by Chris Becker

Asian markets have absorbed the Moody’s rating cut to China’s debt levels with aplomb with initial downside reaction mainly filled across share markets, with most volatility on commodities as iron ore crashes alongside copper and a weakening gold price.

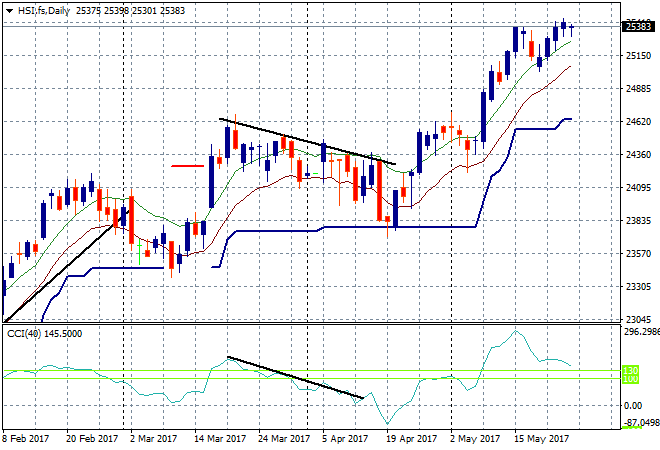

In China the Shanghai Composite recovered from the rating cut after being down nearly half a percent to put in a scratch session, rising a few points to finish at 3064 points, still unable to climb back above its once critical support level at 3100. In Hong Kong the Hang Seng Index has done the same, barely moving yet remaining at its near high just over 25000 points:

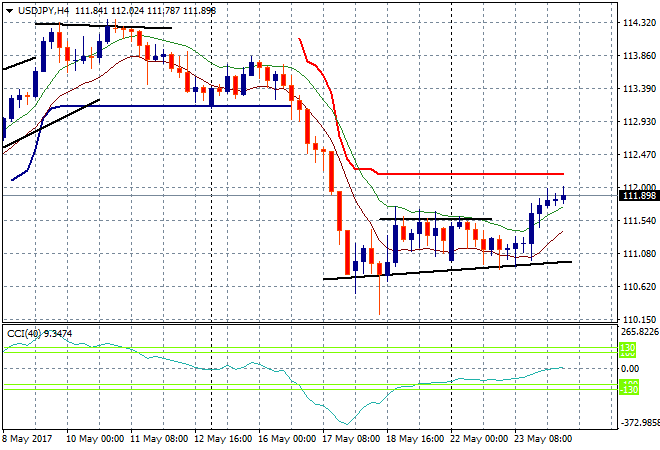

Japanese stocks moved higher as expected on the weakness in Yen, with the Nikkei closing up 0.66% as it bares down once again at resistance at 20,000 points. The USDJPY pair continued its slight uptick, dicing with the 112 handle but still not out of the woods yet:

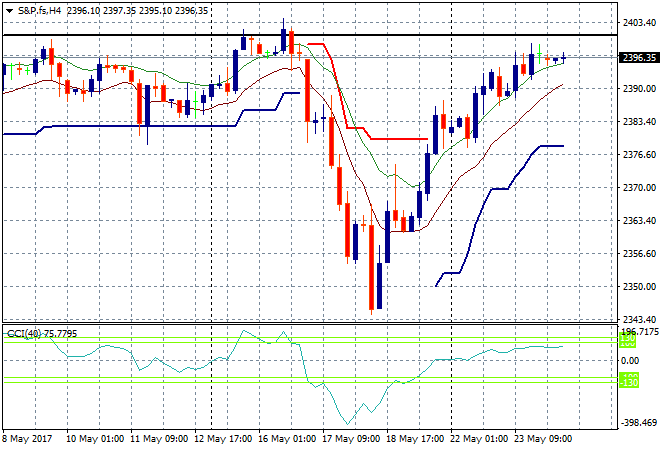

S&P futures are moderating/decelerating the recovery with the S&P nicely back to its pre-dip level where the 2400 point area will be heady resistance:

The ASX200 had a weak session, again having a solid opening and pre-lunch session before selling off in the afternoon to finish only 0.2% higher to 5769 points. While Fortescue dropped nearly 5% as iron ore prices dumped in Dalian trading, the other mining majors were relatively unsettled with Newcrest the only other big loser down 3% as the gold price moderated overnight.

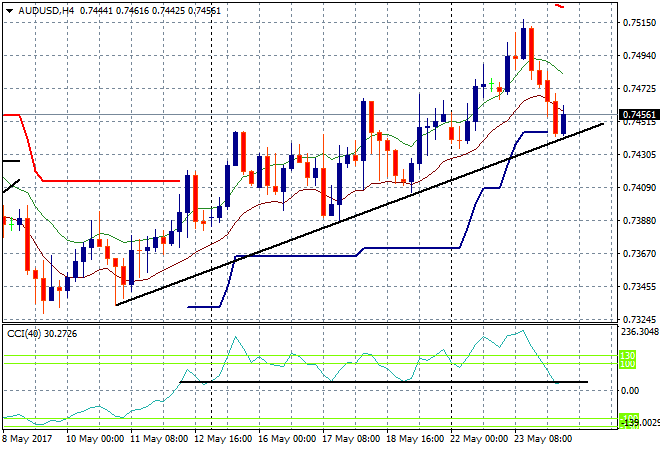

There was action in Aussie dollar though, heading straight down to its bear market rally trendline on the Moody’s cut to 74.50 or so. This tentatively takes out ATR support and the low moving average but I’m waiting for the City t open for confirmation of a final breakdown here:

The data calendar tonight includes a speech by ECB President Mario Draghi, and several key US releases including existing home sales and DOE oil inventories before the release of the last FOMC meeting minutes.