by Chris Becker

Asia starts the week in a mixed mood with a disappointing Chinese industrial production print overshadowed by rising oil prices as OPEC mulls a longer staged cut in supply. Following the equally mixed Friday night lead, stocks across the region have put in scratch sessions in the main, with the USD weakening against the major currencies and gold.

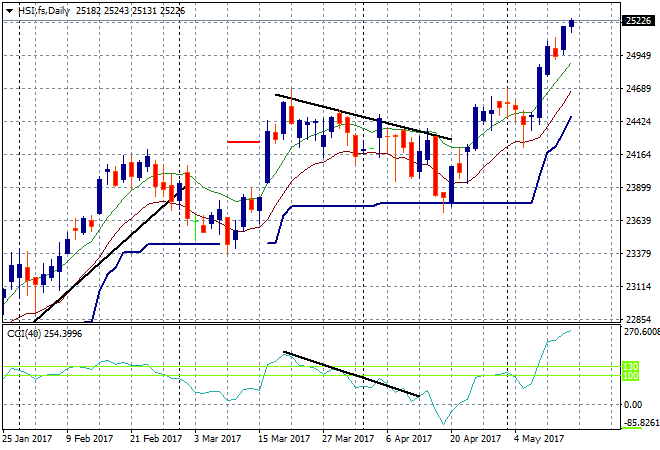

In China the Shanghai Composite is up only 6 points going into the close, or approx. 0.2% higher to 3089 points. The critical support level at 3100 remains too far away once again. In Hong Kong the Hang Seng Index is doing a lot better, making another daily high up 0.6%, remaining well above 25000 points. Momentum readings are nearly off the chart here so a retracement should be expected soon:

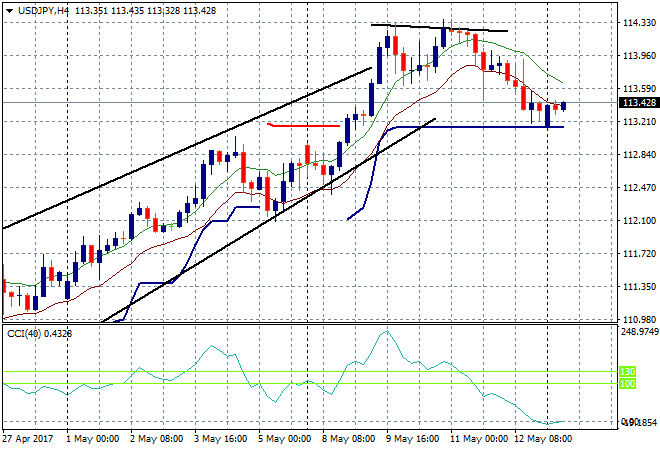

Japanese stocks slipped ever so slightly as the Yen remained somewhat steady against USD during the Monday morning gap and first session. The Nikkei finished 0.1% lower, unable to stay above the elusive 20,000 point level. The USDJPY pair remains where it ended last week at just above the support level at the 113.20 area, where positioning for a breakdown here makes sense:

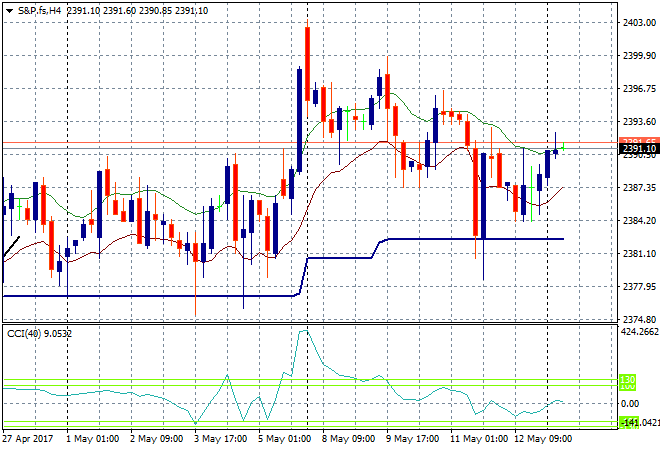

S&P futures are dropping slightly as fears of a spent consumer going into the Northern hemisphere summer continue to rise:

The ASX200 started the week with a scratch session to be at 5838 points, with rises in bank stocks offset by losses in most mining stocks. The reaction to the Chinese industrial production print has been muted to say the least with the only opportunities on the ground available to the intraday traders.

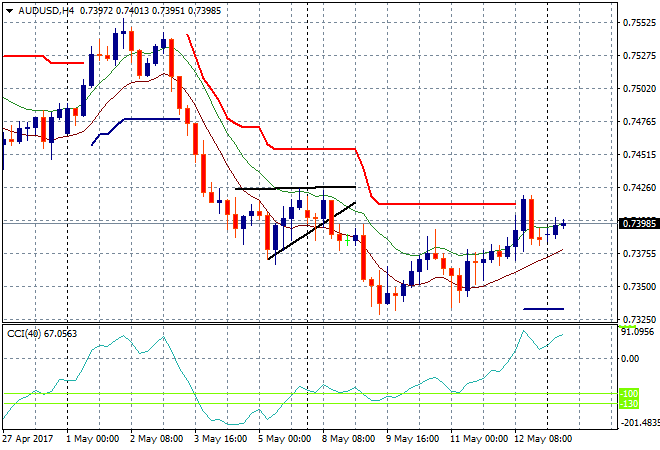

The Aussie dollar is still trying to come back, slowly lifting up to but not above the 74 handle against USD through today’s session. Short term price patterns plus the lower momentum reading suggest this could follow through but the bears remain in charge in the medium term:

The data calendar starts the week slowly with some mid level US housing figures stats only on the watch tonight.