Bottom line: USD has come under broad selling pressure(following inflation expectations) and is now trading below the level when US President Trump was elected. In the near term, the market should trade USD lower into next Wednesday’s expected testimony from Comey. The longer-term story is about growth expectations. EUR should stay supported, with currency-unhedged inflows into European equity markets leading the way. In contrast, JPY should weaken as the BoJ stays accommodative and global reflation comes back onto the agenda.

US political uncertainties seem to challenge this theme currently, explaining the sharp JPY appreciation witnessed this week. It may be too early to judge how much these uncertainties undermine economic prospects, but experience suggests staying cool headed. Politically motivated markets tend to be short-lived and, in the long term, economic fundamentals should prevail. EM is expected to trade weak in the near term as investors de-risk in highly positioned currencies like BRL. We still like currencies that benefit from the strong European outlook, like PLN.

Politics…Despite US political uncertainties, we expect the global reflation trade to stay in place. The economic environment under which political uncertainties surface makes a difference. Generally, combining a weak economy with weak political stewardship is never ideal and hence has the potential to undermine risk appetite. However, when an economy is cruising along and liquidity conditions are strong then politics should have less of an influence.

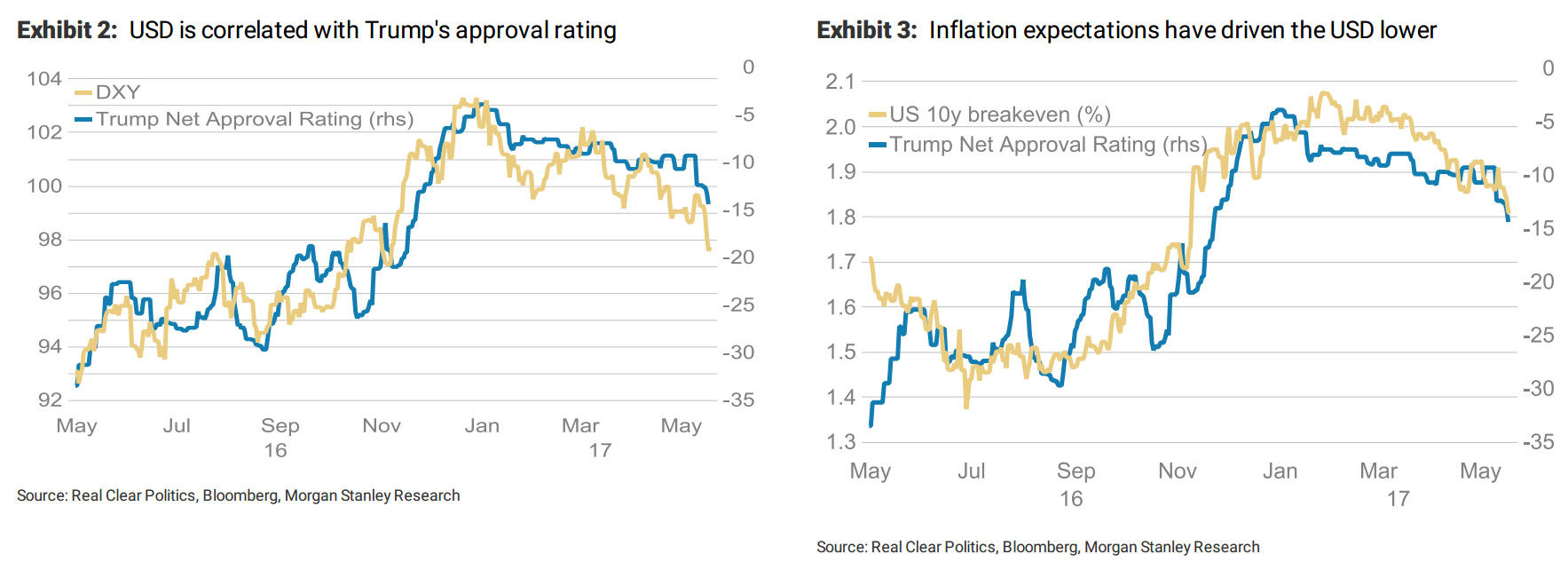

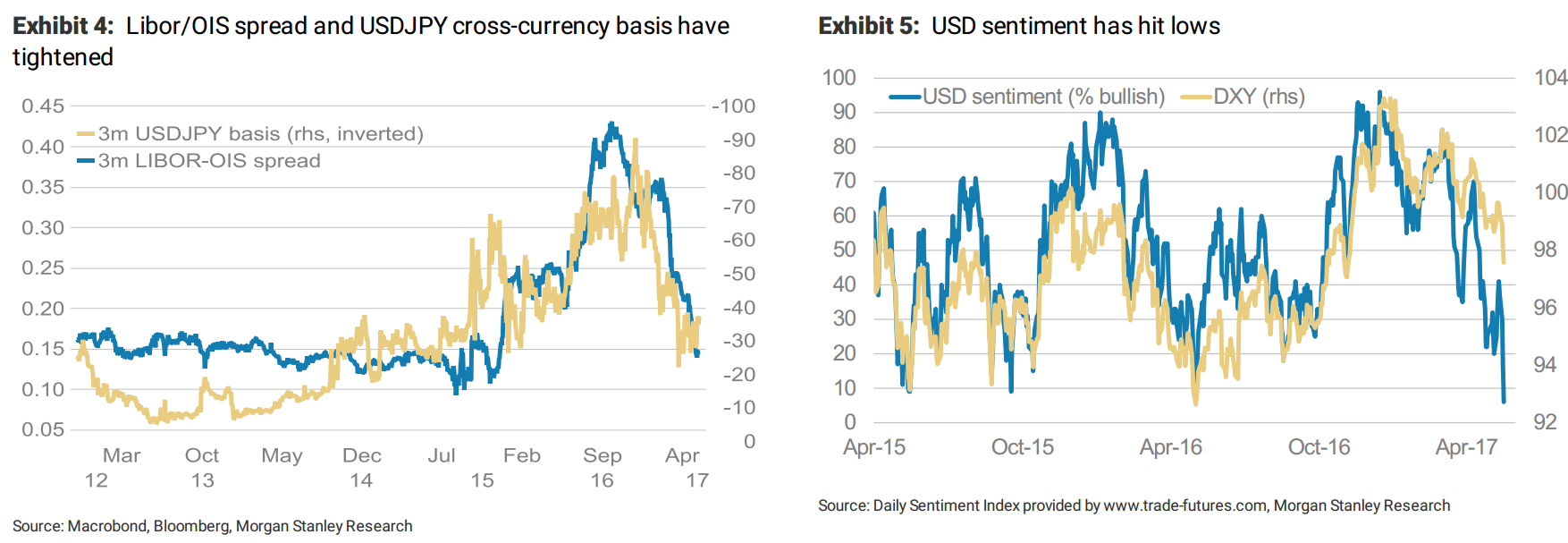

Nonetheless, recent swings in USD find some explanation in changes in President Trump’s domestic support. When his popularity was on the rise, USD moved higher. Conversely, when his approval rating declined, it took USD with it (Exhibit 2). Markets seem to assume that a declining support rate may reduce the US reform momentum and with that the US growth outlook. Dollar sentimen thas also hit lows (Exhibit 5).

….rarely dominates markets for long: There have been two previous occasions of political instability in the US to which many commentators refer . When the Watergate scandal broke during President Nixon’s term, the US economy suffered significantly, but then political uncertainty was only exacerbating weak trends which had been established by other factors such as the oil price shock and the break of the Bretton Woods post-WWII currency framework. When US President Clinton was under pressure due to the Monica Lewinsky affair, the headlines were on the president, but it was Asia’s 1997 balance sheet adjustment dominating markets, pushing USD higher. The message is clear: it is the underlying economic conditions driving markets even though politics may dominate headlines.

The US economy is in good shape, and we base this assessment not only on macro data. At least equally important has been corporate earnings beating market expectations in the current reporting season. Importantly, this beat has not been achieved by financial engineering such as depreciating the existing capital stock at a faster pace than reinvesting to generate positive cash flow. Instead, it has been the bottom line driving corporate earnings higher,underlining the strength of the current economic cycle.

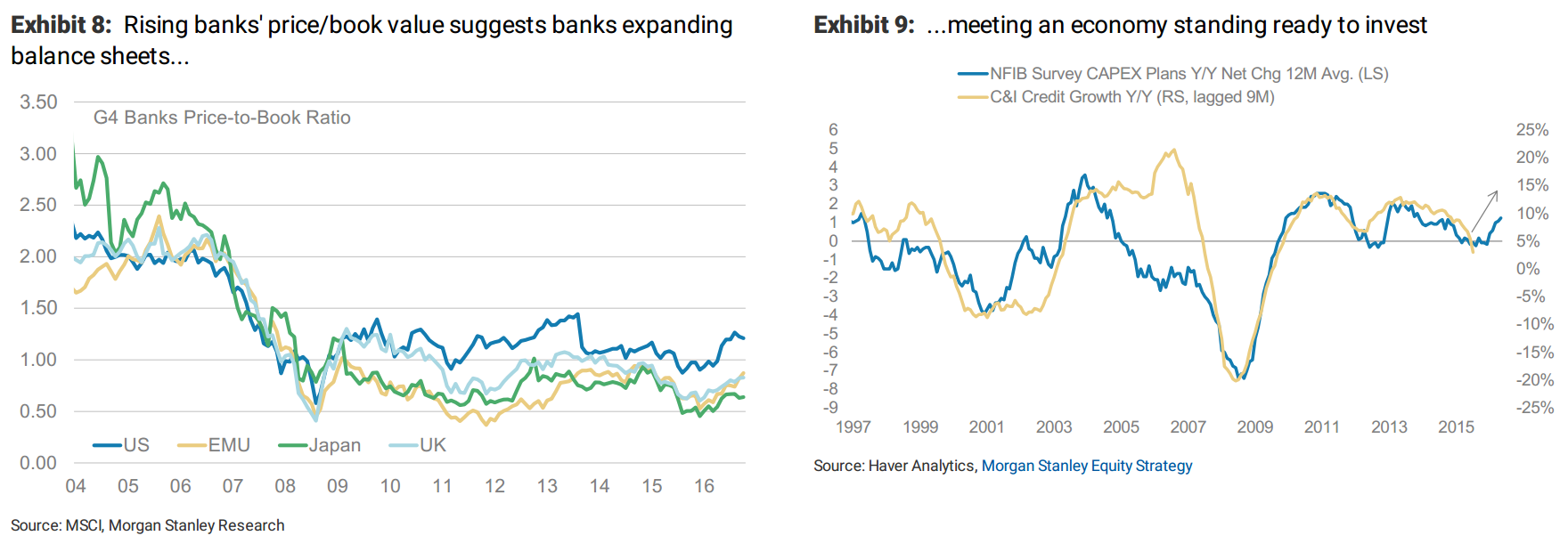

Exhibit 8 shows bank shares’ price/book value. When share prices move towards book value, balance sheet management tends to kick in. In this case, caution tends to prevail, driving balance sheet consolidation. This process sees money supply growth falling, reducing the pace at which central bank liquidity is converted into high-powered liquidity. US bank stocks have taken the lead, pushing well above their book value, suggesting that it may be US banks leading the process to push up the money multiplier. If so, USD liquidity conditions should remain supportive.

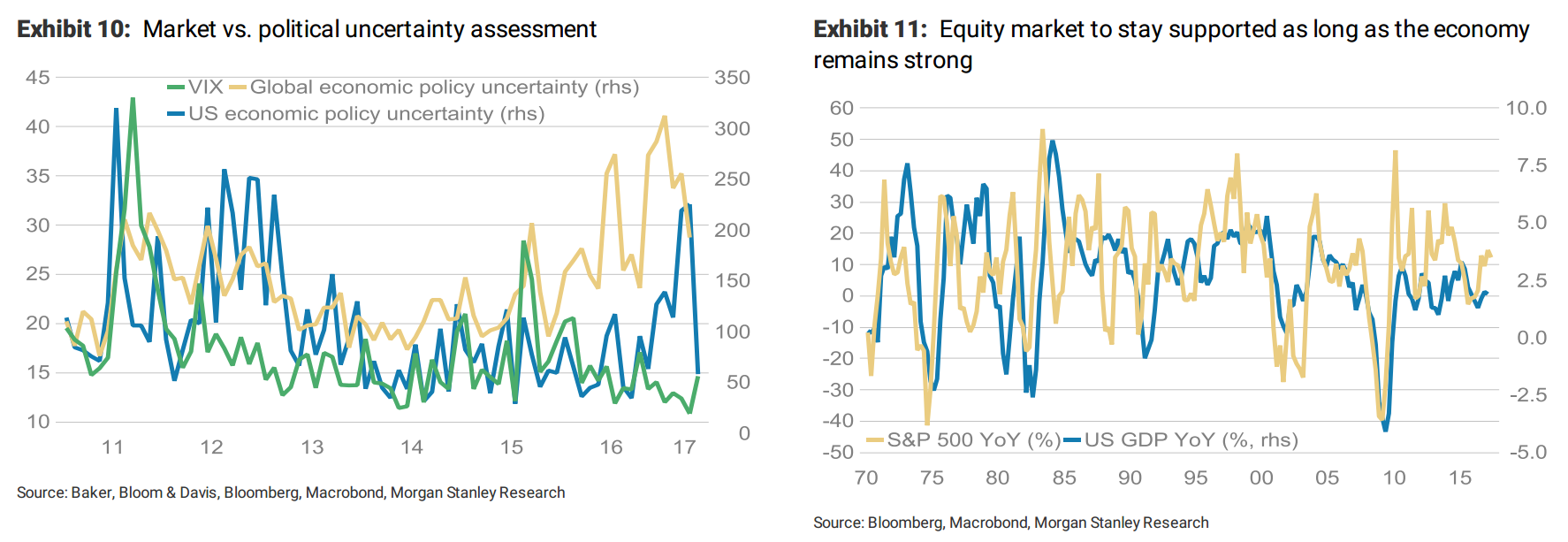

Looking at the vol markets: After a period of calm and low volatility, US political uncertainty drove the VIX sharply higher over two days. The longer-term outlook isn’t to see the VIX back athistorically high levels because global market liquidity is expected to remain ample. Exhibit 10 shows the relationship between market uncertainty (VIX) and political uncertainty. Not so long ago, there had been a gap between market and political uncertainty, illustrated by a low VIX and high policy uncertainty.

With US political turbulence, this gap has narrowed, with the VIX catching up. When it comes to the interpretation of the market pricing of volatility, we like to differentiate between events driving volatility higher and longer-term, structural, liquidity-motivated forces influencing volatility. These structural forces suggest volatility coming back down again. Globally,an excess of DM liquidity defined by money supply growth exceeding the nominal expansion rate of GDP has remained high, suggesting the VIX is likely to decline again soon.

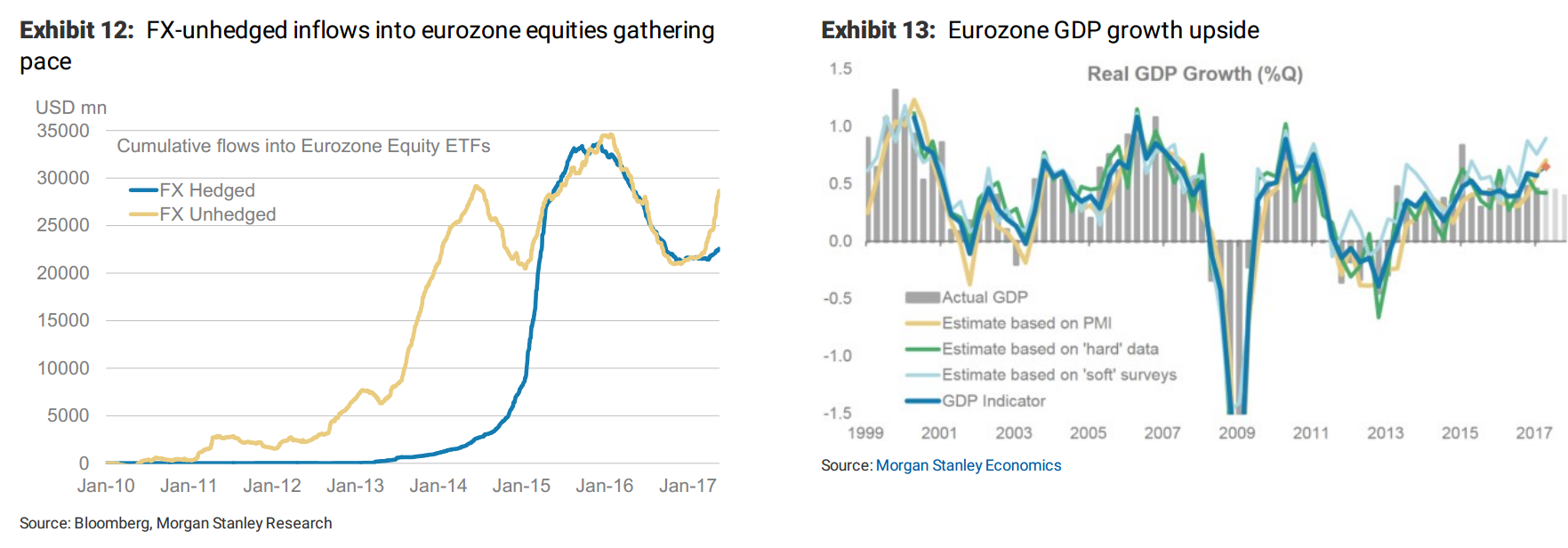

The better EUR outlook: EUR has gained across the board, with currency-unhedged equity inflows leading the way. EUR-denominated risk assets look comparatively cheap and, with markets enjoying supportive liquidity conditions, investors will likely look for value. It is not only EUR benefiting from value-driven flows. Yield pick-up themes have entered the market with investors reducing their low-yielding/liquid exposures, moving funds into higher-yielding assets even if this locks funds in assets offering weak liquidity conditions. Investors turning securities exposures into investing directly into loans or switching liquid currency holdings into exotic, less liquid currencies such as the Icelandic krona provide examples for this switch.

More than late-cycle strength? Positioning for EUR appreciation is a late-cycle trade. Remember that from late 2007 to 2Q08, EURUSD gained from around 1.40 to 1.60 on the perception of a stronger EMU economy at a time when US balance sheet concerns first emerged. Yet again, EUR seems to be heading towards a late-cycle advance, with the better global economy not only helping EMU economic performance, but also increasing demand for EUR-denominated assets trading at attractive valuation levels. So far, EUR strength has been best expressed via EUR crosses against any G10 currency other than USD and GBP. Here, we expect more EUR gains, supported by speculation about the ECB moving towards tapering and higher interest rates, EMU’s export industry monetizing better global demand conditions and past EUR weakness,and markets being hopeful about President Macron’s reform plans and the impact they could have on EMU’s regulatory framework.

The political angle: When President Hollande came into power five years ago,his plans concerning EMU’s regulatory framework were ambitious too. However, Hollande did not link his EMU reform proposals with a domestic reform agenda. Germany had little appetite to change its tough stance due to Hollande’s poor domestic reform agenda. Macron offers a different approach, linking his domestic agenda with EMU reform.

Germany will have its own General Election on September 24. Chancellor Merkel’s junior centre-left coalition partner (SPD)has lost three local elections in a row, increasing Merkel’s chance of getting a fourth term mandate. Markets wonder whether populism has increased EMU reform needs. Macron’s opponent Le Pen has doubled her votes over the past five years;another five years of reform standstill could increase populism further not only in France, but also in other European countries. EMU reforms may now need to be delivered to avoid populism becoming an even bigger problem in the eurozone.

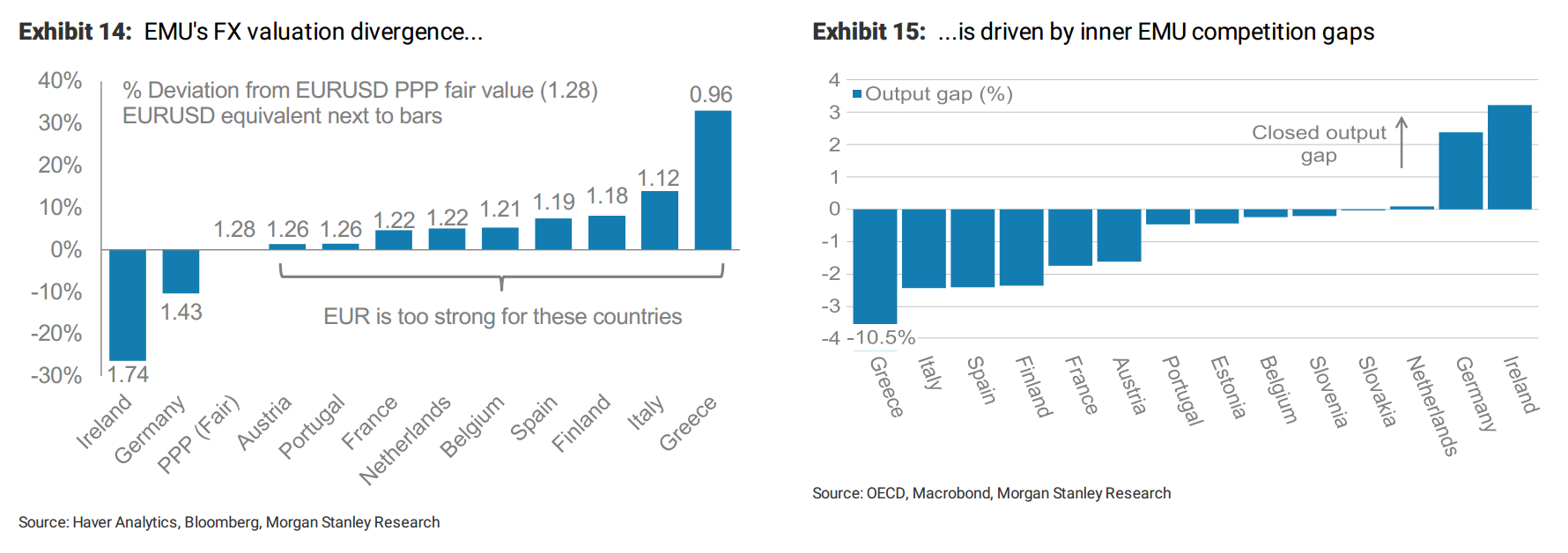

Turning away from the Italian EUR: Our valuation models suggest EUR undervaluation, but only if applied from a common eurozone perspective.From the perspective of individual EMU member states, EUR may not be undervalued (Exhibit 14).For instance, EUR trades near levels compatible to Italian fundamentals, leaving the impression that EMU monetary policy has been set to keep the Italian economy sufficiently supported. Should EMU move closer towards a comprehensive banking/ fiscal union, EUR should move up to valuation levels appropriate for the entire eurozone. Following the German election in September,all eyes will be on whether the new German government may consider a faster pace of EMU integration.

EM Positioning important. US political developments are moving fast and have shaken markets out of their complacency.Further position adjustment can lead to some nearterm EM weakness,and we stick to a neutral view overall on the currency asset class. However, from a longer-term perspective we do not see US political events as something that would derail the investment case for EM. Concerns regarding the ability of the US administration to push through legislation to help US growth would ultimately lead to a weaker USD.

With growth in the EM world picking up and the eurozone outlook looking heathier, the global growth differential would move in favour of the rest of the world, aiding USD weakness. Should US equities take a further stumble, then this would very likely pressure EM further in the near term, but our US equity strategists see upside in the S&P 500 over the rest of the year as a result of strong earnings momentum, which crucially is not dependent on US tax or broader fiscal reform. As such, the unwinding of the ‘Trump reflation trade’ should only place temporary pressure on markets.

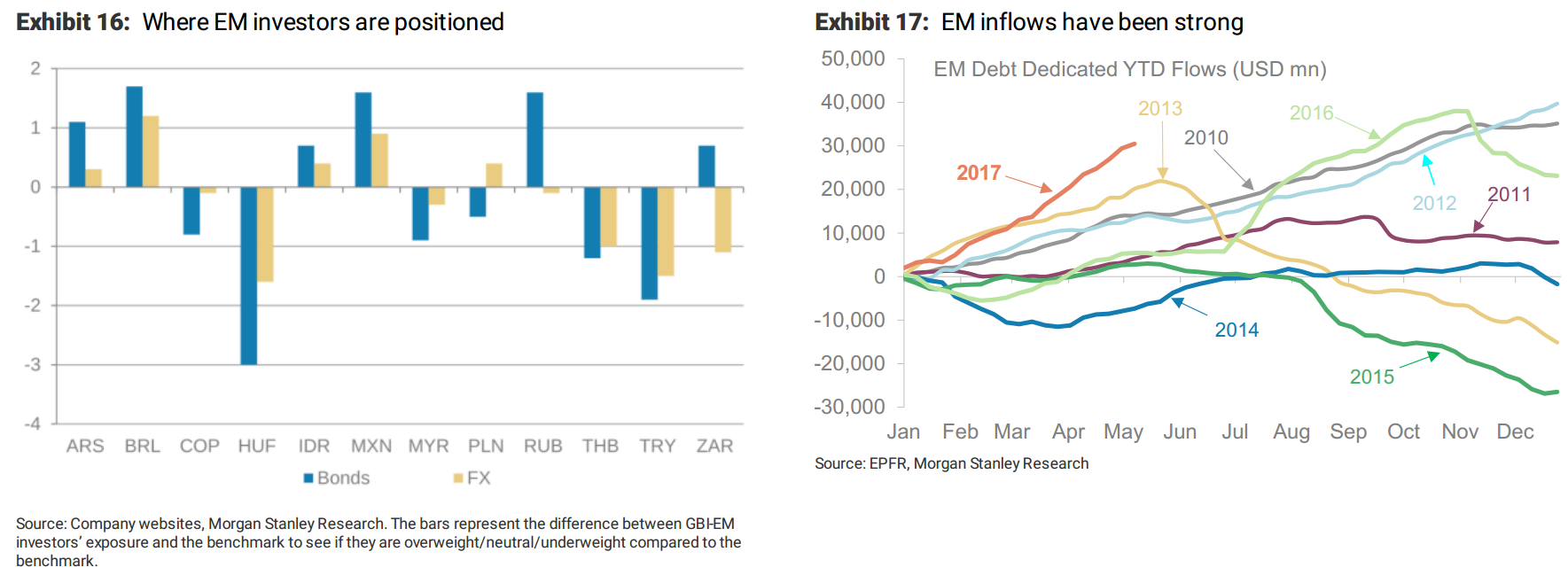

Where is positioning heavy? Temporary EM pressure is likely to be focused on those markets where positioning is heaviest. Our data suggest that fixed income investors remain overweight Brazil,and given political developments in the past 24 hours position reduction will be driven by both local and offshore sentiment. The extent of overweight positioning in both FX and local bonds has reduced in Brazil over the past few months, but remains one of the larger overweights within the EM investment universe, alongside MXN and RUB.

In Brazil, with just two weeks to go until the crucial pension-reform vote, the suggestion by local news that the country’s president is involved in an alleged cover-up and bribery scandal would, if confirmed, raise serious questions about the administration’s ability to govern. With much of the asset price recovery in Brazil based on the growth-enhancing effects of fiscal reform,a sizeable market reaction could ensue if reform momentum is permanently halted and expectations for growth heading into the 2018 election year are marked lower. We were stopped on our BRL position and stay on the sidelines at this point. Even if the headlines are not corroborated, this has illustrated the fragility of Brazilian politics,and could drive investors to look for other EM opportunities.

The USD sell-off has had limited impact on the AUD because of its reduced sensitivity to US yields. The labour market report was strong on the headline (unemployment rate falling) but saw the pickup in part-time jobs instead of full-time, which fell. Australia’s wage data is still expected to be muted, limiting the upside for inflation. Iron ore prices have stabilised now so the focus has turned to the overvalued housing market and consumer confidence. With volatility expected to remain for the USD, we keep a tight stop. CFTC data suggests the market is still long the AUD, which we think is in the process of changing. The banking sector is now under strain after the introduction of a bank levy, which could risk profits and limit wages. Target: 0.69.

Good stuff that. The pilot MB Fund rode the US reflation from December to mid-March then took profits three times, rotating to Europe from mid-March in anticipation of the market move. Both trades have been highly profitable in equity and forex terms. At this stage the pilot fund is still invested in the US though is underweight while it is long selected European stocks. We remain cautious around EM given China is so large a part of that universe and is clearly slowing.

If you’re interested in investing beyond Australia’s sclerotic shores then the MB Fund is for you. It launches in under a month so register your interest today (if you have not already):

Register your interest today (if you have not already):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.