by Chris Becker

A sea red across Asian bourses – except China – in a reversal of fortune compared to the start of the week as ebullience steps back a moment to regroup after the weekends macro events. Locally Aussie shares and the dollar are reacting poorly to a lacklustre retail data print while the commodity complex is desperately trying to find a bottom with iron ore slipping once again and oil price stabilising going into the London session.

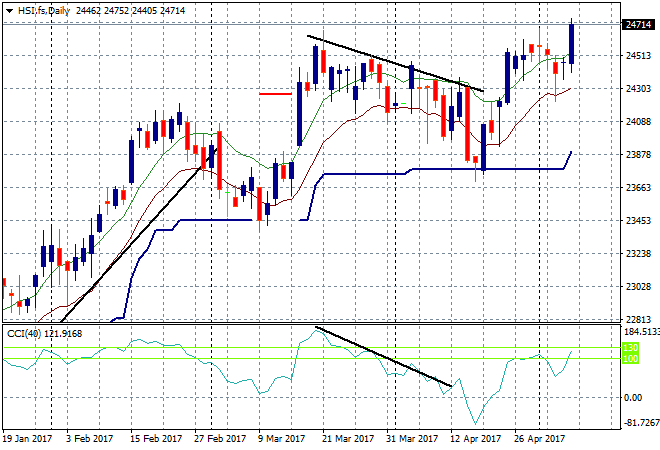

In China the freefall in the Shanghai Composite has been abated – albeit temporarily – with a deep loss after the lunch break filled by the close for a scratch session result. At 3080 points the bourse is still well below critical support at 3100. The Hang Seng is up over 1% in a surprise move with the bearish double top pattern on the daily chart proved incorrect with a new daily and yearly high!

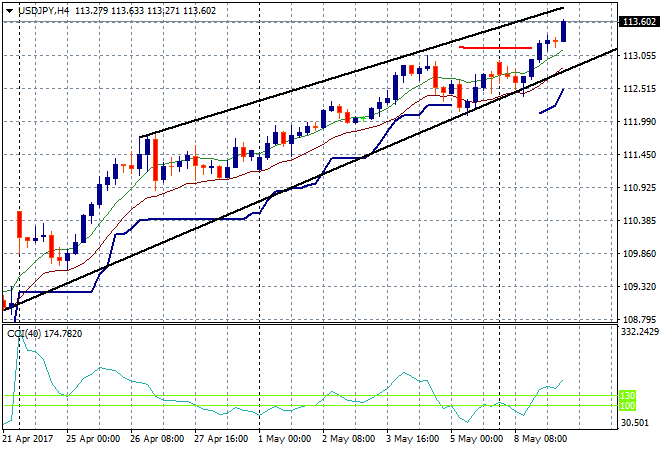

Japanese stocks slipped only a little after the big jump on the return from last week’s holiday with the Nikkei pulling back around 0.3% to remain below the 20,000 point line. The Yen continues to sell off amid USD strength with the USDJPY pair now zooming well above the 113 handle and hitting the top end of its trend channel:

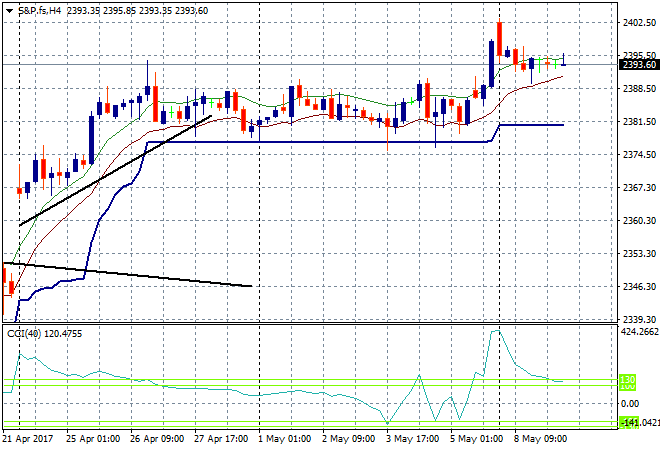

S&P futures are steady – in fact almost lifeless going into the more heavily traded NYLON sessions, as a new round of corporate earnings awaits:

The ASX200 closed 0.5% lower to finish at 5839 points, taking back almost all of yesterdays bullish post-weekend move. This was mainly on the back of another bank, this time CBA which disappointed with its profit announcement, falling nearly 4%, dragging the other divisions of Megabank down with it.

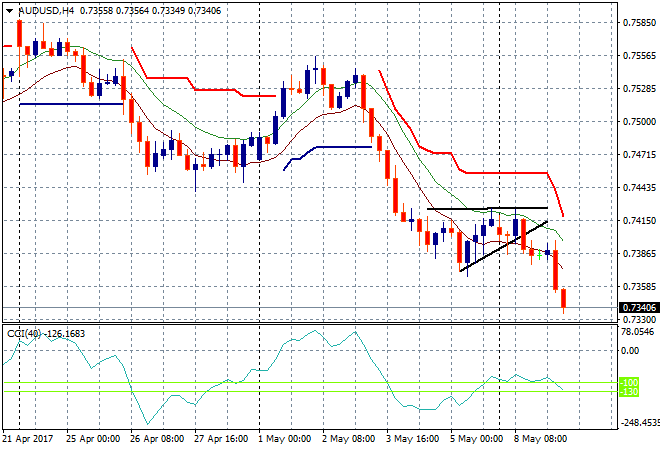

The Aussie dollar has been crushed by the poor retail figures showing, sold off immedaitely below last week’s intrasession low at 73.50 to be at 73.40 or so before the London open and looking very weak here:

The data calendar continues its post NFP quiet period tonight with a speech by Mario Draghi the only thing to be concerned about – oh and the Tweets and other pearls of wisdom emanating from the White House.