From the excellent team of Mark Samter and Co at Credit Suisse:

What is the aim of the mechanism? Whilst the list of intended and unintended consequences from the Australian Domestic Gas Supply Mechanism (ADGSM) are potentially never ending, we do believe the most important factor to determine, as a starting point at least, is what it is actually trying to achieve. Is the mechanism just targeting supply and ambivalent to price? Or is the mechanism wanting to provide affordable gas to domestic users, with knock-on benefits for what this will do to short-run electricity prices? We aren’t policy makers and we aren’t in any sensible position to try and second guess policy makers. So we aren’t in any shape or form trying to assert the probability of either outcome happening. However, given the gravity of the situation and outcomes, it feels worthwhile to bookend the potential outcomes and understand what it could mean for our stocks.

Key points

■ The first scenario is that the ADGSM simply targets supply—i.e., GLNG, in the current form of the ADGSM at least, has to make a given level of supply available and it chooses the price (one assumes export price parity—in this instance, contract LNG price minus cash liquefaction costs only).

■ Under this scenario, on our US$65/bbl oil deck and 70¢ A$/US$ in 2018, southern states would be paying >$14/GJ for gas. GLNG feels no financial impediment. In fact, perversely, given that GLNG has the highest price contract, in an ADGSM where contract export price parity is the price they have to sell at, GLNG delivers gas ~A$1/GJ (potentially higher at QCLNG) more expensive than the other projects. In this scenario, it is hard to see $14/GJ gas being palatable for large parts of industrial demand.

■ The second scenario is that the ADGSM decides to target affordable supply—i.e., the mechanism is used to deliver gas into the domestic market at an “affordable” price. Whilst this could be done with fixed pricing, it is probably politically more palatable to just mandate a volume that has to be cleared and let market forces set the price.

■ Logic would suggest that AEMO/ACCC will err on the side of caution when determining the shortfall—i.e., it is far safer to overestimate the shortfall than underestimate it. In an oversupplied market, obviously prices will clear significantly lower. Where, in theory at least, there is a level of stabilisation to this is that a price will be hit where big industrials/retailers see prices down to where they would exercise take or pay on their existing contracts and substitute in. This should set a $6-7/GJ floor.

■ With gas ever more becoming the price setter for wholesale electricity prices, this scenario that targets prices should clearly see some material downward pressure on electricity prices. We believe that every A$1/GJ off the gas price should lead to A$10/MWh off the electricity price initially with the impact tapering as wind/solar penetration increases to 2020.

■ Whilst we do not want to drift into the politics of policy, it is of course worth noting the competing political challenges of scenario 2. Creating a lower gas price delivers huge financial benefits to large parts of the economy (including households, who of course vote) in the shape of lower gas and electricity prices. Conversely, enforcing GLNG (or others) to sell at below contract prices enforces material sovereign risk. Of course lower gas prices, along with the intervention in the market, clearly risks suitable incentives being provided to bring the much-needed future supply to market too.

■ In terms of the financial impact, for the upstream stocks scenario 1 sees theoretically no impact, whilst scenario 2 sees a material one. If GLNG is the one to shoulder the pain then vs our 2018 modelled assumptions it could lose ~A$5-6.GJ. Our best guess (which will be wrong) sees the shortage at ~50PJa in 2018, rising closer to 150PJa soon after. This could be a ~A$300mn/yr, rising to ~A$900mn/yr, problem.

■ For Utilities AGL and Origin Energy, the impact of Scenario 2 could be substantial, either through earnings and valuation, or via the observed increase in correlation of both share prices to movements in the forward curve. In the scenario modelling below, we estimate 11% of FY19 EBITDA is at risk for both Origin and AGL and 8% and 5% of the DCF value of each, respectively.

■ There is of course an option that the ADGSM is a tool that is never supposed to be used, with the threat of it sufficient to force actions to be taken by the LNG proponents. You could write an encyclopaedia on the game theory behaviour of the various parties, but we did write over two years ago on the prospect of unitising Curtis Island (Islands in the dream?)—where we were wrong there is in thinking PetroChina could take the 6th Train.

■ If contracted volumes could be permanently removed (remembering the buyers really don’t want the gas), 6 Trains could become 5 and you permanently reduce demand and bring the market back into balance.

Just what is the ADGSM trying to achieve?

Over the course of the next seven weeks, one assumes that policy makers will need to arrive at a conclusion as to what the ADGSM is actually wishing to achieve.

Whilst there are myriad intricacies, all important and with potentially huge consequences, the starting point, or mission statement, of what it aims to do is the key question. Perhaps there will be no shortage this year, and the mechanism isn’t enacted until next year. Perhaps we will get actions taken by the LNG projects that ensure there is never a shortage? But in a world where there is a shortage, winners and losers, unfortunately, need to be chosen.

Scenario 1: Ensure supply is available, but leave price alone

If the mechanism just targets the availability of gas, effectively only being concerned with a physical availability of gas rather than an affordable availability of gas, then one assumes that the LNG projects will just be told to make those volumes available at the much discussed “export price parity.”

But what do people mean by export price parity? Our assumption is that it would be the contract price minus only the cash costs of liquefaction (i.e., fuel gas, but with no recovery for sunk capital). Under this scenario, the LNG project is FCF ambivalent between selling to the export market and the domestic market and therefore under this scenario no pain is felt by Santos on the assumption it is GLNG who makes up the shortfall.

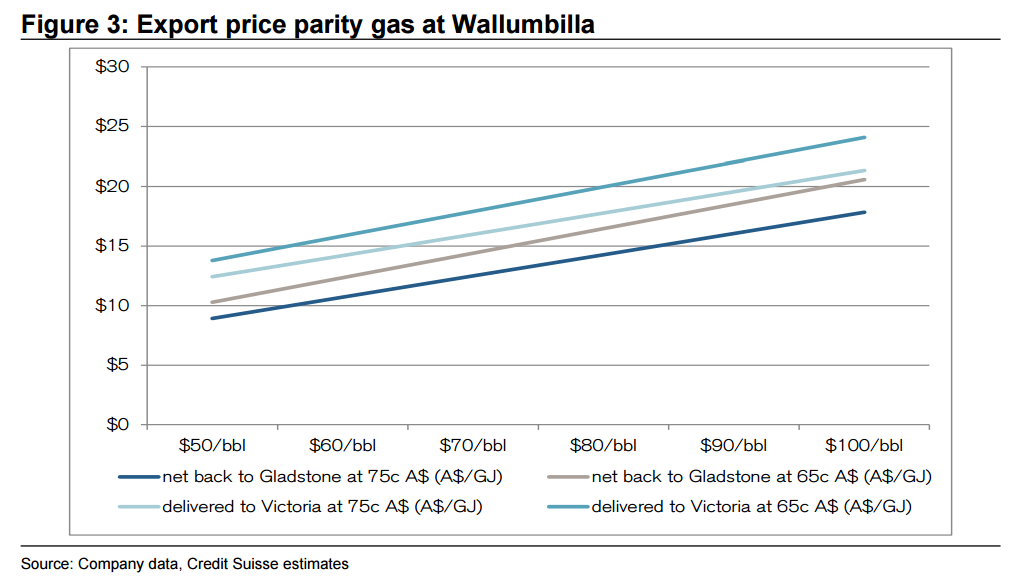

Unfortunately as we have highlighted before, Figure 3 shows that at most sensible oil price assumptions this will really do very little to provide affordable gas to the domestic market.

Of course there are different iterations of what you could deem export price parity as. Is it contract or spot prices? Should it be for the project that is being asked to divert the gas, or the lowest cost gas out of Curtis Island?

The slight perversity of the situation is that, as things stand, it appears that GLNG is expected to shoulder the whole shortfall (as the only one who isn’t a net contributor). If we are under this scenario where they just have to make gas available at their contract export price parity then, given they have the highest price contract, that will lead to a higher price than the other projects diverting the gas (and under this scenario the diverter is FCF ambivalent).

Whilst we don’t get details of contract prices, or how much QCLNG is selling spot, we do believe that GLNG is higher priced gas than both APLNG and QCLNG. Interestingly, on this basis, QCLNG could actually see a FCF gain by pricing $0.01/GJ under the GLNG export price parity as it would be realising higher FCF/GJ than its own contract price.

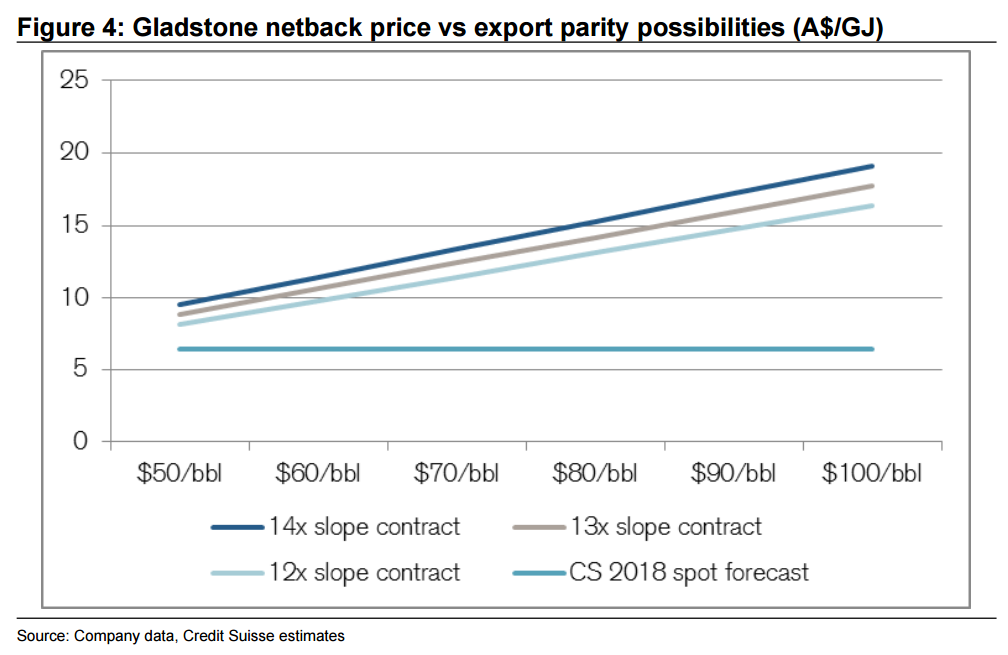

In Figure 4, we take a look at the price differential between 12-14x slope contracts and it is not inconsequential. We also look at the CS 2018 spot LNG forecast, which netback to Gladstone (Wallumbilla really) would be ~A$6.50/GJ.

The difference for GLNG having to sell at the CS spot price forecast and a 14x slope contract would be ~A$6/GJ. Clearly, if our supply shortage forecast of ~150PJa in the 2019/20 window was close to correct, that is some big spondoolies that will be lost.

Scenario 2: Ensure affordable supply is available

The other option is that this mechanism tries to alleviate the pressure on gas buyers, who have seen prices double, triple or even quadruple in some cases. So the mandate becomes to bring affordable new supply into the domestic market which doesn’t lead to demand destruction.

We will address shortly the huge impact this could have on electricity markets too, but from the perspective of the E&Ps first this clearly has the potential to cause material financial pain to any LNG project that is forced to divert gas like this.

There are a couple of ways that an impact on price could be created. The first is to just mandate a price, but one would assume this is more directionally interventionalist than would be politically desirable though.

The other way is to mandate that whatever the designated volume it has to clear domestically. In other words, you have to find a clearing price for all of the volume. If the mechanism has erred on the side of oversupplying, as it logically would, then this should a clearing price materially below export price parity.

As we discuss in this note, there is a logical argument (although logic doesn’t always prevail) that there would be some price support around the level of existing large scale domestic contracts—as those buyers would exercise take or pay on their contracts and hoover up this gas if it got too cheap. This would take us to a $6-7/GJ gas price.

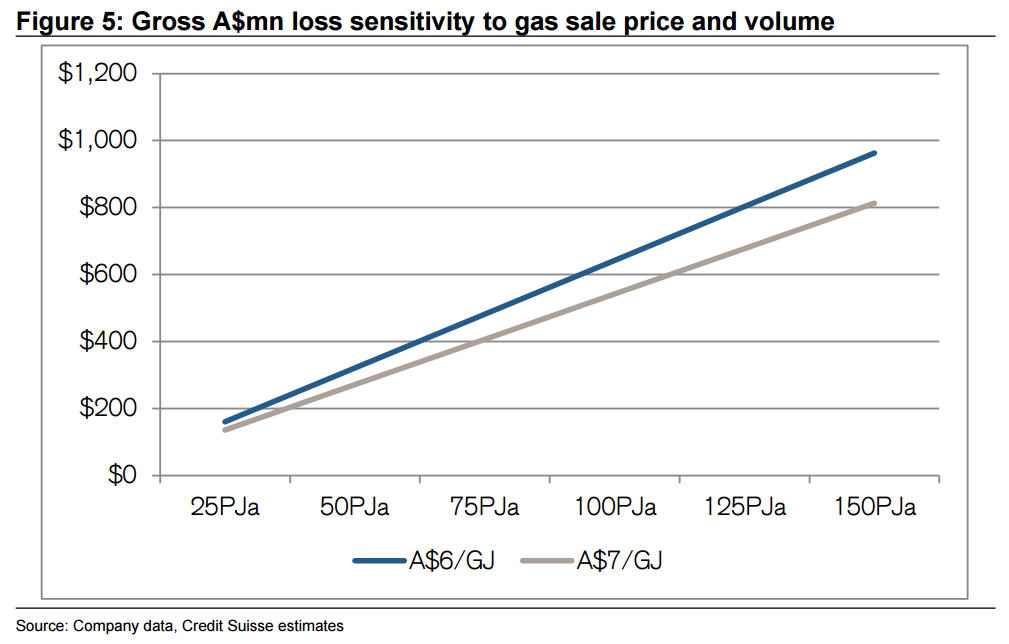

As can be seen in Figure 5, depending on the scale of the domestic supply shortfall, a very large economic loss relative to selling on contract could be felt. Clearly at these numbers, the concept of compensation, or just sovereign risk, comes into proceedings.

As we have said before, the buyers at GLNG (who are 42.5% of the JV) will realise a large economic benefit from not taking export volumes as they could either buy cheaper or not be forced to resell. If Santos were able to reprice the Horizon contract, then they get compensation too. Total remain the piggy in the middle though, and without something being done there isn’t much attractive mud for them to roll around in.

Non-trivial impact on short-term electricity prices

Gas increasingly the marginal price setter post-Hazelwood

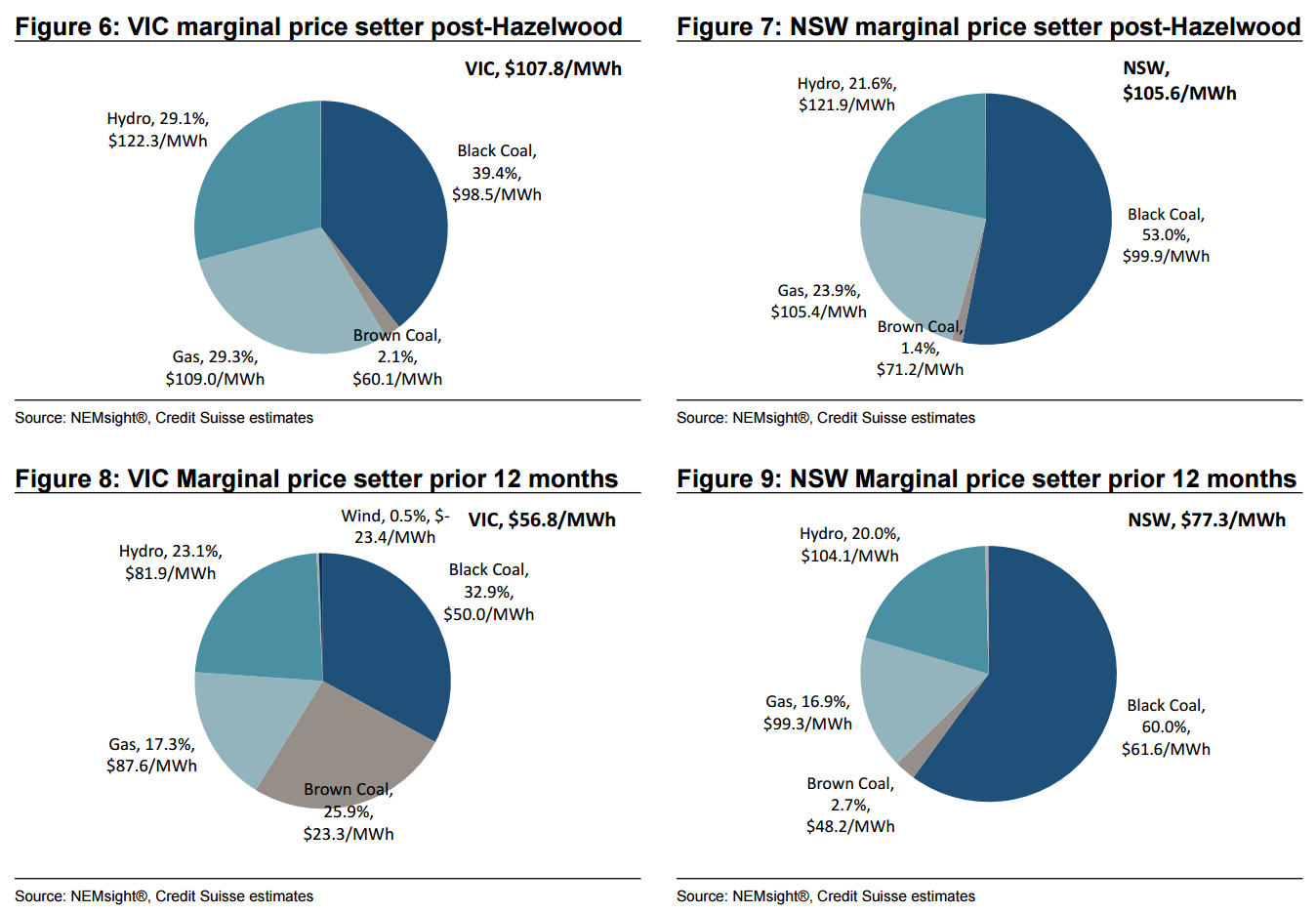

With the ADGSM, the government has a tool that could quite profoundly reduce short-term wholesale electricity prices and thus have a more broad impact on the ‘energy crisis.’ As the electricity market has tightened due to an uptick in demand and several coal closures, gas has increasingly become the marginal price setter. This is particularly true since the closure of the Hazelwood brown coal power station in Victoria in March 2017 that previously generated ~10% of total NEM demand.

As shown in Figures 6 to 9, the proportion of pricing intervals where a gas-fired generator is the marginal spot price setter in VIC and NSW has increased 12% and 7%, respectively, versus the prior 12 months.

Coal stations pricing well above short-run costs, in-line with gas short-run

The other interesting fact revealed by the charts below is that the black coal generators have increased their average bid prices approximately $40/MWh since Hazelwood closed versus the 12 months prior. An increase in benchmark export thermal coal spot prices from approximately A$70/t to A$110/t could theoretically explain up to half of this increase, though in practice the ability of most coal stations to opportunistically buy significant incremental spot coal volumes is limited.

A more likely explanation is that the black coal generators have responded to the tighter market balance by pricing their output just below the next highest bidder, which is gas.

Arguably, Hydro has also increased the value they place on their water reserves in response to expectations of higher prices based on higher gas prices.

Expect 1-for-1 proportional change in short-term gas and electricity prices

As such, a change in gas prices is likely to have a significant impact on electricity prices far beyond what could be explained by its average contribution alone. We would expect almost a 1-for-1 relationship; i.e., a 1% decrease in short-term gas prices could reduce short term electricity prices. Or, a $1/GJ reduction in short-term gas prices may result in a $10/MWh decrease in short term electricity prices.

This effect should lessen over time as the electricity markets current dependence on gas for both energy and capacity reduces over time with the increasing build of wind and solar.

Risks to share prices through increased correlation to electricity futures

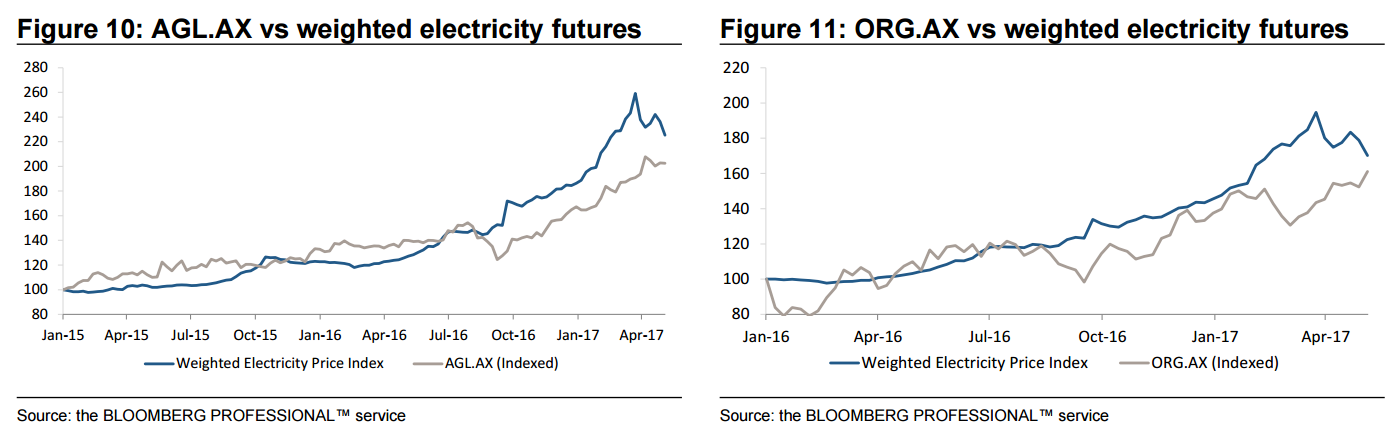

We endeavour to provide some earnings and valuation sensitivities to a Scenario 2 type outcome in the pages below. However, on the surface, the increased correlation of both AGL and Origin’s share price to movements in the electricity futures—as shown in Figures 10 and 11 below suggests that a risk to short-term electricity prices represents a risk to equity market valuations.

CS cut ratings ORG and AGL as well.

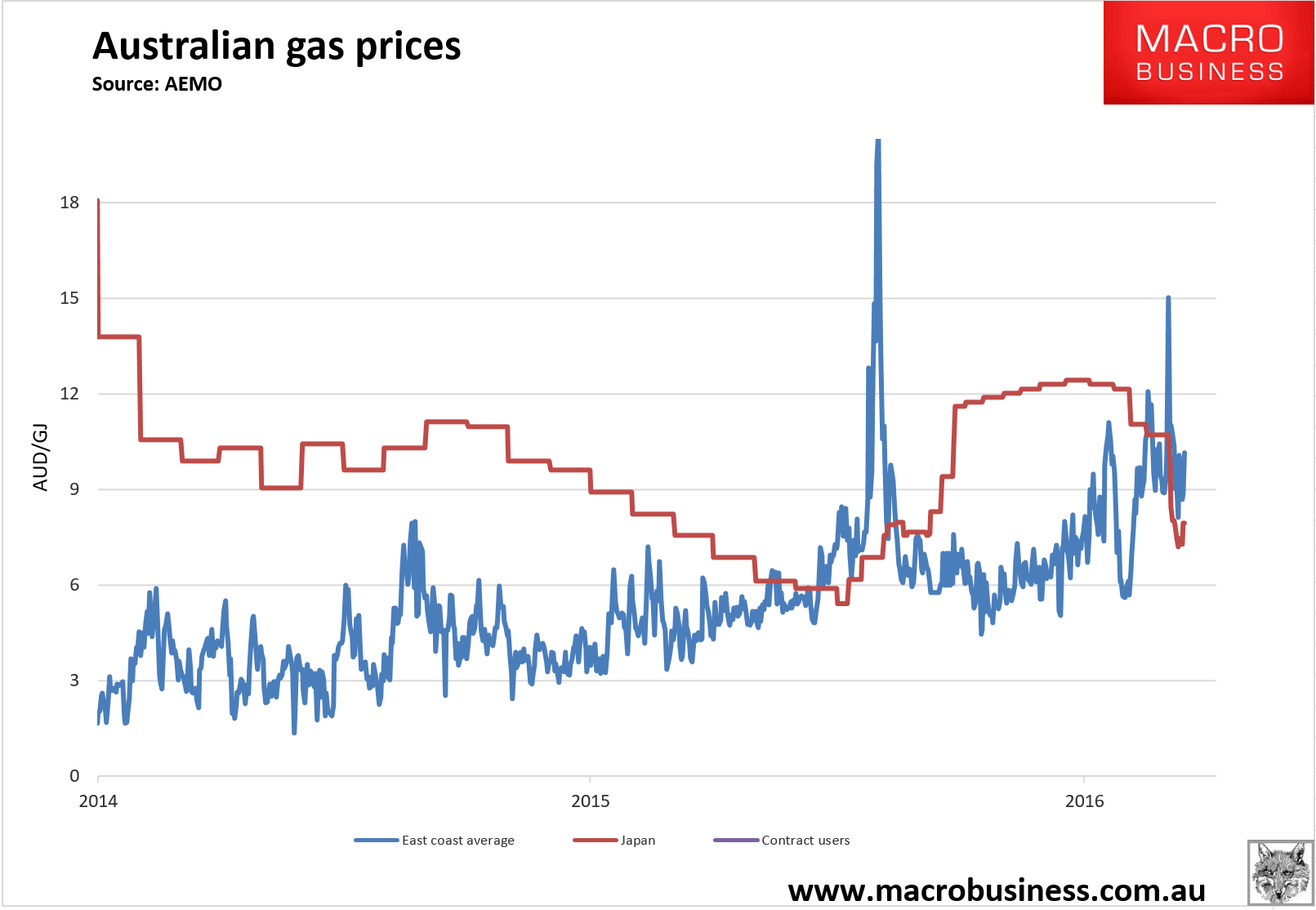

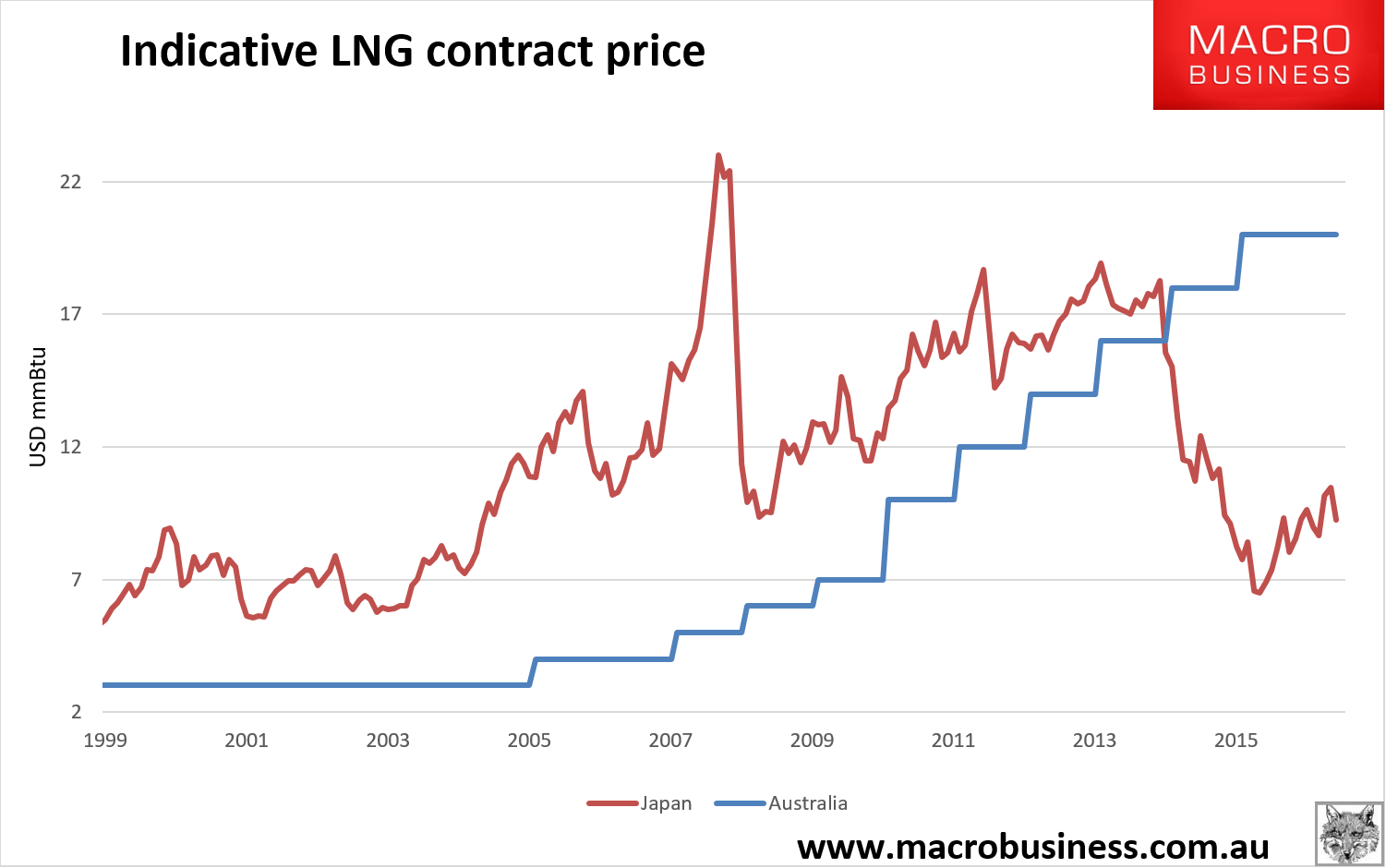

In case you’re wondering, local gas spot prices remains miles above Japanese today:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.