Global equities have hit fresh highs, and the ASX200 is close to a nine-year peak. Equities should, of course, trend up over time as earnings tend to rise. But we’re concerned at present, and see a dip (ie, 5%+) coming, for several reasons.

Valuations are elevated. The global PE ratio is close to 15-year peak, while Australia’s non-resources PE has jumped to 17¼x – the highest level since 2002. Further, the Australian PE has been remarkably stable over the past couple of years – its volatility is around record lows. We’re not sure that can last.

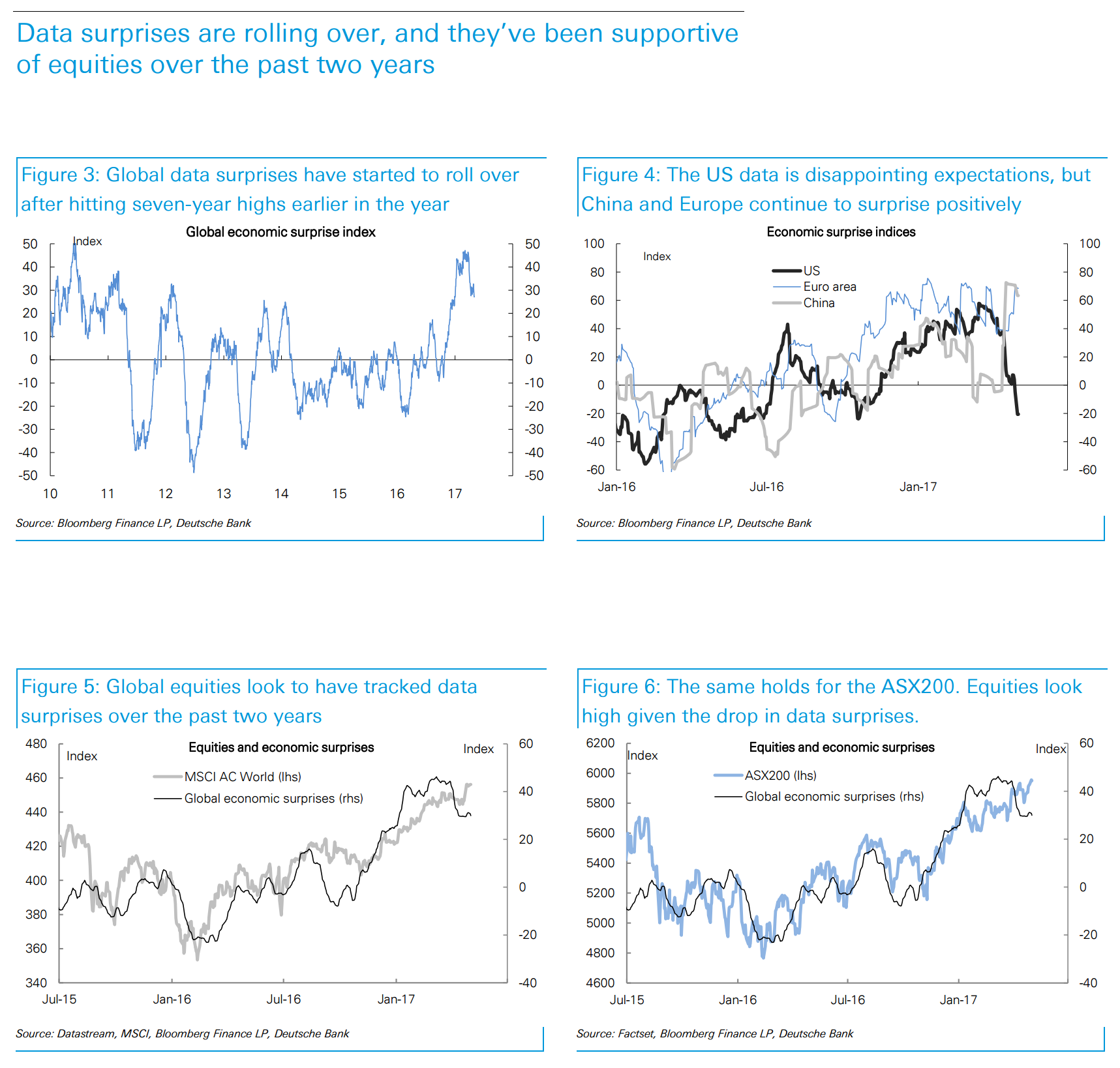

Data surprises are rolling over. Equities could struggle without the sugarhit of consistently above-consensus macro data. Both global and Australian equities have followed data surprises over the past 18 months, and there looks to be downside risk.

Earnings revisions look to be peaking. Both globally and Australia, earnings revision ratios have hit net upgrade territory – the highest since the GFC recovery. They rarely stay at these levels for long, unless the cycle is particularly strong, or earnings are recovering from a downturn. As with data surprises, normalisation of earnings revisions could remove a plank of support for equities. We also note that our Profit Pulse, a real-time tracker of earnings, appears to have peaked.

May is a key month for company trading updates. Some have already been soft (Pact, Coke, Star, Vocus) and we expect more in that vein given the soft consumer backdrop and poor weather in April.

So what to do? The obvious – lean defensive, particularly since defensive stocks are a little cheap relative to the past few years. We add to our weight in defensive names, at the expense of cyclical industrials. Our key picks are: AGL (strong earnings momentum on higher power prices), APA (continued investment opportunities in gas infrastructure), Suncorp (cheap vs peers, Qld exposure), Woolworths (churning out decent growth in a soft environment). We remain overweight banks and resources – these sectors have a lower correlation to the market than industrials, as they tend to follow their own cycle.

I don’t agree with Tim Baker on much and today is no exception. Banks and miners? Cripes. If there is one relative certainty about the second half it is that China is going to slow and iron ore fall. That may or may not derail broader equity markets but it virtually guarantees Australian under-performance versus other bourses as miners re-rate lower and fully valued banks are shunted as housing slows into falling income.

If you’re sick of local fund managers that only swim in the cracked local fish bowl and would like to expand your investment horizons then the MB Fund (launching in the next month with 70% international stocks) is for you.

Register your interest today (if you have not already):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.