by Chris Becker

Its holiday time for most of Asia, with Hong Kong and Japanese share markets closed, the focus pivoted to China and its satellite Australia, where the latter dipped suddenly on poor earnings from ANZ and BHP. Lower commodity prices are not helping either with gold slipping and oil down before the Atlantic markets open, with share futures there not looking bullish either.

In China, the Shanghai Composite is down nearly 0.3% to 3135 points, barely holding above the level of crucial support at 3100:

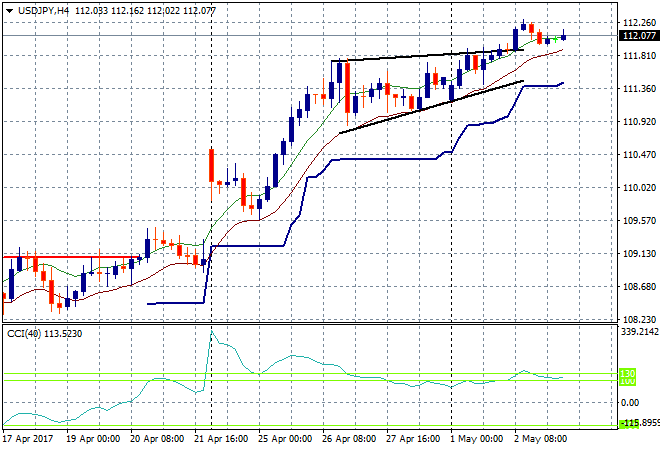

The Nikkei was closed for a holiday today. The USDJPY pair remains elevated after its recent breakout above the four hourly pennant pattern and above the 112 handle . I’m watching the low moving average carefully for signs of a reversal here:

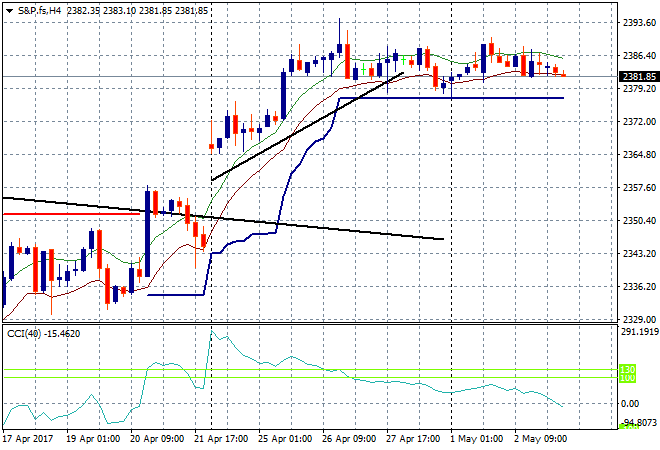

S&P futures are dragging down due to the Apple post-close earnings shocker, so I”m expecting a mild selloff at the start tonight: but not breaking out before the open as all eyes remain on corporate earnings tonight:

The ASX200 was hit hard today with bank stocks flailing around on the ANZ news and other dynamics, dragging the whole bourse down over 1% to close at 5892 points, below the 5900 level for the first time in over a week. The market remains on its bull trend channel on the daily chart, but needs to hold around the 5850 level.

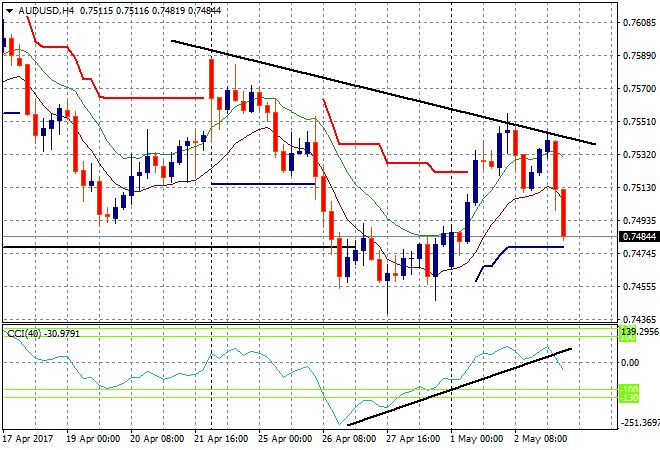

The Aussie dollar was swiftly sold off in the middle of the session, cracking straight through the 75 handle to be at 74.80 before the London open. In the lead up to the FOMC meeting this does not auger well, so I’m positioned for a possible breakdown below the 74.50 support zone, not far away at all!

The data calendar tonight is packed with German unemployment (the only unemployment print that matters in Europe), EZ Q1 GDP figures, DOE oil inventories, ISM non-manufacturing and then the FOMC meeting.