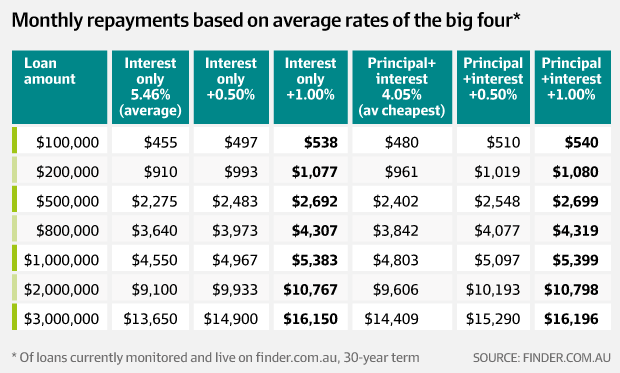

Any advantages of funding property portfolios with popular interest-only loans are rapidly disappearing as lenders hit the red alert button by raising rates, tighten terms and offer lucrative incentives to pay down debt.

Investors dumping property on to the market will trigger bigger falls, analysts warn. They are also being squeezed by recent federal budget restrictions on travel concessions for inspecting investment properties and cuts to depreciation claims for rental property furniture and fixtures.

Navid Guia has three investment houses, each with an attached granny flat — two in St Marys, 45km west of Sydney’s central business district, and one in Sacramento, in the US, close to his family.

All the properties are interest-only with a loan to value ratio of between 10 per cent and 20 per cent.

He is protecting his portfolio from rising rates and peaking prices by positive gearing, ie, income from the investments is higher than interest and other expenses.

…Other portfolio investors, such as Mario Borg, finance strategist, with Mario Borg Strategic Finance, says: “There are many home owners making interest-only home loan repayments, not realising that they could be paying a much lower interest rate if they choose to make principal and interest repayments.”

…Christopher Foster-Ramsay, of Foster Ramsay Finance, reckons the difference between investor interest-only loans and owner-occupier principal and interest rates will blow out to 100 basis points by the end of the year.

Nowhere in the article does it offer the best advice of all to property portfolio owners: sell up and deleverage because:

you’ve wrecked the economy by creating an enormous imbalance in household debt and regulatory authorities have turned against you;

Labor is going to win the next election in a landslide and remove negative gearing, forcing demand lower and supply higher, hurting prices;

anger is boiling about excessive immigration and the risk of cutting it back is obvious;

as we approach the end of the cycle shock, the three major supports to prices – interest rates, fiscal policy and immigration – are all approaching exhaustion.

Any property portfolio investor that knows his craft knows that he is, in fact, holding a highly-leveraged and illiquid set of assets that is very vulnerable and difficult to restructure if conditions turn against him.

That need not be an issue for the buy and hold investor. Real estate has cycles like everything else. But what that list of negatives adds up to for me is that this is not a normal inflation and policy driven business cycle.

Rather, it is a long cycle shift ahead – triggered by balance sheet not cash flow exhaustion – and that always involves a much deeper and longer shakeout.

Structural exhaustion requires structural repair and you do not want to get caught holding a portfolio of deflating assets with high leverage in that scenario.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.