The Reserve Bank of New Zealand (RBNZ) has released its bi-annual Financial Stability Report (FSR), which once again dissects the nation’s (read Auckland’s) housing bubble and warns on risks to financial stability and the macro economy. Below are the key extracts pertaining to the housing market:

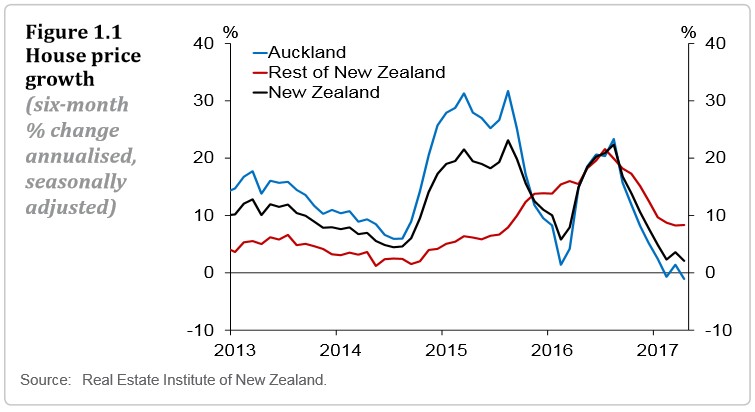

House price growth has slowed in the past eight months (figure 1.1). This reflects several factors: the Reserve Bank imposed tighter loan-to-value ratio (LVR) requirements on lending to property investors in October 2016; banks have tightened serviceability criteria and increased mortgage interest rates; and affordability pressures are constraining prices in parts of the country. Household credit growth has fallen, but remains high at around 8 percent per annum. Household indebtedness continues to increase in relation to incomes.

The outlook for the housing market remains uncertain. While building activity has increased in recent years, the rate of house building remains insufficient to meet rapid population growth and address existing housing shortages. Mortgage interest rates also remain low, despite recent increases. A further resurgence in house prices would be of real concern, given existing affordability constraints.

The LVR policy has improved the resilience of the banking system to a correction in the housing market. However, a significant share of households has taken on loans at high debt-to-income (DTI) ratios and appear to be vulnerable to an increase in interest rates or a decline in income. An economic downturn could materially weaken the financial position of these households, which could exacerbate a fall in house prices if they are forced to sell their properties…

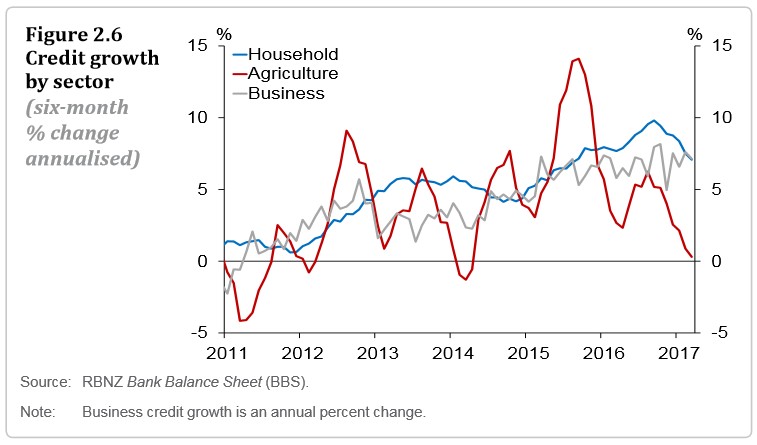

In the six months to March, housing credit grew at an annualised pace of 7 percent, compared to 10 percent in the six months to September (figure 2.6). The slowdown is due to a combination of factors, including higher mortgage interest rates and a tightening of high-LVR lending restrictions. Consumer credit growth has picked up, increasing 5 percent in the year to March, but it remains just 4 percent of total credit…

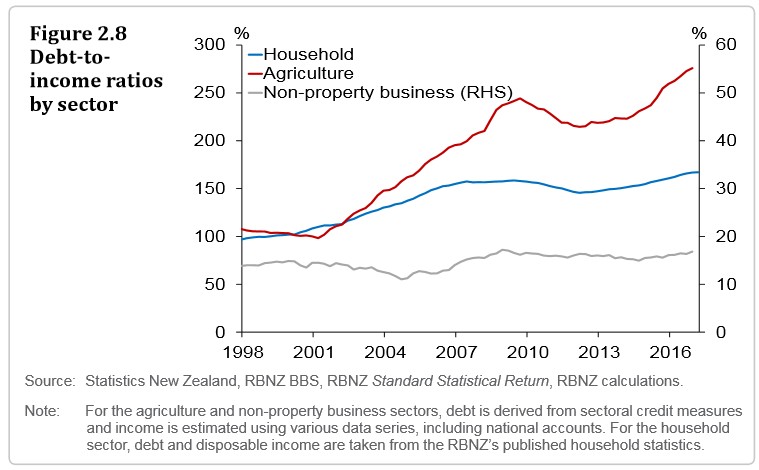

Household debt-to-disposable income rose to 167 percent in March, and debt has also increased as a proportion of income in the agriculture sector (figure 2.8). While low interest rates have eased debt serviceability burdens, higher indebtedness has made borrowers more vulnerable to a sharp rise in interest rates or a fall in incomes…

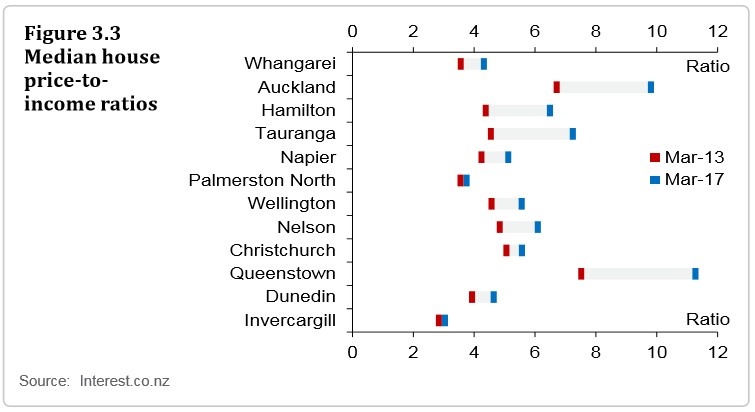

House prices, however, remain overvalued in many parts of the country on key metrics, and there remains the risk of a sharp correction. Prices are particularly stretched in Auckland and some surrounding cities, where price-to-income ratios have increased substantially (figure 3.3). Prices have also become more stretched relative to rents in the past year: although, nationwide, average rents grew at 4 percent in the year to April, house prices grew at twice that rate. Rental yields are near record lows…

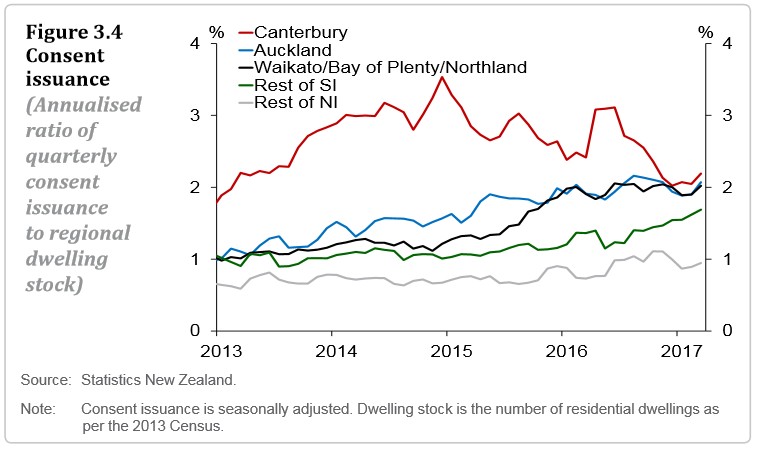

High house price and rental price growth reflects strong demand for housing relative to supply. This is, in part, driven by high levels of migration. Over 60,000 more people of working age moved to New Zealand than left in the year to April. Supply has been slow to respond to population growth, particularly in Auckland where about half of new migrants have settled. Building activity has picked up over the past two years, but the level of consent issuance in Auckland is still likely to be insufficient to accommodate population growth and address existing housing shortages (figure 3.4)…

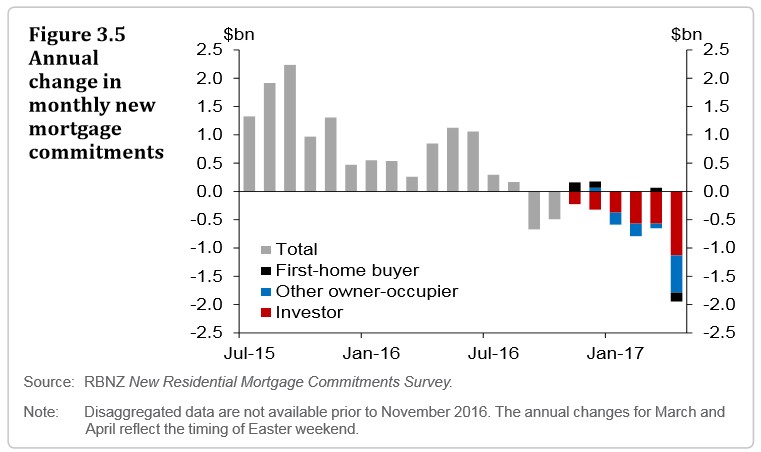

Household credit grew by around 8 percent in the year to March. However, new mortgage lending has fallen in recent months: in the three months to April, banks wrote $3.3 billion less in mortgages than in the same period a year before (figure 3.5). Lending against investment property fell particularly sharply, with investor lending now comprising around 35 percent of new mortgage lending, compared to 42 percent in April 2016.

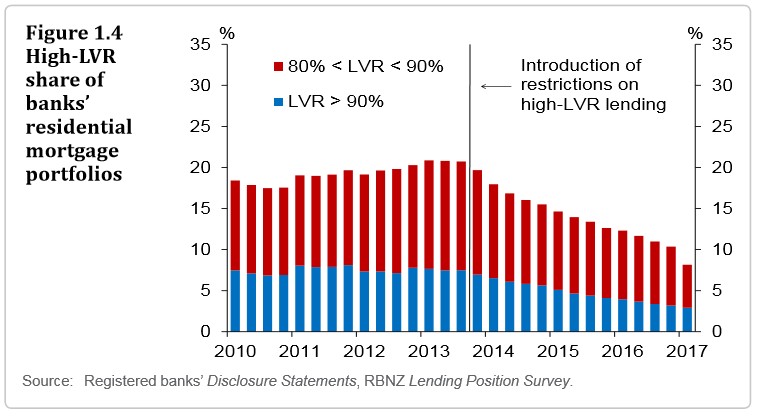

Banks have disproportionately reduced lending to riskier borrower classes, partly in response to the Reserve Bank’s tightening of LVR restrictions in October 2016. In the year to April 2017, the share of total new mortgage lending to investors with LVRs above 60 percent has halved. The share of new mortgage lending to owner-occupiers with high LVRs has also remained low. These developments have helped to further reduce the stock of high-LVR lending on banks’ balance sheets, increasing banks’ resilience to housing market risks…

Despite the recent slowdown in house price growth and new mortgage lending, many households remain heavily indebted. The household debt-to-disposable income ratio has increased to 167 percent, above its peak of 159 percent in 2009. Low interest rates have kept this debt level manageable, but many households are vulnerable to an increase in interest rates.

Auckland households are particularly vulnerable, as they are more indebted relative to incomes than households in the rest of New Zealand. The concentration of debt in Auckland is also particularly concerning given that Auckland house prices are at a heightened risk of a sharp correction, due to the particularly large price increases in recent years…

An increase in the share of borrowers with high debt-to-income (DTI) ratios has contributed to the increase in aggregate household indebtedness. These borrowers are vulnerable to debt servicing shocks, such as higher interest rates or a fall in income. This makes them more likely to default on their mortgage or cut consumption sharply, and makes them more likely to sell their house to repay their mortgage, in response to mortgage affordability shocks. If a significant proportion of households have debt burdens that are unsustainable in the event of an affordability shock, financial stability could be threatened by direct losses on bank mortgage lending and by indirect losses on banks’ other assets, caused by an economic downturn…

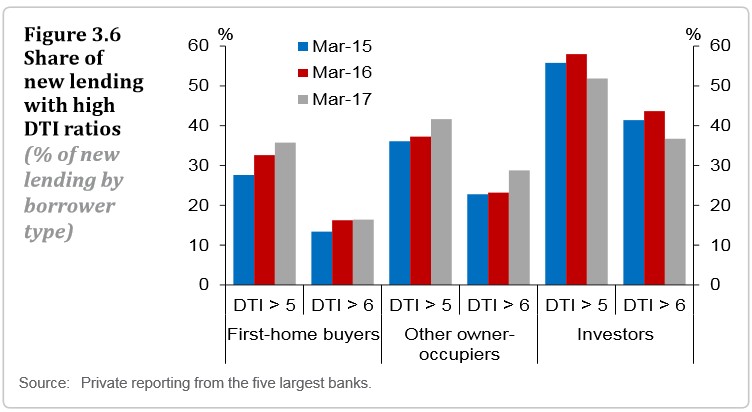

Banks report that the share of new lending at DTI ratios above five has continued to grow over the past year for first-home buyers and other owner-occupiers, to 36 percent and 42 percent respectively in March (figure 3.6). For investors, the tighter restrictions on high-LVR investor lending have had a significant impact on high-DTI borrowers, reducing their share of investor lending from 58 percent to 52 percent…

Preliminary Reserve Bank analysis on the impact of higher mortgage rates on recent borrowers suggests that many would struggle to service their mortgage if mortgage rates increased… Fixed interest rates may give some borrowers time to adjust to higher interest rates. However, based on banks’ current mortgage portfolios, about 40 percent of mortgages would re-price within six months and 60 percent within a year…

New Zealand is particularly vulnerable to a sharp rise in mortgage rates as the banking system funds a large proportion of its mortgage credit from offshore wholesale markets. The cost of this funding can increase sharply if there is an unexpected increase in global interest rates or a change in investor risk appetite, and banks are likely to pass on the higher funding costs to customers through higher mortgage rates…

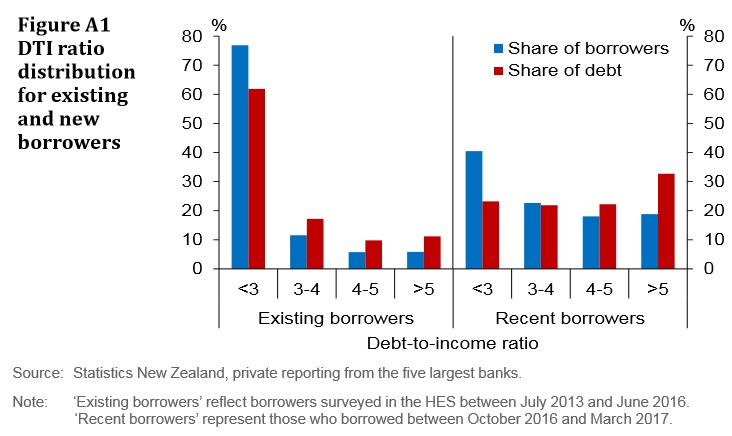

DTI ratios tend to be highest for recent borrowers who have had limited time to pay down debt or increase their incomes, and because house price inflation has been strong relative to income growth in recent years. After removing outliers, 19 percent of recent borrowers have DTI ratios above 5 compared to 6 percent in the overall stock of borrowers (figure A1). The share of new borrowers with high DTI ratios has increased in recent years (figure 3.6), which, if maintained, will increase the indebtedness of the overall stock of borrowers over time…

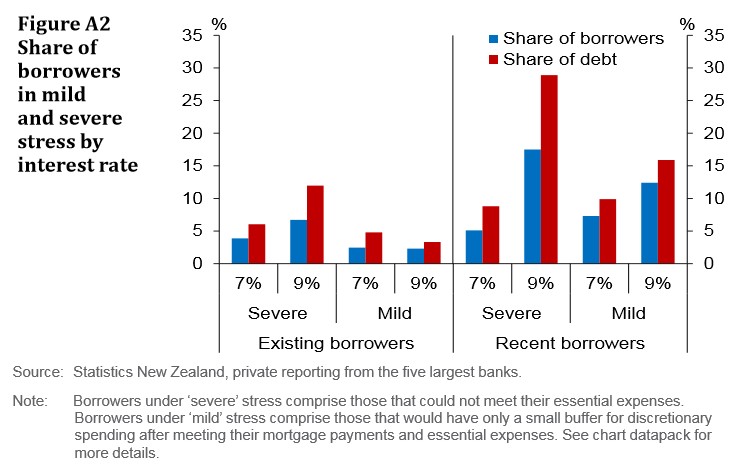

Many borrowers are estimated to be vulnerable to higher mortgage rates (figure A2). It is estimated that around 4 percent of all borrowers, representing 6 percent of the overall stock of mortgage debt, and 5 percent of recent borrowers, representing 9 percent of recent mortgage debt, could not meet their essential expenses (‘severe stress’) if mortgage rates were 7 percent. A further 2 percent of all borrowers and 7 percent of recent borrowers would only have a small buffer for discretionary spending after meeting their mortgage payments and essential expenses (‘mild stress’). Stress would be much higher at a 9 percent mortgage rate, with 7 percent of all borrowers and 18 percent of recent borrowers expected to face severe stress.

Auckland borrowers appear particularly vulnerable to higher mortgage rates. Around 5 percent of existing Auckland borrowers are estimated to face severe stress if mortgage rates were 7 percent, compared to 3 percent of borrowers outside of Auckland. The share of recent borrowers in severe stress is also expected to be greater in Auckland, particularly if mortgage rates rose to 9 percent.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.