Opposition Leader, Bill Shorten, has copped criticism over estimates that retaining the temporary deficit levy and restricting an increase in the Medicare levy to incomes above $87,000 would yield revenue of $7.8 billion over four years. According to Labor, the deficit levy would raise $1.85 billion in 2018-19, but Liberal Democratic senator, David Leyonhjelm, has disputed these costings, noting that the deficit levy is slated to be abolished from July 2017. However, the Opposition says the Government could still extend the levy, particularly if the Medicare levy increase is rejected by the Senate. From The Australian:

Liberal Democratic senator David Leyonhjelm yesterday called out the Labor costings as disingenuous. He said it was “misleading budgeting” because Labor had no way of extending the deficit levy from opposition.

He also noted the impost on high-income earners was due to be lifted from July 1, asking whether Labor planned to reimpose the deficit levy with a retrospective start date if it won government.

“Labor’s very keen on high taxation and they are convinced that this class-war approach of tax the rich is electorally appealing,” he told The Australian. “It suits their purposes to criticise the government for removing the tax on high income people. And presumably they don’t want to admit that reimposing a tax would be required for their budgeting to be accurate … $1.8bn is still a fairly big blackhole.”

Labor argues its costings are relevant because the government could still decide to extend the deficit levy. It also says a Senate rejection of the government’s across-the-board increase to the Medicare Levy could bring an extension of the deficit levy back into play.

Meanwhile, Labor’s call for the 2% deficit repair levy to be made permanent has sparked concern among tax planners and accountants. Retention of the levy would create an ongoing top marginal tax rate of 49.5%, creating a gap of almost 20% between the top income tax rate and the company tax rate. Greg Travers of William Buck Chartered Accountants says it is likely that some high-income earners will consider tax avoidance initiatives as a consequence, noting that this will further add to the Australian Tax Office’s costs in tackling tax avoidance. From The AFR:

“This means some high income earners – not all – will seek to avoid paying tax at 49.5 per cent,” [Greg Travers] said.

“Retaining the debt levy will increase the incentive to try and tax plan, which can evolve into tax avoidance, and will only increase the problem. The irony is this will make negative gearing even more attractive”…

A large difference between income and company taxes creates a “significant bias” towards trapping profits at the corporate rate, even when those funds are used personally by shareholders, said BDO tax partner Mark Molesworth.

“Taking the two rates further apart will … only exacerbate the problem.”

Terry Hayes, senior tax analyst, Thomson Reuters, notes that the trend of the past few decades to narrow the gap between the top personal rate and company taxes seems to be sliding into reverse.

“The gap is set to grow to 20 percentage points or more,” he said.

“[This] can become fertile ground for tax planning…”

Small business owners have also had a dig at Shorten, warning that companies will consider relocating offshore if a future Labor government winds back the recently announced tax cuts for companies with turnover of up to $50m. From The Australian:

Ms Melbourne is a co-founder and executive director of Intelledox, a software exporting company with an annual turnover of about $10m. It employs 35 people in Australia as well as 14 others spread across Singapore and North America.

She is calling on the Opposition Leader to support the government’s small business tax cuts, arguing that bipartisan support for the extra relief will provide certainty for the sector and help boost Australian competitiveness.

“We’re under pressure to move our business offshore to places like Singapore or Silicon Valley where the tax conditions are significantly more favourable,” Ms Melbourne said.

“We’re proudly an Australian company employing Australians. We want to keep our IP here in Australia, but we are anxious to get some clarity around this conversation. It will enable us to invest confidently in our own business and I know there is a raft of other businesses — certainly in the innovation sector — who feel the same.”

It is worth pointing-out the contradictions above.

First, the accountants quoted in the second article argue that Labor’s plan to raise the top marginal tax rate will push people towards negative gearing, but fail to mention that Labor also plans to close negative gearing to investors in existing dwellings (where more than 90% of investors currently invest). Thus, this claim is a bit of a non-argument.

Second, the accountants claim that Labor’s plan to raise the top marginal tax rate would raise the gap between personal and company tax rates by so much that it would foster tax planning. But again, they fail to mention that Labor would also unwind the Coalition’s recent cuts to the company tax rate for businesses with turnover up to $50 million, and would oppose extending company tax cuts to all businesses within a decade, as proposed by the Coalition.

Thus, there are swings and roundabouts with Labor’s policy, and the Coalition’s company tax cut agenda would equally widen the gap between personal and corporate taxes, leading to greater incentives to engage in tax planning.

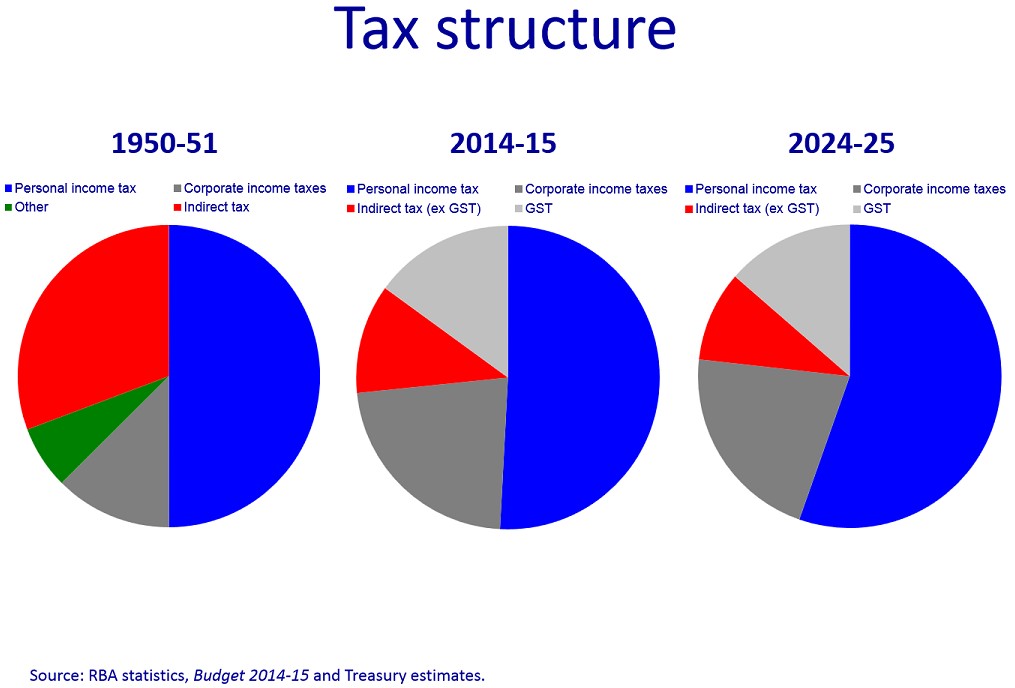

One area where I do agree with the above commentators is the argument that Australia’s tax system is becoming far too reliant on personal income taxes. As shown in the below Treasury chart, Australia is just as reliant on income and profits taxes as it was in the 1950s, and will become more so over the coming decade as bracket creep (aka “fiscal drag”) increases workers’ tax burdens:

Ultimately, genuine tax reform requires broadening the tax base and building it around more efficient and equitable sources. It also requires unwinding Australia’s many world-beating tax concessions (e.g. superannuation, negative gearing and capital gains tax discounts, and fringe benefits), which cost the Budget billions of dollars in foregone revenue and are skewed towards the wealthy and higher income earners.

Sadly, neither Labor or the Coalition have offered comprehensive plans for tax reform, and have instead offered piecemeal measures – Labor on negative gearing and the CGT discount and the Coalition on company taxes.

The end result is that instead of trying to broaden the tax base, both sides are doing the opposite by relying on never-ending increases in personal income tax via bracket creep, while the base of workers shrinks as the population ages and the proportion of retirees rises.