■ Not cheap vs history: On traditional valuation ratios Aussie equities are not cheap. The 12-month forward P/E is currently 15.3x and the 20-year average has been 13.9x. We are not overly concerned with valuations at the market level. As we have seen that in the past this phase of the market cycle, the earnings expansion, tends to be a time of falling P/Es but rising price indices. However, we are always looking for cheap and growing stocks within the equity market.

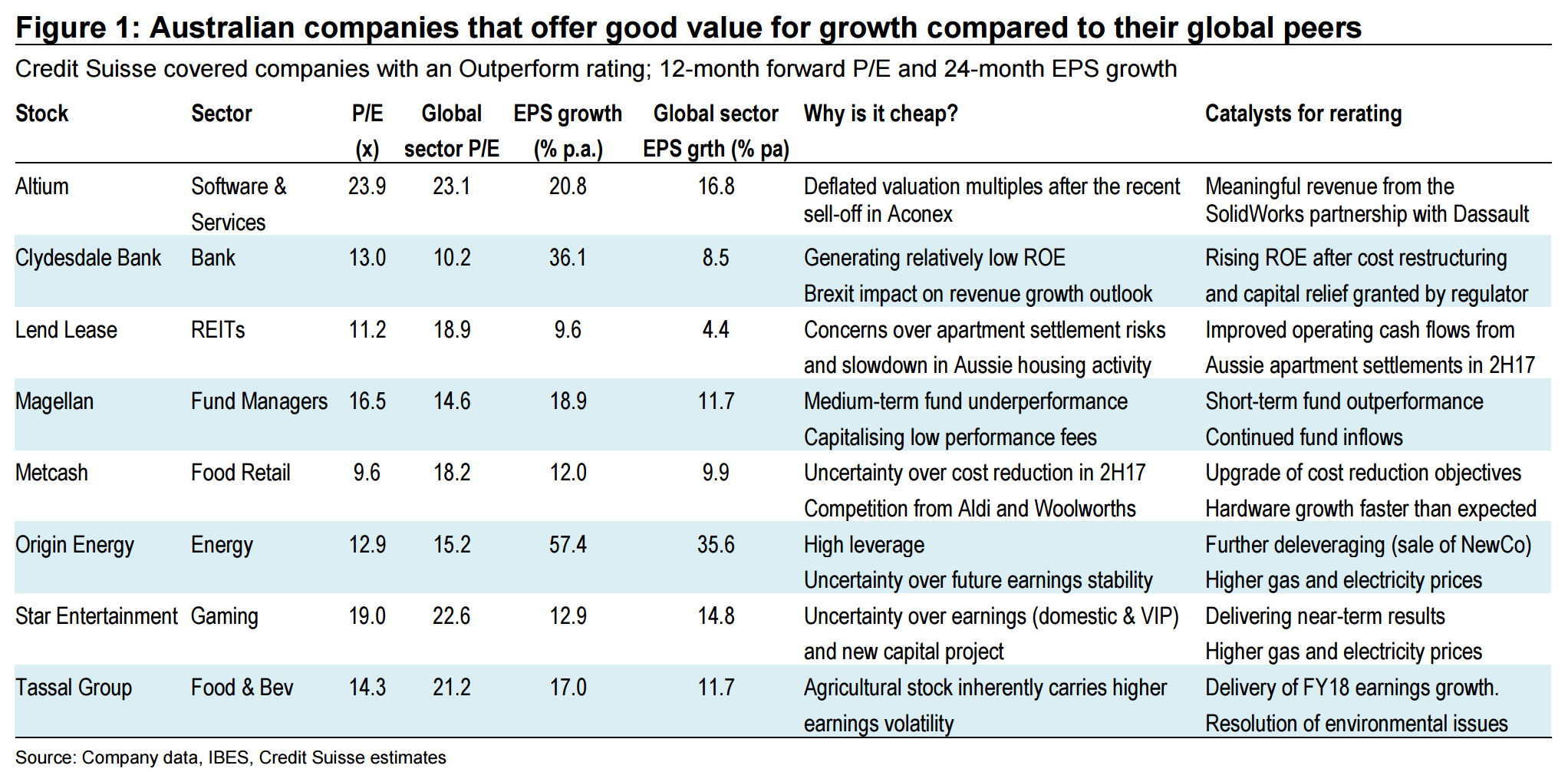

■ Cheap vs global peers: In the figures that follow we highlight Aussie stocks which look cheap on a P/E basis but are still expected to grow faster than their global peers. We recently provided a snapshot of Aussie stocks vs their global peers and here we provide an update. Our stocks trade at an average P/E of 15x but are forecast to grow EPS by 23.1% over the next two years. This compares to a global average of 18x and 14.2%.

AUD exposed stocks are worth a look but anything directed towards domestic demand is cheap (vs global peers not Aussie history) for a very reason. The outlook stinks:

China is tightening hard and the risk is growing that it is going to overshoot in addressing shadow banking;

Australia’s terms of trade are headed for new lows as iron ore crashes to nightmare levels;

the car industry is shutters;

regulators stall house prices and the dwelling construction boom tumbles;

mining investment continues to fall and there will be little offset in non-mining, and

the energy shock persists.

A little fiscal building ain’t going to offset this.

Advertisement

If you’re sick of fund managers that only swim in the cracked local fish bowl and would like to expand your investment horizons to jurisdictions where there is growth then the MB Fund (launching in the next month with 70% international stocks) is for you.

Register your interest today (if you have not already):

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.