by Chris Becker

Outside mainland China, stocks are up across the Asian region with political and macro events once again overshadowing markets. The fallout from Trump’s firing of the FBI director and the sabre rattling from North Korea were distractions as commodities tried to regain from their recent losses while the USD itself remains strong against the majors.

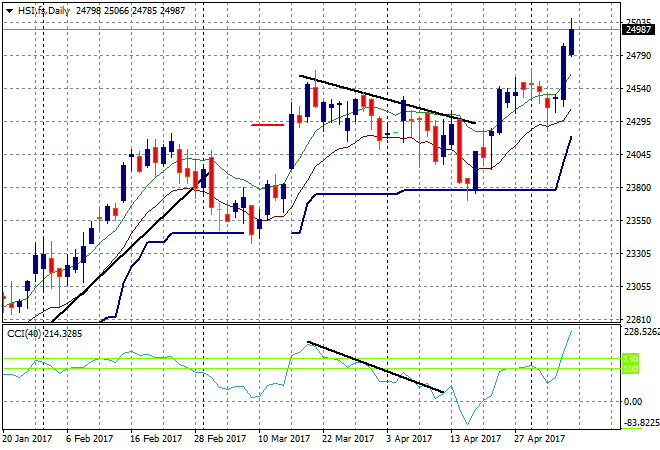

In China the Shanghai Composite is currently steady going into the close, now at 3075 points it remains well under threat from further falls as regulators continue to tighten the reins. The critical support level at 3100 may turn into strong resistance soon. Other Chinese markets are doing quite a lot better with the Hong Kong based Hang Seng up 0.7% to be above 25000 points for the first time since mid 2015. As always I’m distrusting of this overbought type of move but buying new highs is almost always better than trying to short them!

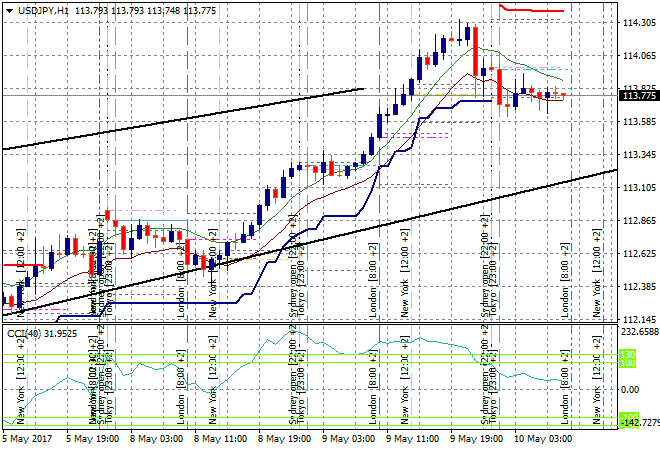

Japanese stocks had a modest session as their corporate earnings season gets under way with the Nikkei taking back it previous session losses to be up 0.3% but still just below the 20,000 point line. The Yen is remarkably stable with the USDJPY pair remaining below the 114 handle in a mild retracement after the big run up at the start of the week:

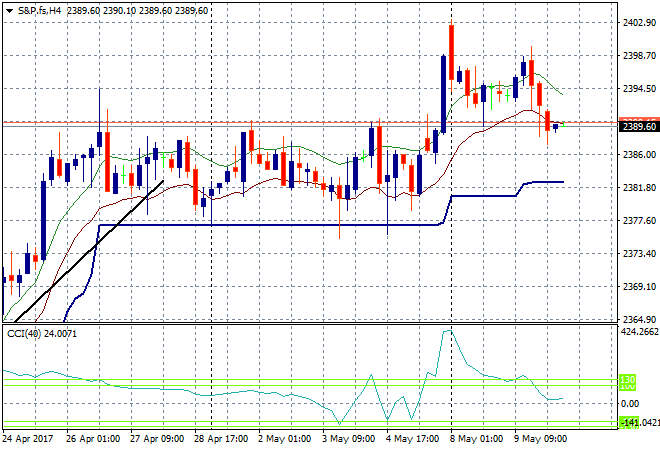

S&P futures are dropping slightly on the domestic political risk front as yet another new round of corporate earnings awaits, these are likely to be ignored as Nixon 2.0 fills the newswires:

The ASX200 closed 0.6% higher to finish at 5875 points, taking back all of yesterdays small dip and absorbing the Budget with aplomb. Most of the major banks were off slightly due to the Budget measures but this was offset by iron ore miners have another day in the sun, with Fortescue rising over 5% and near 2% rises for BHP and RIO.

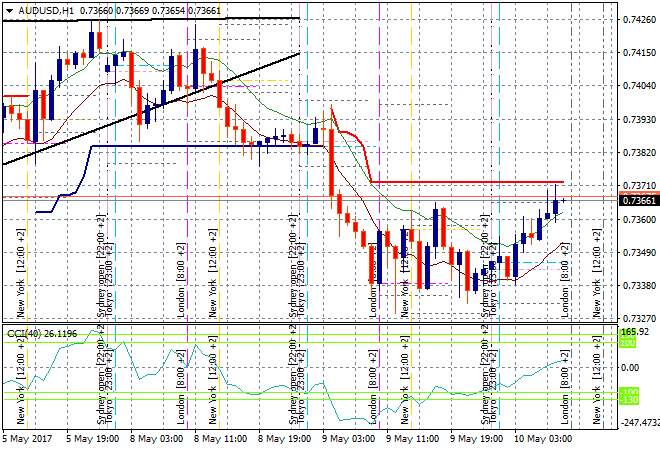

The Aussie dollar is coming back slightly after being crushed by yesterdays poor retail figures showing, currently at 73.60 and trying to beat trailing resistance on the hourly chart. The London open may put paid to that as this area is a juncture for enacting longer term shorts:

The data calendar continues tonight with another speech by Mario Draghi, this time to the Dutch Parliament, while in the US oil traders will closely watch the next round of DOE inventory reports.