Yesterday S&P released a new report comparing Australia and Canada, explaining why it sees the former as a much weaker AAA sovereign than the latter.

Strong Institutions And Governance Effectiveness

We consider Australia and Canada’s institutional arrangements and governance effectiveness to be key strengths. Both countries are federal parliamentary democracies supported by strong institutions and the rule of law. They share a monarch, Queen Elizabeth II, who reigns but does not rule. Both have made peaceful transitions to nationhood from their British colonial origins. Similar to other ‘AAA’ rated sovereigns, they are both well-governed, with predictable economic policies and social stability. We expect these factors to continue to help support robust, diversified economic growth during the medium term and enable policymakers to respond in a timely way to economic shocks. Their similar histories, institutions, and political cultures reflect their common roots in Britain’s parliamentary system and English common law–except for civil legal matters in Canada’s French-speaking province of Quebec, which was a French colony. Similar to the ‘AAA’ rated sovereigns in Europe, there is considerable public participation in policy debates. In both countries, we expect political stability and continuity in key economic and other policies, despite changes in government. In line with our assessment, Australia and Canada rank highly on international governance and development indicators (table 2).

Similarly Strong Economic And Monetary Profiles

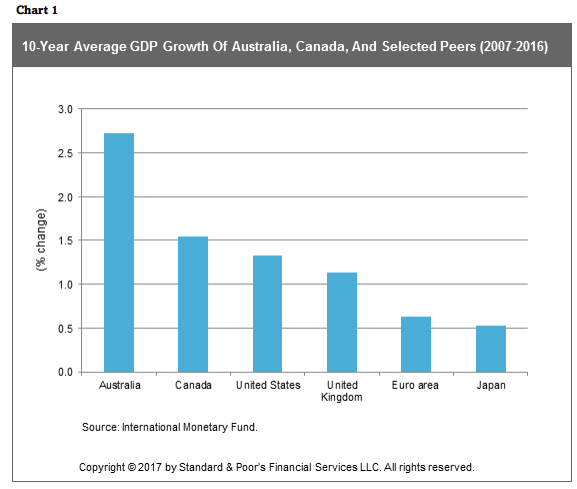

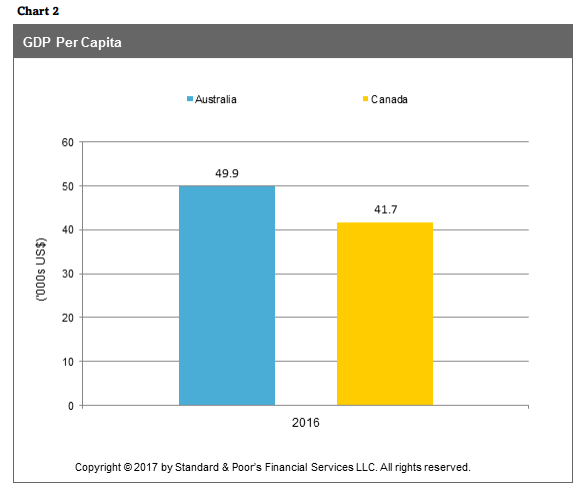

We view the economic and monetary profiles of Australia and Canada as strong, which we believe enhances the two sovereigns’ resilience to economic shocks. Both countries have strong, prosperous, and open economies, most clearly demonstrated by their high per capita incomes (chart 1). Australia and Canada’s favorable performance compared with most other advanced economies during the current century demonstrates their economic resilience. Australia’s annual growth rate during 2000-2016 averaged 2.7%, exceeding that of all ‘AAA’ sovereigns except for small countries such as Hong Kong, Singapore, and Luxembourg. Canada’s average annual GDP growth rate was also relatively high during the same period, at 2.1%, compared with 1.9% in Germany and 2% in the U.S. Australia and Canada performed well after the financial crisis that started in 2008. Australia was the only ‘AAA’ rated sovereign that maintained positive growth in 2009, with GDP expanding 1.8%, down from 2.6% in 2008. All the other countries suffered a contraction. The Canadian economy contracted 3% in 2009, but resumed growth of 3% the following year Australia and Canada’s relatively favorable economic performance after the 2008 financial crisis partly reflects the proactive policymaking at the time. Australia’s better performance likely also reflects its different trade linkages. Canada’s economic growth was affected heavily by its trade exposure to the U.S., while Australia benefited from its high trade exposure to rapidly growing China. Australia’s economic growth was supported by a large mining investment pipeline that was already in existence at the time due to China’s effect on surging commodity prices.

Being relatively small, open economies, Australia and Canada remain exposed to downturns in the global economy. With China’s medium-term growth outlook now one of the major risks to the global economy, Australia’s high trade exposure to China could become a weakness; it is likely to suffer more than Canada and many other economies from any major downturn in China’s growth. That said, our earlier analysis suggests that Australia and Canada could suffer a ratings downgrade in a China ‘hard-landing’ scenario (see “Stress Scenario Analysis: What Would Happen To Ratings Globally If China’s Growth Halved?” published May 4, 2016).

Healthy banking systems also helped the Australian and Canadian economies to perform relatively well following the 2008 financial crisis. We believe both nation’s banking systems remain sound. We place the Australian and Canadian banking systems on the lower end of our scale of banking system risks. In our Banking Industry Country Risk Assessment (BICRA), we assign Canada as ‘Group 2’ and Australia as ‘Group 3’ (on a scale of ‘1’ to ’10’, with ‘Group 1′ being the lowest-risk–a group to which no country is currently assigned. See “Banking Industry Country Risk Assessment Update: May 2017,” May 5, 2017).

That said, we believe risks could be rising in both countries, albeit from a low level, due to high and rising household indebtedness and strong growth in property prices. These developments raise the risk of abrupt adjustments in household employment and incomes, or house prices, or all concurrently, leading to consumer hardship and potential asset-quality problems for lenders. In Canada, we assign a negative trend on the “economic risk” component of our BICRA assessment, for these reasons, and we recently increased our assessment of economic risks facing Australia’s banks for similar reasons (until May 22, 2017, we placed Australia in “Group 2,” alongside Canada). However, the major banks in both Australia and Canada are adequately capitalized, in our opinion. In addition, banks in both countries apply sound lending practices, supported by conservative regulatory standards and strong regulatory oversight, and therefore should be well placed to respond if there were unexpected downturns in their respective housing markets or broader national economies. A key difference between Australia and Canada’s banking systems, though, is their exposure to external vulnerabilities; Australian banks operate in an economic environment exposed to material external sensitivities, reflected in persistent current account deficits and high external debt, while Canada’s current account deficits are balanced by the country’s overall net external asset position. In addition, Australian banks are materially reliant on offshore wholesale funding, while Canada’s banks, though they also access foreign funding, are, by a slim margin, net external creditors.

Australia and Canada’s strong monetary flexibility provides them with important economic buffers. These buffers were starkly exemplified during the 2008 financial crises, when both nations’ exchange rates depreciated sharply and their central banks aggressively loosened monetary policy to support their economies.

Both countries operate free-floating exchange-rate regimes that can adjust quickly to economic developments and absorb some of the effects of an economic shock by boosting trade competitiveness. We believe the buffer works well because both countries have diversified economies that enable enhanced trade competitiveness to genuinely assist economic growth, and little unhedged foreign-currency debt to create adverse balance-sheet issues. And these currencies are both actively traded, limiting the risk of disorderly price movements or stalled trading in illiquid markets. Indeed, the Australian dollar and Canadian dollar represent small but significant shares of official foreign-exchange reserves. The Australian dollar represented 1.8% of total allocated reserves and the Canadian dollar 2.0% as of December 2016. These shares have risen substantially in recent years as central bank reserve managers have diversified their portfolios, and indicate strong market confidence in the currencies. However, neither currency has reached “reserve currency status,” which we define as currencies representing at least 3% of allocated reserves.

Monetary flexibility is augmented by long track records in both countries of successful inflation targeting by independent central banks. The Reserve Bank of Australia and the Bank of Canada adopted inflation targets in the early 1990s, and average inflation has remained within the RBA’s 2% to 3% target and the BOC’s 1% to 3% target during the economic cycles since then. This has led to well-anchored inflation expectations and provides the RBA and the BOC high credibility and flexibility to enact countercyclical monetary policy in times of economic shocks.

Divergent External And Fiscal Profiles

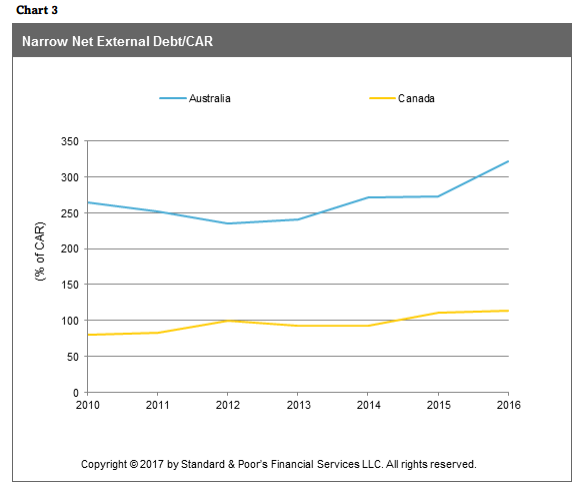

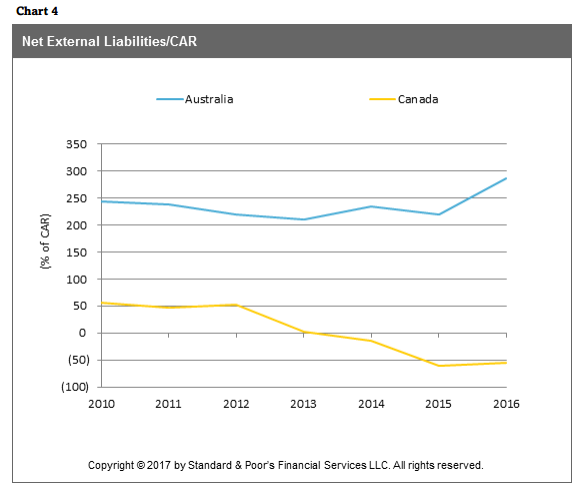

The biggest difference between Australia and Canada is their external profiles. Australia’s external profile is much weaker than Canada’s, and is far and away the weakest of any ‘AAA’ sovereign. Canada has a much lower level of narrow net external debt than Australia. Furthermore, Canada is in a net asset position when all external assets and liabilities (i.e., direct investments and equity investments) are taken into account.

In both countries, though, current account deficits are sizeable. Australia has a much longer history of running current account deficits than Canada, however, leading to a weaker external balance sheet. And with Australia’s banking system carrying most of this external debt, we believe Australia’s economy is much more vulnerable than Canada’s to any major shift in the willingness of foreign investors to provide funding.

We believe Australia’s government finances, more so than Canada’s, need to remain strong to balance the country’s external vulnerability, especially that of the banking system, for the sovereign’s overall profile to remain consistent with a ‘AAA’ rating.

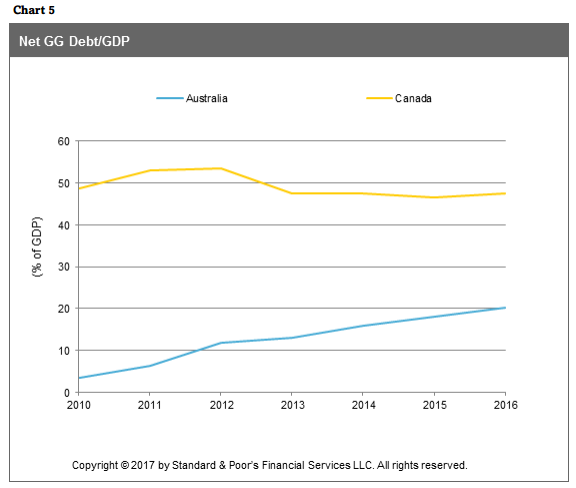

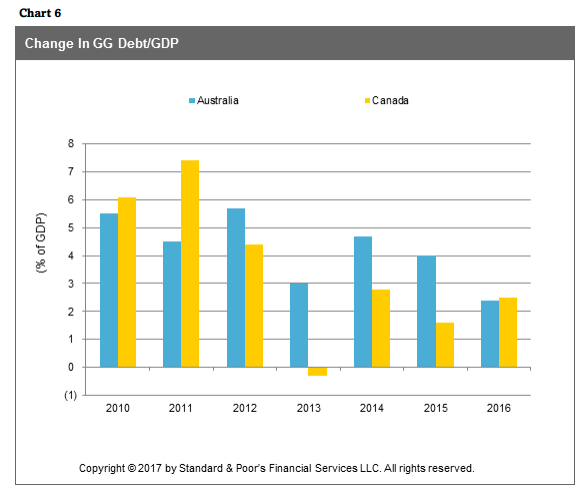

Australia remains in a lower government debt position than Canada, but fiscal performance has been slipping and is now weaker than Canada’s. This fiscal slippage has occurred in Australia, despite government intentions to reach budget surpluses since fiscal 2013, because of sharp falls in the prices of Australia’s key export commodities since their peak in 2011. This significant delay in improving fiscal performance, and the risk of further delays, prompted us to place the rating on negative outlook in July 2016.

More broadly, we believe there is a broad consensus in both countries for prudent fiscal policy, which will likely keep fiscal deficits and government debt low to moderate. This was particularly evident in both countries in the decade or so before 2008, when revenue growth was relatively favorable. In Australia, the central government entered the 2008 financial crisis with budget surpluses and negative net debt, having used some of the windfall gains of the earlier commodity price boom to pay off debt. Canada’s fiscal adjustment began in 1994; the general government primary balance improved by 10 percentage points of GDP between 1993 and 2000 and, similar to Australia, the federal government ran budget surpluses for 11 consecutive years up to fiscal 2008. Improvements in fiscal performance led us to raise our sovereign ratings on Australia and Canada to ‘AAA’ in the early 2000s.

There’s only one reason to write this report beyond academic interest. S&P is preparing the ground to downgrade Australia. It will come later this year as Morrison’s fiscal fantasy falls apart with the iron ore price.

Moreover, given the response to the recent bank downgrade, I think it likely that a sovereign downgrade will lift Australian funding costs materially.

Advertisement

It will also be the death knell of the Coalition Government as its key brand of budget management disintegrates into a cascade of downgrades for it, every state budget, every local government, the big five banks and the many government corporations around the country.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.