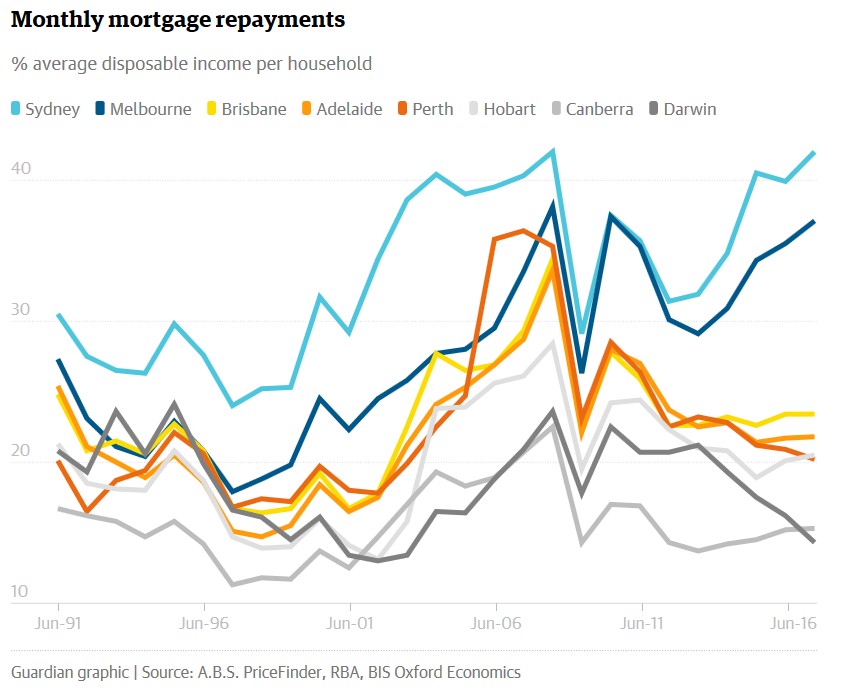

BIS Oxford Economics has done some interesting analysis for The Guardian showing that Sydney’s mortgage affordability is now the equal worst on record, with Melbourne’s just below 2008’s record low, driven primarily by housing investors:

As of December 2016, 42% of the average disposable income of a New South Wales household was swallowed up by monthly mortgage payments on a median-priced house in the capital – after a 25% deposit.

It was the same in 2008, still the highwater mark of housing unaffordability in all but one Australian capital.

Melbourne at 37.1% in December was forbidding but it was worse there in 2008 (38.1%) and 2010 (37.4%)…

Richard Robinson, senior economist for BIS Oxford, says the affordability problem, most acute in Sydney and Melbourne, is mainly a story of “wealthy people investing in property and driving up price and demand”…

Phasing out negative gearing to stop investors writing off rental losses on multiple properties against their income, and tax discounts on capital gains, Robinson says, are key to “deflating the bubble slowly before it goes pop”.

The Turnbull government has resisted calls for such moves, leaving in place what Robinson calls the world’s most “generous tax breaks for residential property”.

“To me, that’s where all our savings have gone.”

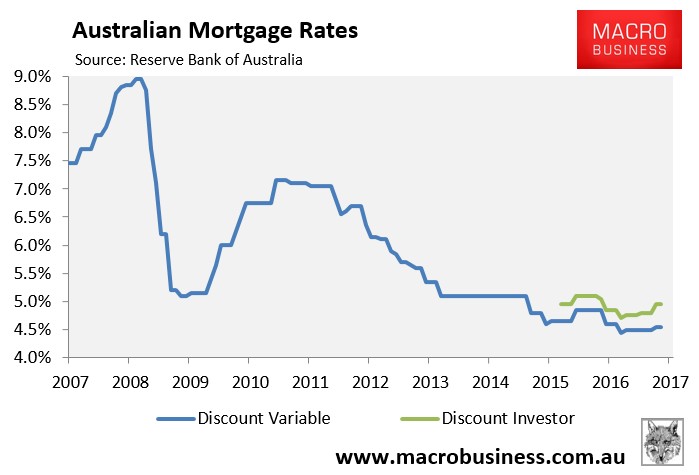

That’s quite an extraordinary result given discount variable mortgage rates have fallen from 8.95% in August 2008 to 4.55% currently:

Advertisement

With interest rates approaching a lower bound, you don’t have to be a rocket scientist to see that there’s little scope to ease mortgage pressures and that Australia’s indebted mortgage slaves are highly vulnerable. Moreover, even a small rise in mortgage rates could spell doom for a significant proportion of borrowers.

Bur rather than take BIS’ advice and unwind negative gearing and the CGT discount, the Turnbull Government – in concert with the NSW and Victorian State Governments – is instead seeking to pump first home buyer demand and blow more air into the bubble.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.