by Chris Becker

Asia ends the week with a whimper as stocks across the region outside China fall on a lack of risk taking in response to overnight moves in US markets. Tonight’s advanced retail sales data will either embiggen the risk takers or have them scurrying as the Chimerica make cheap consumer crap/buy cheap consumer crap dynamic holds into the second half of the year. Commodity prices are mixed with oil and gold up slightly but iron ore down once again putting in nearly two months of decline.

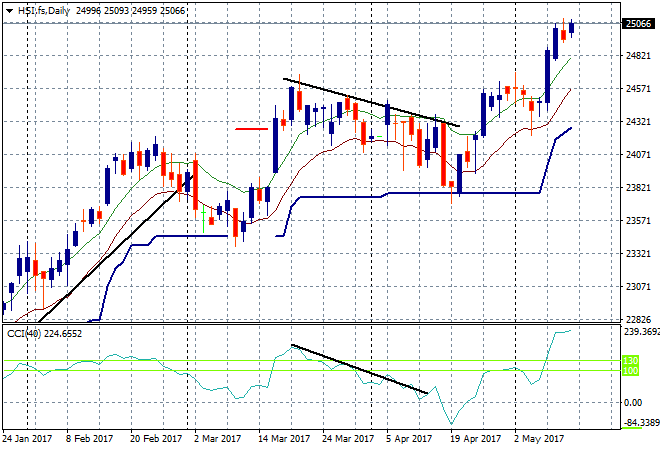

In China the Shanghai Composite is leading higher going into the close, currently up nearly 0.8% to 3087 points. The once critical support level at 3100 is only a few points away, but its now turning into strong resistance as the bear market rally evaporates in the face of tightening regulation. Not so on the Hong Kong based Hang Seng, currently up 0.2% making another daily high and crushing my expectations for a retracement as it remains above 25000 points:

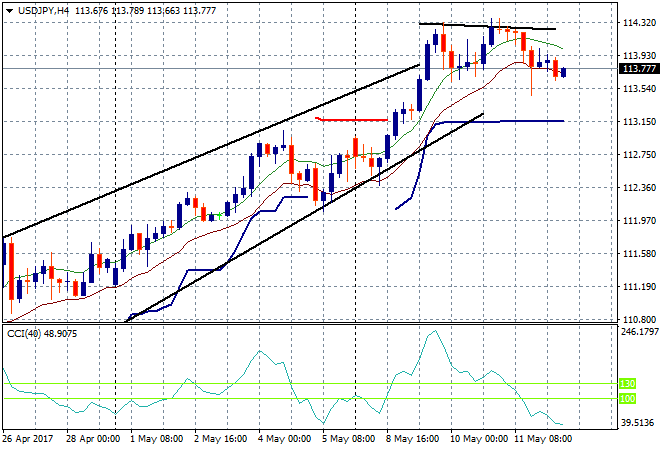

Japanese stocks slipped though as the Yen regained some modest strength. The Nikkei finished 0.4% lower, unable to stay above the elusive 20,000 point level. The Yen is slowly moving higher against the USD with the USDJPY pair slipping just below the 114 handle and unable to make further headway. The next support level here is around the 113.15 level and could be tested tonight:

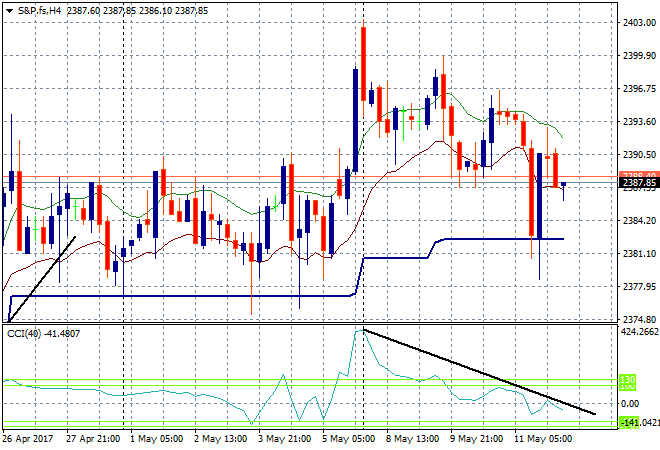

S&P futures are dropping slightly as fears of a spent consumer going into the Northern hemisphere summer continue to rise:

The ASX200 finished the week in a slump, falling over 0.7% to be at 5836 points, as consumer and bank stocks suffered the brunt of losses. This takes the bourse below my watch level of 5850 points setting up a possible correction here after tonights economic data print.

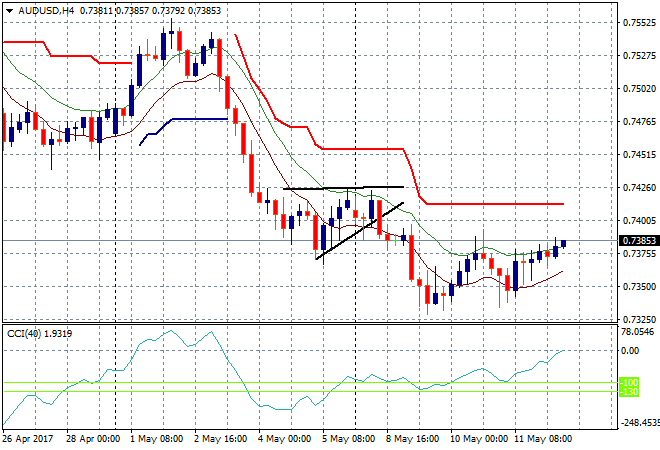

The Aussie dollar is still trying to come back, slowly lifting up to but not above the 74 handle against USD through today’s session. Short term price patterns plus the lower momentum reading suggest this could follow through but the bears remain in charge in the medium term:

The data calendar concludes the week with three major releases. First, its German GDP for the 1Q then the one-two punch of US CPI and advanced retail sales for April.