Paul Kerin is Adjunct Professor in the University of Adelaide’s School of Economics appears at The Australian today with some atrocious gas market analysis:

LNG export restrictions recently announced by Prime Minister Turnbull were based on false premises and ignored the dynamic consequences. Consequently, they’ll diminish — not improve — Australia’s overall economic welfare.

Turnbull claimed that domestic gas prices were higher than those in markets we export to and that contract prices being offered to domestic buyers were “four or five times” US prices. However, the first claim isn’t true, while the second is dangerous and irrelevant.

Turnbull claimed that some domestic buyers were being offered prices of $20 a gigajoule, that these were “way above the export price” and “should be half that or less”. However, in doing so, he made two apples-with-oranges comparisons: long-term contract prices versus spot prices, and landed LNG prices at port versus domestic gas prices delivered to customer premises.

…I analysed the latest data available on monthly spot prices in Australia and Japan prior to Turnbull’s announcement. The average landed spot price of LNG exports to Japan contracted in March was $US6.20/MMbtu (or one million British thermal units). Adding conservative estimates of other buyer costs (such as regasification) gives a wholesale cost at distribution entry point of about $A10/GJ. That’s higher than AEMO’s average March gas spot prices at the Brisbane and Adelaide hubs for March ($A8.24/GJ and $A9.77/GJ, respectively), although below the average price at the Sydney hub ($A10.90/GJ).

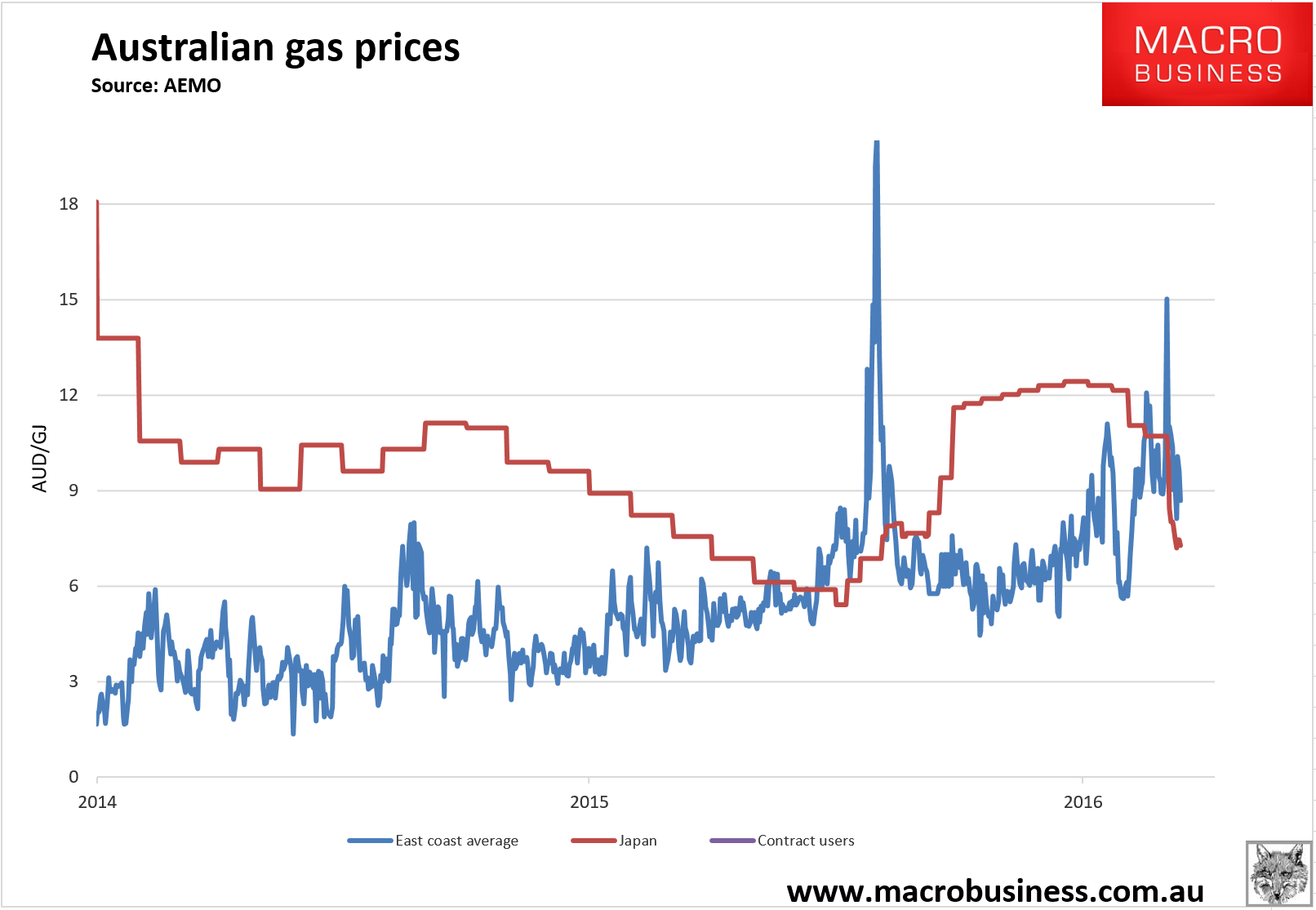

Lordy, nobody claimed that the Aussie price always above the Japanese but the longer term chart shows the trend is increasingly the case:

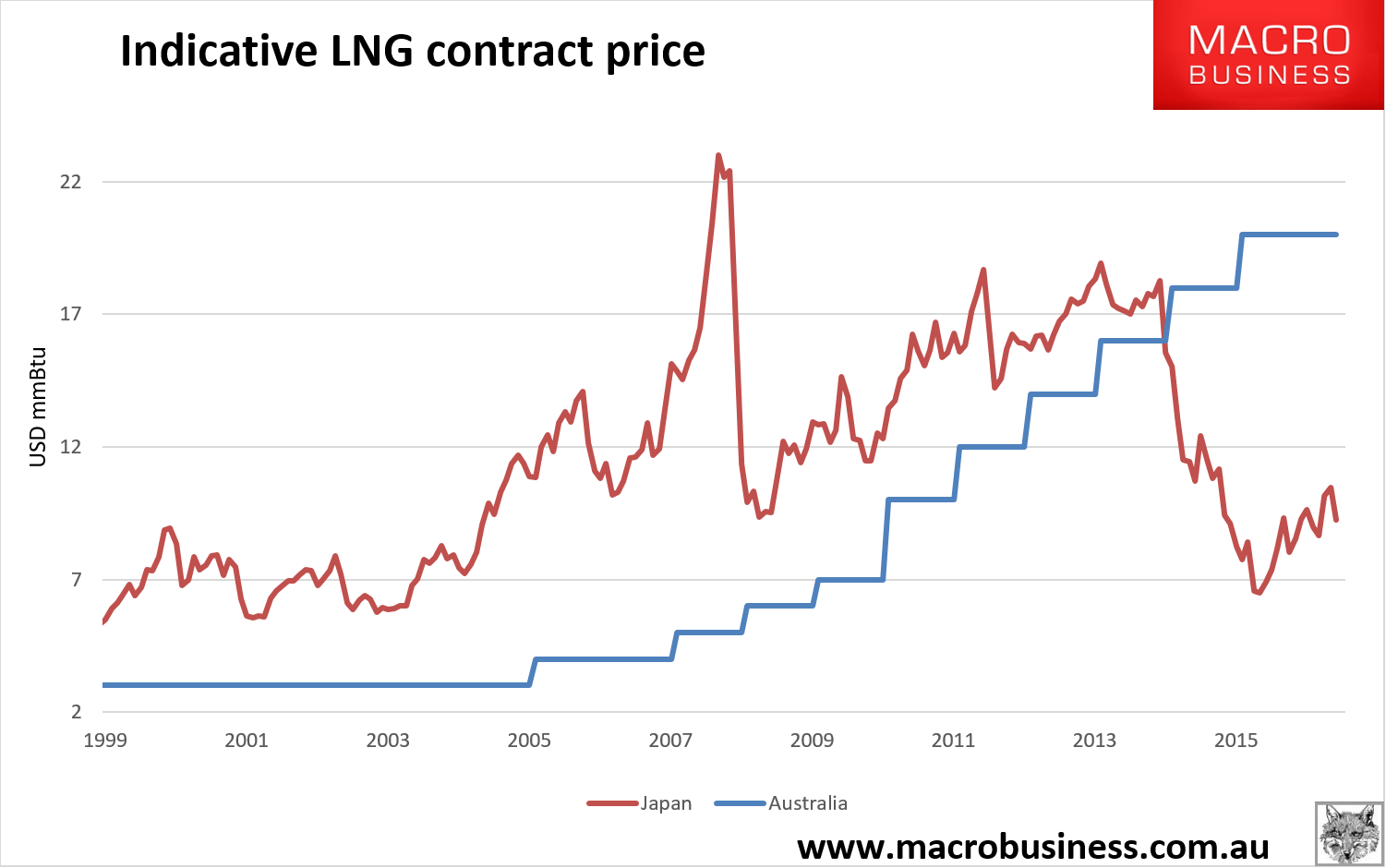

Moreover, the vast majority of volumes in both countries are traded on contracts (roughly 80%) and on that basis, bulk Australian gas consumers are paying AUD15-20Gj versus Japanese at the oil-linked price of AUD9.70Gj:

He goes on:

Further, his reference to the US is baffling. The US produces 97 per cent of what it consumes. Until now, its exports have been tiny and largely by overland pipeline. With little capacity to export or import LNG by ship, US gas prices have been driven by local factors — in particular, enormous subsidies to natural gas (including shale gas).

If Turnbull wants Australia to be like the US, here’s what he’d have to do: subsidise natural gas to the tune of billions of dollars per year and shut down Australia’s LNG export facilities. This might reduce domestic gas prices, but it would dramatically harm Australia’s economic welfare.

Jeez, professor. Australia has a gas shortage of roughly 200Gj. That is 4% of expected export volumes in 2018. Nobody is suggesting that Australia stop exporting, only that it keep the lousy 4% we need to not blow up the economy for the benefit of a gas cartel.

With due respect, professor, you’re talking rubbish.

Glencore enters the debate today as well:

Glencore has warned that Australia has drifted past a “tipping point” of industrial energy “demand destruction” and that the nation has 12 months to re-establish reliability and affordability of its base load power capacity or risk permanent and unpredictable shifts in the shape of the economy.

The commentary by the most senior Glencore executive based in Australia, global coal boss Peter Freyberg, comes as the future of the Swiss-based miner’s Queensland copper mining and processing estate is being undermined by a concert of uncertainties over the availability and price of gas and electricity supplies.

…”We have to meet Australia’s energy needs now, in five years, 10 years and 15 years. We can’t rely on blue-sky thinking. There is an energy crisis in the world’s largest exporter of coal, the second largest exporter of gas and a major exporter of uranium. We need real solutions. Unless we make decisions really quickly, and I mean in the next 12 months, that re-establish base load capacity then we have no chance of sustaining the economy in the shape that it is in now.

“In the end the market will work its way to balance,” Freyberg continued. “It will stabilise – but the wrong way and for the wrong reason. The inability to secure affordable base load supply means that the problem will be fixed by demand destruction.

“We are beyond the tipping point in terms of industrial demand destruction. And when capacity is closed and plants are shut down, they don’t come back.

“As an aside,” Freyberg added, “nationalising gas production is not the solution.

“Making sure that the incredible resources in the ground are developed is a solution. Short-term intervention is not going to fix a problem. Until gas is drilled in NSW and Victoria we will be in deep, deep trouble.”

More tripe. If the crisis is now so must be the solution. Supply responses will take years if not a decade to flow. We need them, yes, which is why reservation is not enough. We also need harsh “use it or lose it” rules to force the cartel to develop or divest reserves.