“The core rationale is that the reflation dynamic is moving from the early deep cyclicals — notably commodities — to later stage cyclicals, particularly banks and technology,” say GS analysts led by Timothy Moe.

“Although we remain constructive on the banks, they have relatively modest 5 per cent upside to our target prices and less than for banks in other markets.”

“Our analysts have taken a more cautious view on the resource stocks given recent weakness in key commodities such as iron ore, coking coal, copper and aluminium.”

They see only 3 per cent upside to their materials sector price targets, with risk of earnings downgrades if commodity prices continue to decline.

“Therefore, the top-down thematic as well as bottom-up company analysis both point to a more restrained view for the bulk of the market capitalisation.”

After a 10 per cent boost to aggregate market earnings this year from a rebound in resource companies’ profits, they look for 6 per cent growth in 2018.

With a forward P/E multiple at 15.7 times — 1 standard deviation above the 10 year range — they we expect modest valuation compression and therefore expect only a 1 per cent price return.

“We also have a less enthusiastic view on Australian dollar prospects compared to six months ago when we were more positive on Australian equities and expect no FX tailwind.”

“So, even with the benefit of the region’s best dividend yield of 4.5 per cent, this results in 6 per cent total USD return, which is moderately lower than our composite 8 per cent regional expectation.

Next up, cutting back their absurd line-up of rate hikes. They’ve played a shocker on this rebound.

Morgan Stanley has been much better with its argument that global reflation is bypassing Australia:

Advertisement

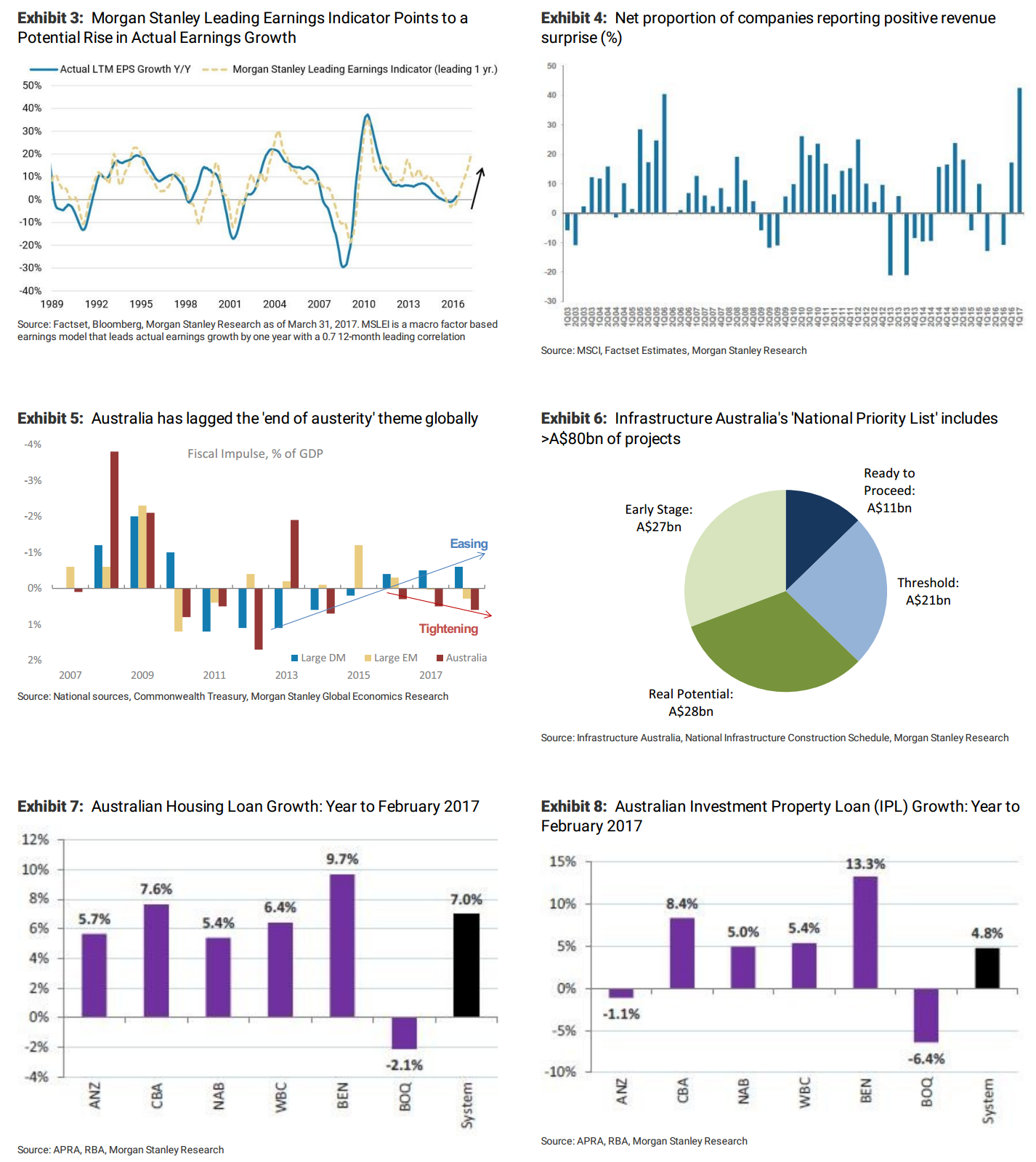

Revenue momentum and surprises are a key feature of recent US and European equity strength. In Australia, however, the asset turn for the industrial earnings cycle is falling, making the need for a fiscal boost more imperative.

Revenue Surprises Building in DM: One of the key planks in our US strategy team’s optimism towards the US equity market outlook is that revenue momentum for the S&P 500 is expected to build. Indeed, revenue growth has been increasing and is now expected to be close to 8% y/y in 1Q, the highest since 2012(US Equity Strategy: Initiation of Coverage: Classic Late Cycle, 10 Apr 2017). Likewise, European earnings have delivered a very strong set of results so far, with 43% of companies beating consensus estimates by 5% or more, with just 20% missing. The key feature has again been revenue trends where 58% of companies beat revenue estimates by 1% or more (versus 17% missing). The 41% net sales beat is the strongest on record with data going back to 2003.

Another Point of Disconnect for Australia: Unlike DM peers, the outlook for ASX 200 top-line growth is one of continued deceleration. After years of cost out and balance sheet focus, the headwinds building across the domestic cycle are limiting revenue growth potential.Low wage growth and higher ‘essentials’ costs all set the tone for a lower asset turn for the industrial cohort of stocks,and that places pressure on margins. Exhibit 1 and Exhibit 2show thatnot only are consensus sales estimate trends for Industrial-ex-Banks decelerating, but the reality of tougher conditions ahead has seen a significant drop off in FY17e growth rates and subdued aggregate levels expected for FY18e and FY19e.

Banks Commentary Confirms Lower Growth for the Economy: The current Banks reporting season has seen earnings supported by recent repricing initiatives but also a consequential impact of lower expected system and volume growth. Our Banks analysts recently cut total housing loan growth to sub-4.5% in FY18e and FY19e for the majors and we add this to business credit growth of 3-5% depending on which Bank you look at, system growth looks to be sub-5% for a while. The macro read-through is one of a looming disconnect and potential growth disappointment to consensus. Consumer Updates Mixed: With conference season underway and the raft of 3Q Industrial sector updates feeding through – we would assess the top-line momentum for many sectors as mixed to soft. The cracks seen in the recent WES update and recent CCL downgrade (Coca-Cola Amatil: The Earnings Cloud…23 Apr 2017) flagged good reasons for caution. And while WOW delivered a solid comp sales result – they took it off someone else rather than growing the category. More broadly there seems more pockets of weakness than strength with cautious commentary from A-REIT updates around specialty, slowing sales trends in SULauto and sports divisions,a still-cautious FLT and weak consumer impacts for SGR.

Fiscal Boost Needed: The slowing top line for the domestic economy is in need of a fiscal pulse to fund animal spirits. To date,actual spending in Australia has missed our forecasts over 2014-15 and exacerbated the post-mining boom weakness, despite a strong investment pipeline in NSW. The Federal Budget will be crucial to the macro outlook, with government rhetoric hinting at what we have called the ‘MissingFiscal Link’:an infrastructure stimulus. We have previously identified up to A$80bn (5% of GDP) of priority projects that could be fast-tracked through a stimulus over 5-10 years to also help absorb some of the labour displaced by the downturns in resources/housing construction. Skepticism remains high in consensus positioning, in our view, but this Budget will matter as either delivery of a necessary buffer to the slowdown happening or an accelerant (via disappointment) to a much lower growth outcome for the broader economy.

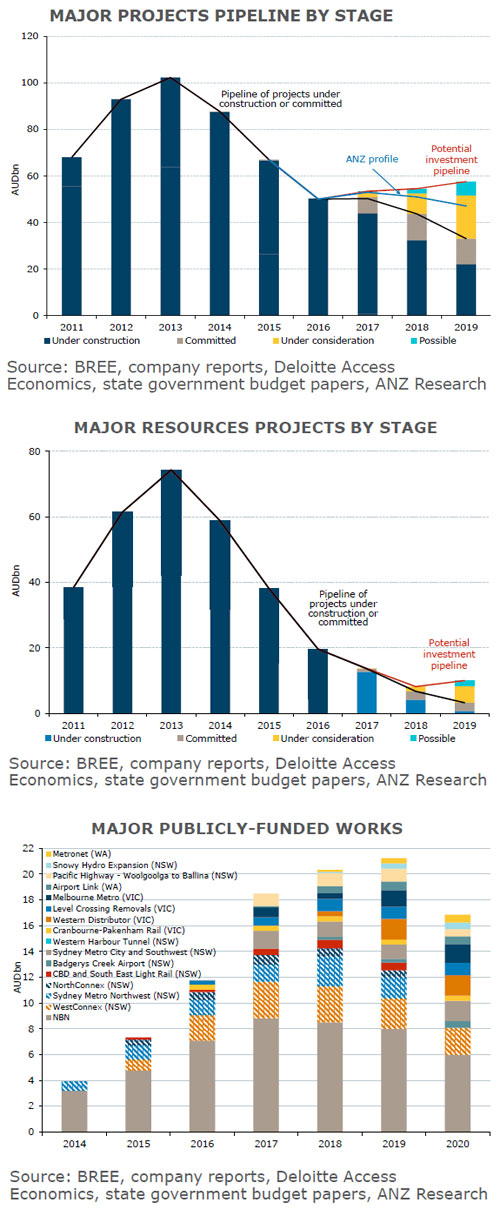

We got a little infrastructure stimulus of course but most of MS’ list is in addition to ScoMo’s chosen pork. Such as it is, the stimulus will barely add to growth beyond this year:

Advertisement

That’s a boost of 1-2bps to growth across 2018-2019.

With banks fading into partial-nationalisation and miners exposed to Chinese tightening plus a hideous iron market there will be nowhere to hide for Australian stocks over the next few years. It remains my view that the ASX is topped out.

If you would like to swim beyond the cracked and leaking local fish bowl with your investment, to jurisdictions where there is growth, then the MB Fund (launching in the next month with 70% international stocks) is for you.

Register your interest today (if you have not already):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.