by Chris Becker

Yet another low volume day in Asia as Chinese markets remain closed while other bourses tried to find their way after the UK and US markets were also closed overnight. Currency markets are acting on Super Mario’s dovish comments last night, selling the Euro down, but other safe havens like Yen and gold remain strong. All eyes will be on a slew of US economic data, plus the Twitter-in-Chief back on home soil after a weekend of golf.

In mainland China the Shanghai Composite was closed while the Hong Kong based Hang Seng Index also took the day off.

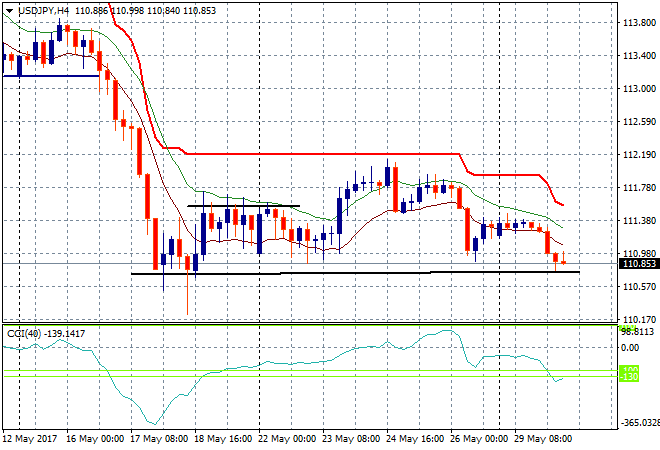

Japanese stocks were again little unchanged, even as Yen strengthened slightly against USD on low volumes. The Nikkei finished another four points lower at 19677, still well below key resistance at 20,000 points. The USDJPY pair fell on the Tokyo open, heading below the 111 handle but finding some support from a previous week low here. But turn this four hourly chart upside and it looks like a breakout pending no?

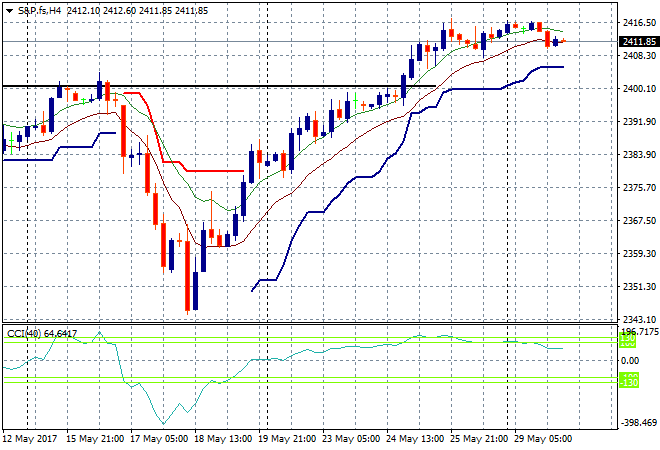

S&P futures are off slightly in anticipation of markets reopening tonight:

The ASX200 at first sold off on the open in what looked like a repeat of yesterdays sour start to the week but eventually rallied after the lunch break to finish up 0.2% to 5717 points, still well below local resistance at 5800 points. Nothing to get excited about as it was probably short covering going into tonights session.

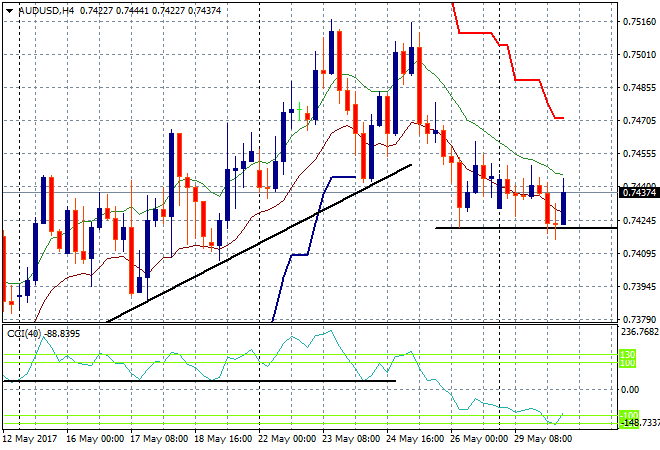

The Aussie dollar followed in kind, heading back to last week’s intrasession low at just above the 74 handle against USD before rallying this afternoon. It will be a turgid week for the Aussie as we await the Chinese manufacturing PMI on Wednesday then the non-farm payrolls on Friday night. The 74 handle must hold here:

The data calendar tonight includes the most important economic print for Euro traders – German CPI – while there’s two big hitters from the US, namely personal consumption expenditure and consumer confidence data for April, with house price data in between.