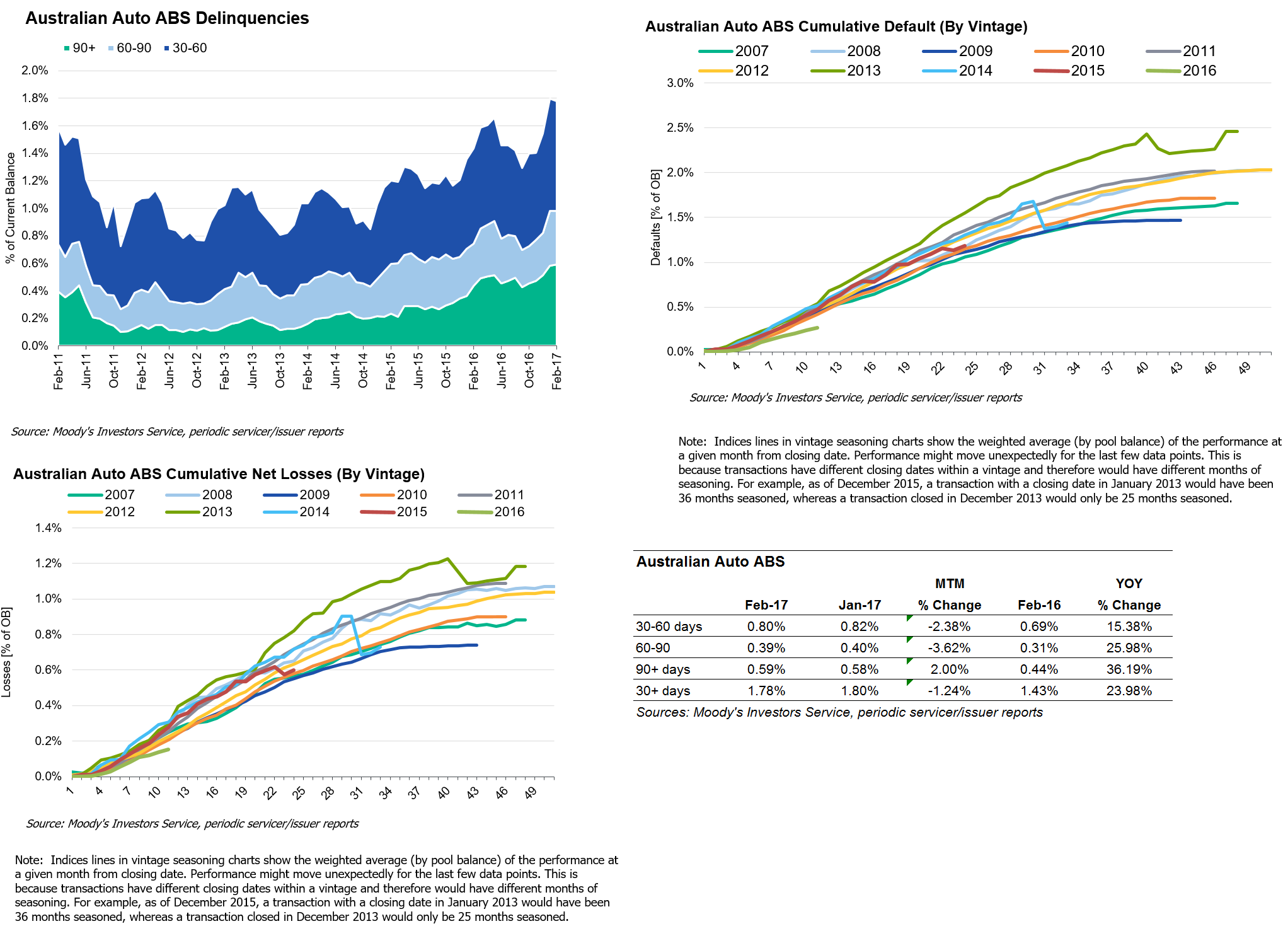

Moody’s Investors Service says that delinquencies for Australian auto loan asset-backed securities (ABS) fell in February 2017 from January 2017, while prime residential mortgage-backed securities (RMBS) rose.

Specifically, 30+ day delinquencies for Australian auto loan ABS transactions decreased to 1.78% in February 2017 from 1.80% in January 2017, but was up from 1.43% in February 2016.

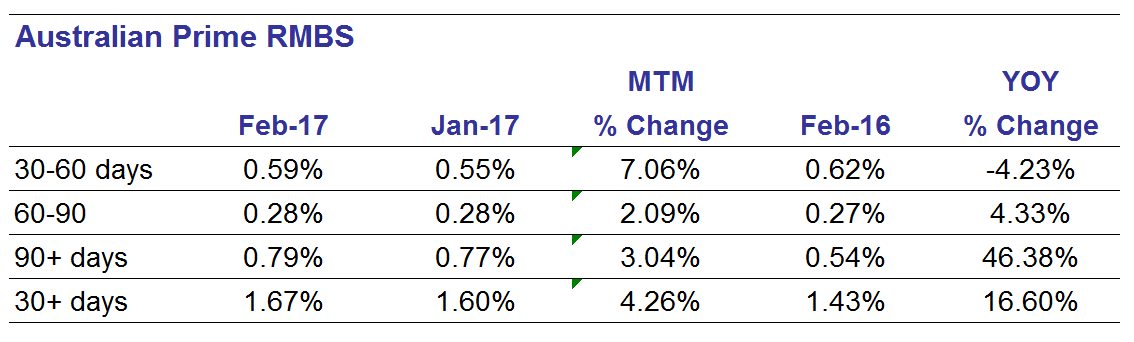

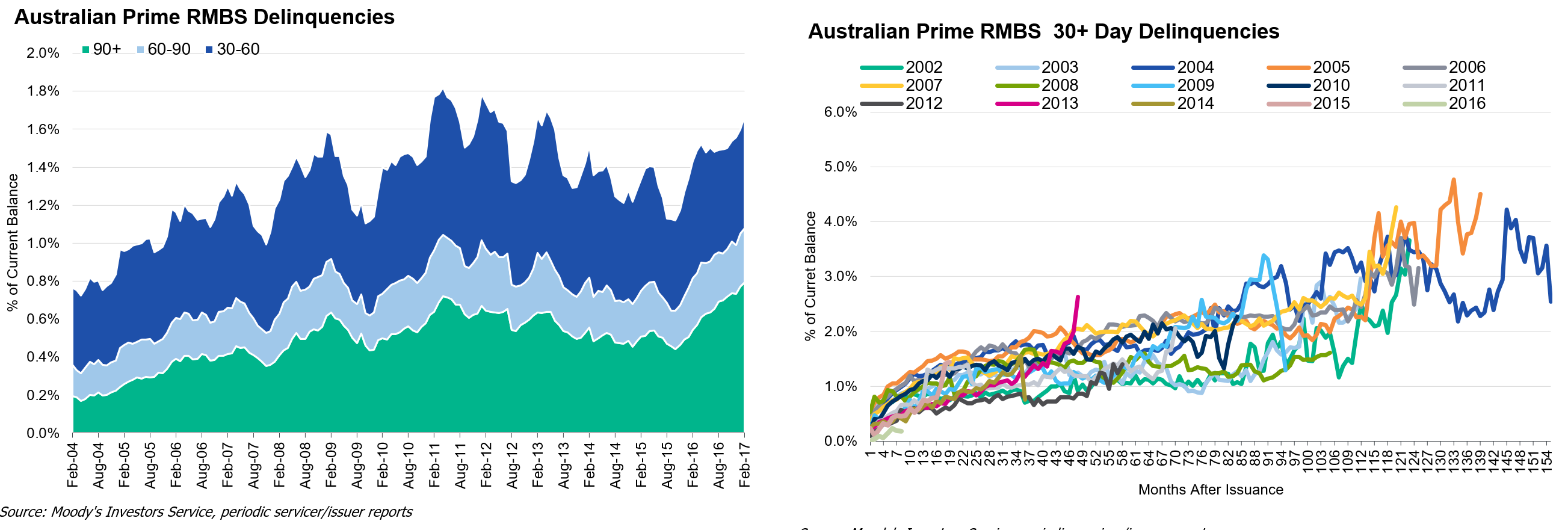

Delinquencies for prime RMBS transactions rose to 1.67% in February 2017 from 1.60% in January 2017 and 1.43% in February 2016.

“Looking ahead, we expect that delinquencies for Australian auto loan ABS and prime RMBS will continue to rise in 2017,” says Alena Chen, a Moody’s Vice President and Senior Analyst.

“Weaker economic conditions in states reliant on the mining industry, rising underemployment, weak wage growth and less favorable housing market conditions will drive delinquencies higher,” adds Chen.

Chen was speaking on the release of the latest edition of Moody’s monthly Global Structured Finance Collateral Performance Review report.

Moody’s semi-annual study of RMBS delinquency rates in Australia — which compares the performance of residential mortgage loans on a state, region, and postcode level — shows that delinquency rates have increased across all states.

A significant portion of the increase in delinquencies can be attributed to the inclusion of loans under hardship arrangements in the calculation of delinquency rates, but delinquencies increased irrespective of this development.

In Western Australia, South Australia and the Northern Territory, the 30+ delinquency rate climbed to the highest levels since Moody’s records began in 2005. Mortgage performance in New South Wales was relatively strong, despite an increase in delinquencies.

Weaker conditions in states reliant on the mining industry, high underemployment, and less favourable housing and income dynamics will drive delinquencies higher.

…New regulatory measures to restrict interest-only mortgage lending will have some impact on demand for housing, particularly apartments. Nevertheless, overall, Moody’s expects the upward pressure on housing prices to continue in the near term, in an environment of low interest rates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.