Dumbstralia really is the odd one out right now and it is going to get worse. From UBS:

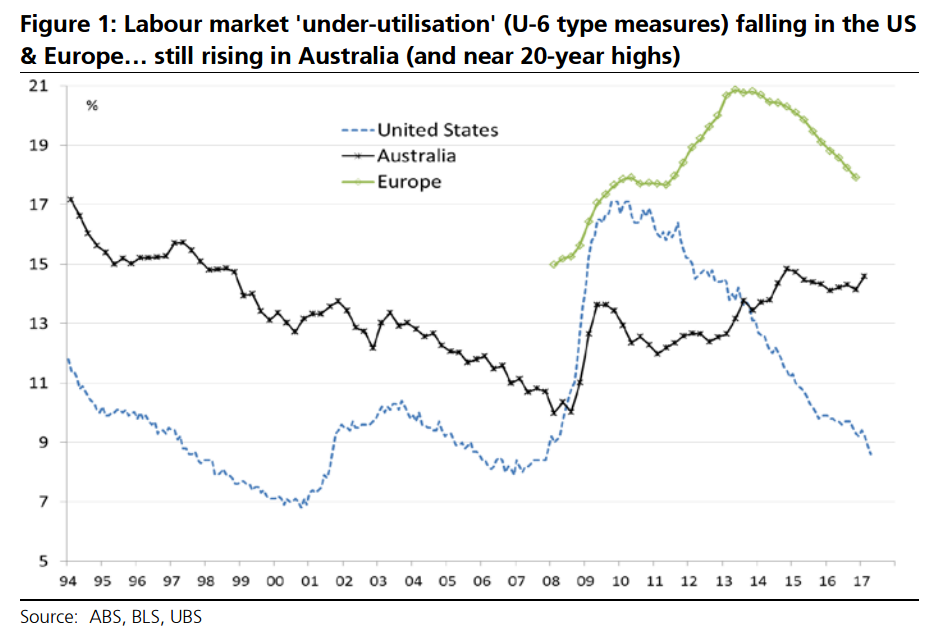

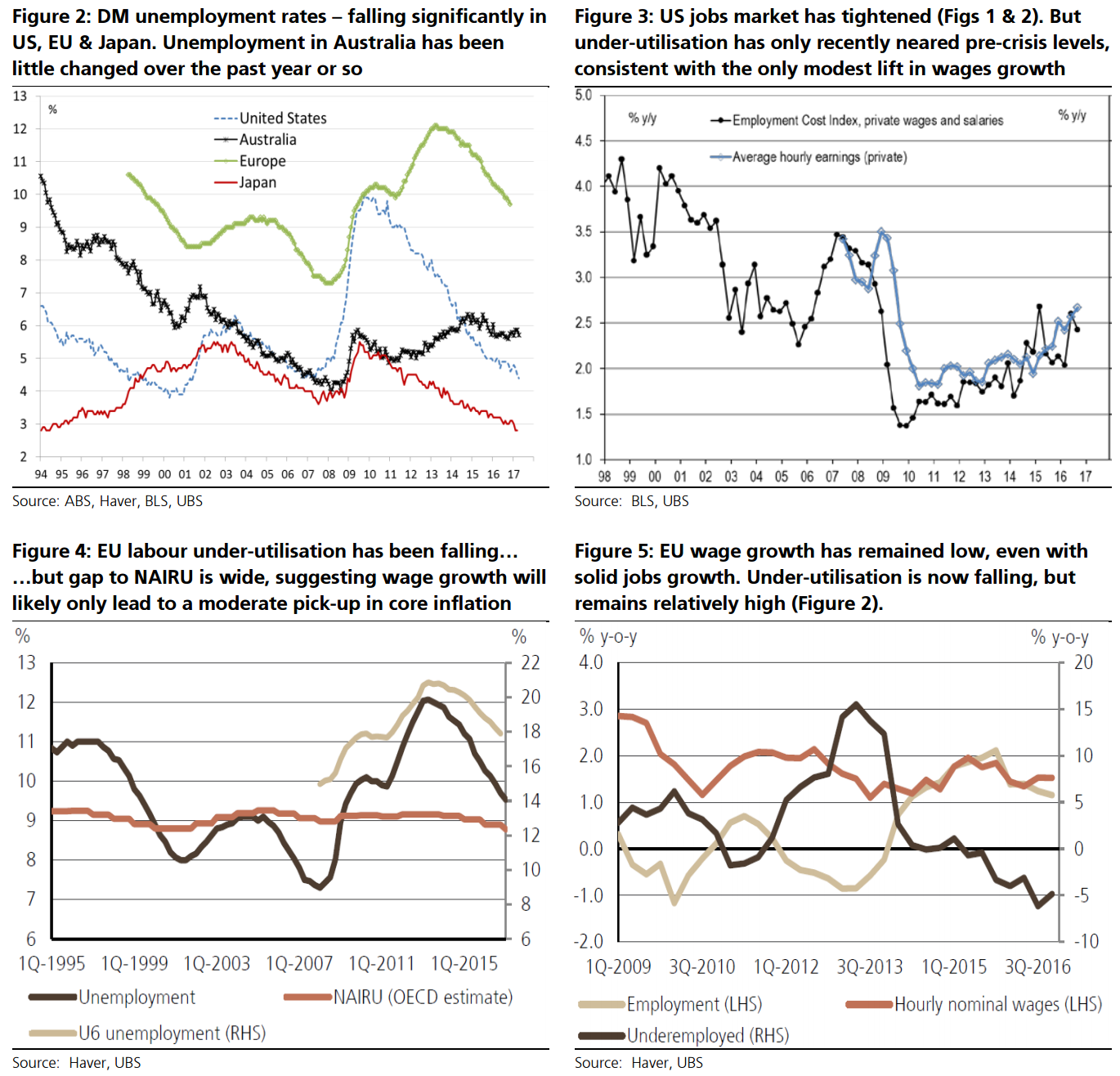

Labour slack or under-utilisation is falling in US & EU, Aust’s remains elevated Core inflation in key DM economies, while stabilising, remains subdued. And to date, there’s not been a convincing broad-based pick-up in DM wages growth that would signal global inflation pressures are building materially. One of the key drivers has likely been significant amounts of labour market slack (along with prior downward wage rigidities & weak productivity/capex). Moreover, the traditional measure of jobs market ‘spare capacity’, namely unemployment, has also likely under-estimated that slack, due to large sections of countries’ labour supply being employed, but under-utilised.

But in some key DM economies, we’re now seeing measures of underemployment falling, signalling less slack in jobs markets, which may support modestly better wage growth over the coming few years. In the US, the unemployment rate has been falling rapidly (Figure 2), having been below the NAIRU for some time (~5%, the rate below which wage pressures tend to build). But their so-called U-6 measure of labour ‘underutilisation’ has only recently roughly returned to its pre-global crisis level of a decade ago (Figure 1), consistent with the only modest lift to date for wages growth (Figure 3).

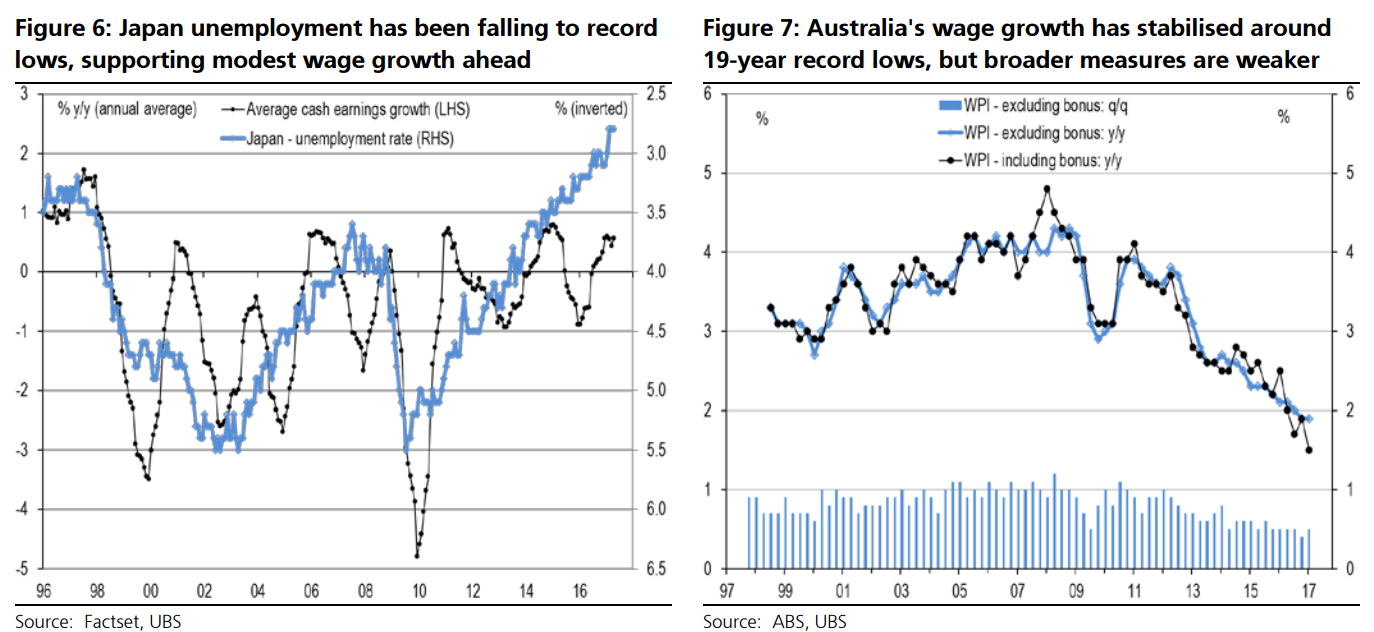

In Europe, a similar measure of under-utilisation (calculated by our EU economists), which has been very high at 21% through much of 2013 & 2014 has been falling steadily to a 5-year low of 18% (Figure 1). As our EU economists emphasise, even though EU’s unemployment rate has been falling closer to the NAIRU, it remains above it, the gap to underutilisation measures remains wide, & wages growth low (Figures 4 & 5). Nonetheless, the fall in labour market slack is encouraging. In Japan, an increasingly tight labour market (Figure 6) is also supporting modest wages growth.

However, for Australia, signs of reduced labour market slack are much less evident. As Figure 1 shows, under-utilisation is around 20-year highs, and not trending lower as in the US, Europe or Japan. Similarly, Australia’s unemployment rate (Figure 2) has also been little changed for the past 18 months, at around 5¾% (about 1%pt above latest estimates of the NAIRU). In Australia’s case, this labour market slack has been continuing to add downward pressure to wages growth. While the quarterly wage price index has steadied around 0.5% q/q, the y/y pace continues to edge low, now at 1.9% in Q117, a 19-year record low, while broader measures including bonuses look even weaker (Figure 7).

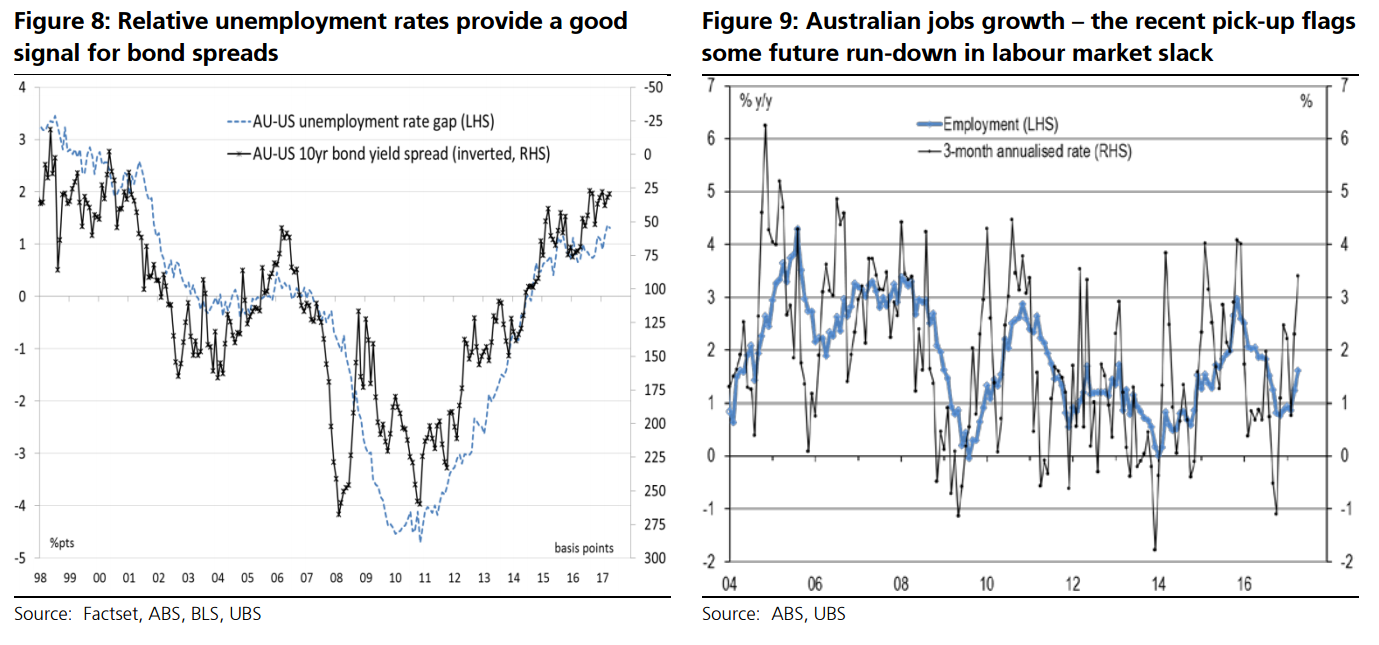

Recent jobs data for Australia suggests some easing of this downward pressure on wages over the coming year (Figure 9) with a recent strong pick-up in jobs growth, to a 3½% annualised pace over the past three months. In addition to improving leading indicators of hiring intentions, this suggests wages growth in Australia should soon stabilise, and may even drift higher over the next couple of years.

Nonetheless, with Australian wage growth to remain relatively subdued for now, it supports our ‘low inflation’ thesis for Australia, with the RBA’s preferred measures of core inflation unlikely to return to their 2-3% inflation target before 1H18, with the RBA unlikely to start its rate normalisation until very late 2018 (UBSe +25bp to 1.75% in Q418).

This suggests the RBA is likely to get successively out-hiked by the US Fed over the coming year or so, with UBS’s Fed funds forecast of 2.00-2.25% for end-18 above the RBA cash rate forecast of 1.75% (the first time since the early 2000s). This short-end compression also supports an ongoing historically tight AU-US 10-year bond spread – as does relative unemployment rate gaps (Figure 8).

Two words for ya: priced out. Instead of engineering a post-mining boom real exchange rate deflation so we could compete, win business and invest, we blew the Dumb Bubble instead and priced ourselves of a whole new set of industries too.

UBS is quite right on the implications but is far too bullish on Australia. Things will get worse before they get better here and the RBA be forced to cut rates before long.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.