by Chris Becker

All pistons firing with all markets opens today and reacting to full markets open last night with the Chinese manufacturing PMI released without much fanfare around lunchtime. While it was a good print, most markets were unphased with a mix of scratches and small retreats for stocks while commodities retreated particularly iron ore, which weighed on the big miners on the ASX200.

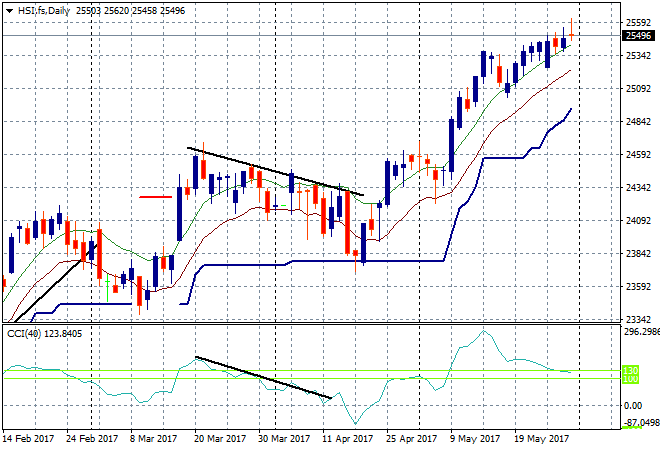

In mainland China the Shanghai Composite reopened after a long weekend and is currently up a little going into the close, holding on at 3118 points, just above key support at the 3100 point level. The Hong Kong based Hang Seng Index had a scratch session, just above 25500 points as momentum tapers in the current reflation trade:

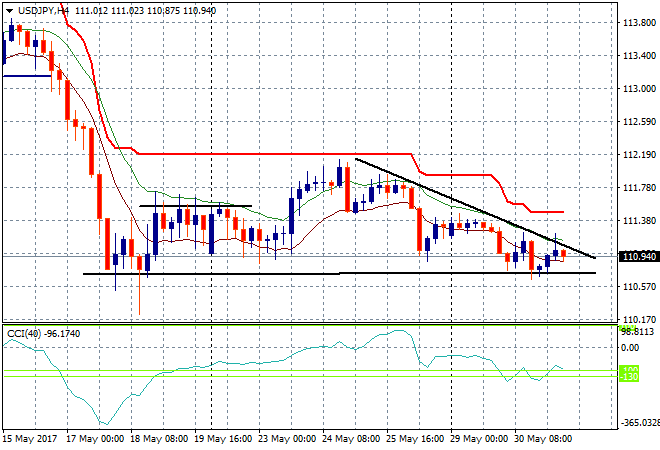

Japanese stocks retreated as Yen strengthened slightly against USD with the Nikkei finishing down 27 points or 0.14% lower to 19650, still well below key resistance at 20,000 points. The USDJPY pair remains depressed here, dicing with the 110 handle in what looks like a setup to breakdown going into Friday’s NFP:

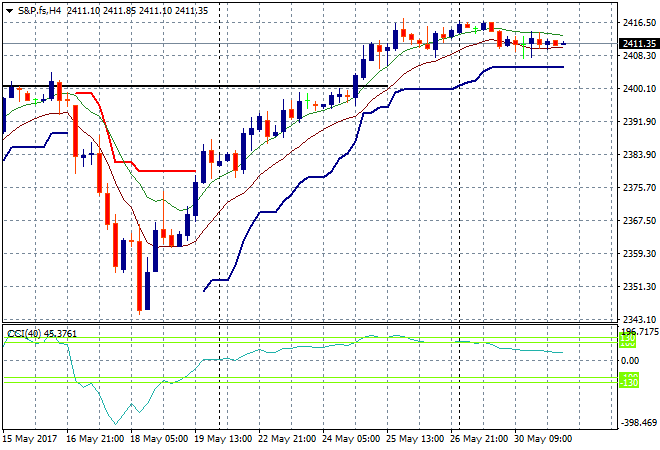

S&P futures are again off slightly after last nights fairly weak showing on the broader market:

The ASX200 started off well enough and ramped up going into the PMI print but sold off going into the close, barely finishing with a scratch session at 5724 points, still well below local resistance at 5800 points.

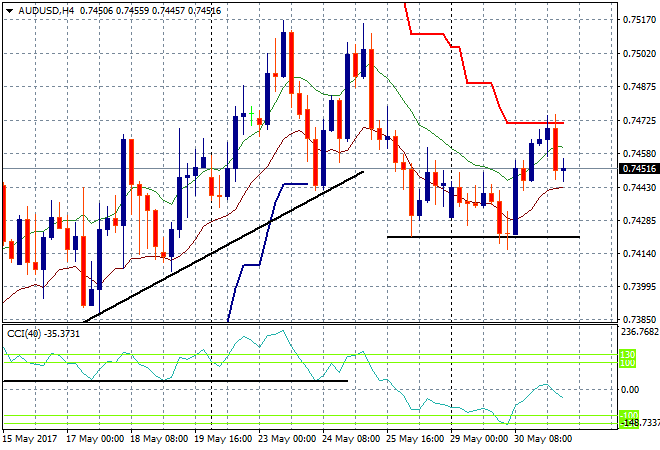

The Aussie dollar had a false breakout that caught traders (thanks…sheesh) on the PMI print, before reversing and heading back down to 74.50, proving that four hourly ATR resistance overhead is too strong:

The data calendar tonight includes the most important figure for the ECB – German unemployment – and expands on last nights German CPI with the EZ wide version. In the US its a preview of the FOMC’s wider view with the Biege Book release.