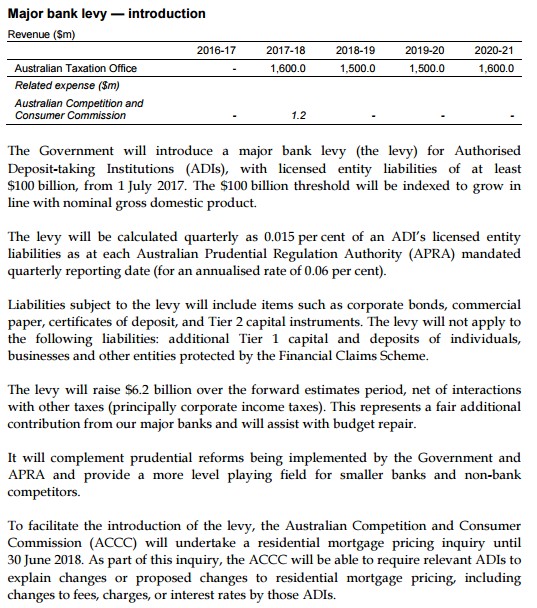

Amid the ongoing widespread bleating over the $6.2 billion bank levy (Budget measure explained below), two young commentators have risen to the top to explain why the levy is such good policy.

First, The Australian’s Adam Creighton has been quick to highlight why Australia’s banks are effectively quango organisations that operate with public support that affords them the ability to make oversized profits. Viewed in this light, the bank levy merely redistributes some of these profits back to taxpayers:

…the structure of the banking system in advanced countries such as Australia has very little to do with a free market…

For a start, government limits the number of banks by law, which boosts their profits. Banking licences are literally licences to create money (as banks simultaneously enter a loan and a deposit on their balance sheet).

The government also specifies how and what banks can sell…

On top of that the Reserve Bank provides them loans at very cheap rates and the federal government guarantees pretty much all their liabilities — a remarkable boon for banks.

To think banks can exist independently of government is a libertarian fantasy…

“When losses are borne by taxpayers, the incentives of stockholders and depositors to discipline bankers are much weaker … Australia’s banks have followed this trend, with liabilities about 20 times the value of their equity…

“Banks” are legal entities with unique government-sanctioned rights… This close relationship with government creates enormous rents or “super profits”, which aren’t eroded by competition…

The Coalition’s bank levy is the beginning of the end of the comfortable contract between the Australian government and bankers that has lasted a generation. The levy is a sign that the negotiated division of spoils among bankers, shareholders and taxpayers is going to be gradually rewritten.

Fairfax’s Jessica Irvine has made similar arguments:

…it is a nice thing, indeed, to see a policy proposal which is not only outrageously popular, but also makes good economic sense.

…the major bank’s borrowings are essentially guaranteed by taxpayers…

During the global financial crisis, the government stepped in to guarantee the deposits and new borrowings of all banks, in return for a fee. All those debts have now expired. But the banks continue to benefit from the knowledge that the government will step in again, if things go bad.

The more credit worthy they are perceived as being, the cheaper they can borrow.

And taxpayers carry the can when it all goes wrong…

It’s hard to estimate the size of the discount banks enjoy on their borrowing by virtue of the taxpayers effectively going guarantor on their loans. In all likelihood, it is much higher than 0.06 percentage points – which is all the levy seeks to recoup.

In a sense, the levy is similar to lenders mortgage insurance, which home borrowers pay when they have a deposit of less than 20 per cent.

If anyone should get this, it should be the banks which have been charging home borrowers this insurance for decades.

The bank levy is a form of protection for taxpayers in case the banks get into trouble and need their support to keep going.

Both Creighton and Irvine are spot on. The bank levy helps internalise some of the cost of the extraordinary public support that the big banks receive from taxpayers via the Budget’s implicit guarantee (which provides a two-notch improvement in the banks’ credit ratings), the RBA’s Committed Liquidity Facility, the implementation of deposit insurance, and the ability to issue covered bonds. All of these supports have helped significantly lower the banks’ cost of funding and given them the ability to derive super profits.

As noted by Chris Joye on Friday, the 0.06% bank levy is also very ‘cheap’, since it would only recover around one-third of the funding advantage that the big banks receive via taxpayer support:

If the two notch government support assumption is removed from these bonds, their cost would jump by 0.17 per cent annually to 1.11 per cent above cash based on the current pricing of identical securities. So the majors are actually only paying 35 per cent of the true cost of their too-big-to-fail subsidy…

Requiring banks to pay a price for the implicit too-big-to-fail subsidy is universally regarded as best practice because it minimises the significant moral hazards of having government-backed private sector institutions that can leverage off their artificially low cost of capital to engage in imprudent risk-taking behaviour.

Again, what better way to internalise some of the cost of the government’s support than extract a modest return to taxpayers via the 6 basis point levy on big bank liabilities?

The Turnbull Government’s unexpected bank levy announcement is the single best thing to come out of the 2017-18 Budget. It deserves widespread support from the community and parliament.

unconventionaleconomist@hotmail.com