RBA Governor Phil Lowe’s speech yesterday on household debt an house prices once again pinned Australia’s housing woes on the imbalance between supply and demand, as housing and infrastructure has failed to match strong population growth:

The supply of well-located housing and land in our cities has been constrained by a combination of zoning issues, geography and inadequate transport. Another related factor was that our population was growing at a reasonable pace…

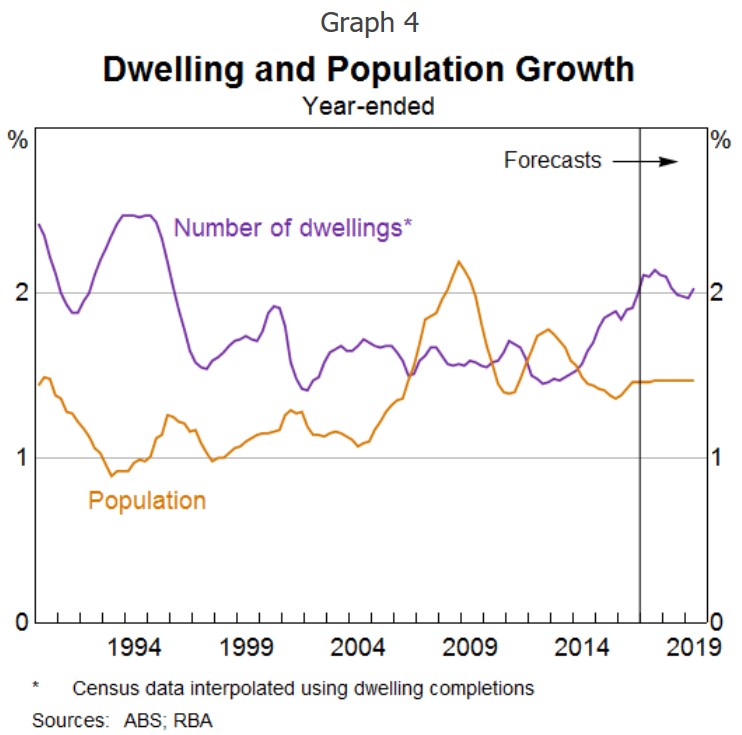

Population growth picked up during the mining investment boom and, although it subsequently slowed, it is still around ½ percentage point faster than it was before the boom (Graph 4). For some time the rate of home-building did not respond to the faster population growth; indeed, the response took the better part of a decade. The rate of home-building has now responded and we are currently adding to the housing stock at a rate not seen for more than two decades. Over time, this will make a difference.

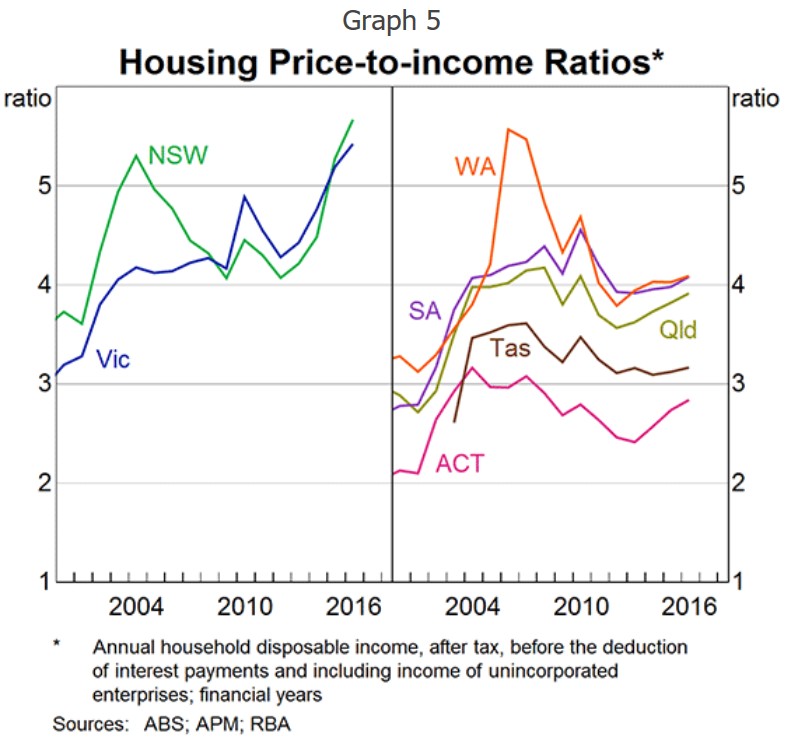

It is Melbourne and Sydney where population growth has been the fastest over recent times. Not surprisingly, it is these two cities where the price gains have been largest, and these price gains have helped induce more supply. Indeed, Victoria and New South Wales account for all of the recent upward movement in the national housing price-to-income ratio (Graph 5).

…increased supply and better transport could be expected to help address the ongoing rises in housing prices relative to incomes…

In the Q&A, Lowe also argued that “if you can increase the supply of well-located land, then the average price of residential land that goes into house and land would be less”. So clearly, Lowe believes that the best solution to solving Australia’s housing woes, especially in Sydney and Melbourne, is to boost supply – i.e. the quantity of well located land and the number of dwellings – via expanding infrastructure investment.

Lowe’s latest comments follow those made in last month’s speech, whereby low also blamed Australia’s housing woes on an imbalance between supply and demand [my emphasis]:

Advertisement

…as is often the case in economics, it [the housing market] largely comes down to supply and demand. On the demand side, population growth in Australia – especially in our largest cities – picked up unexpectedly in the mid 2000s and it is only in the past couple of years that the rate of home building has responded. This imbalance was compounded by insufficient investment in the transport infrastructure needed to support our growing population. Nothing increases the supply of well-located land like good transport links. Underinvestment in this area is one of the factors that has pushed housing prices up. Put simply, the supply side simply did not keep pace with the stronger demand side. The result has been higher prices…

It is hard to escape the conclusion that we need to address the supply side if we are to avoid ever-rising housing costs relative to our incomes and to avoid the attendant incentive to borrow that is created by rising housing prices”.

What I find most irritating about Phil Lowe’s musings is that he acknowledges that Australia’s mass immigration program has helped create the supply-demand imbalance, especially in Sydney and Melbourne, but won’t countenance cutting immigration to historical norms to take the pressure off housing and infrastructure.

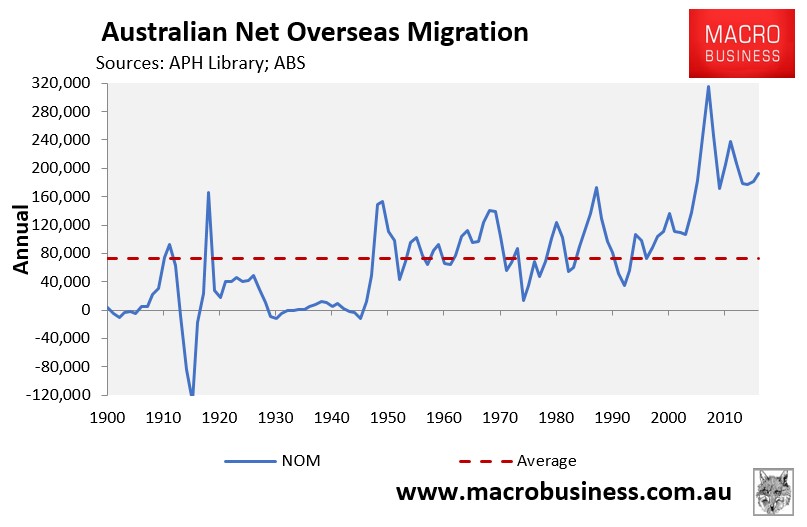

Blind Freddy can see the massive ramp-up in net overseas migration (NOM) in the early-2000s:

Advertisement

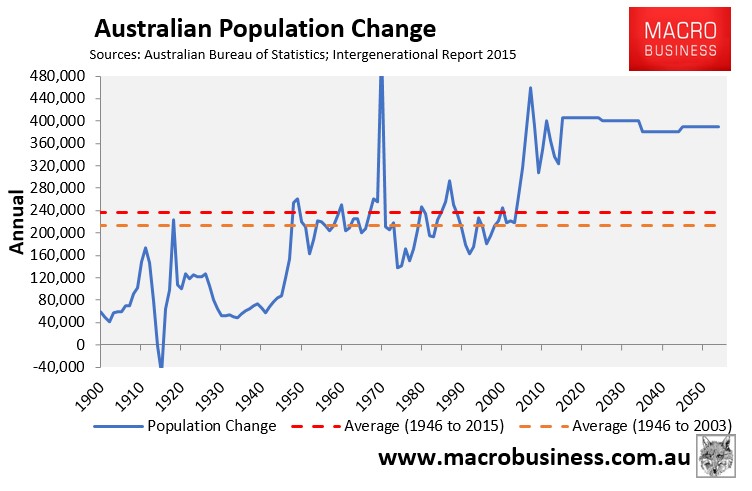

That has driven the huge growth in population, which is projected to continue long into the future on the back of continued strong migrant inflows:

Advertisement

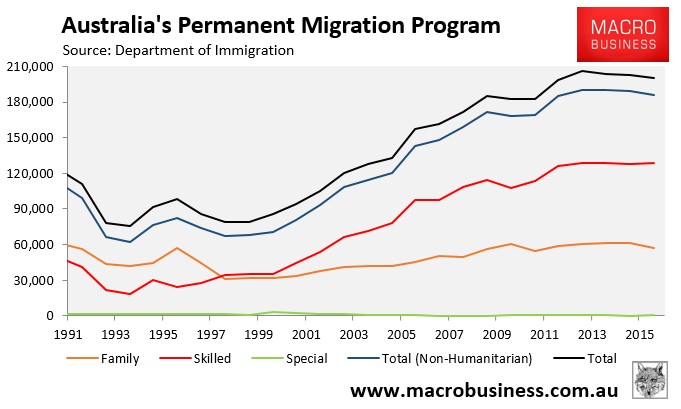

Rather than being “unexpected”, the huge lift in immigration was a deliberate policy choice made first by the Howard Government and continued by subsequent federal governments. We know this because the permanent migrant intake was massively increased in the early-2000s from less than 90,000 to 200,000 currently:

Given mass immigration has caused the supply-demand imbalances for housing and infrastructure in the first place, it would seem that an obvious solution to the problem is to reduce immigration back to long-run norms?

Advertisement

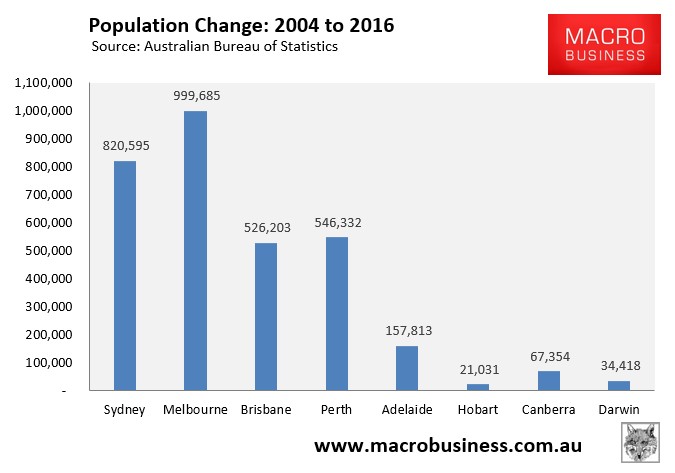

As noted by Phil Lowe, the Australian housing market is primarily a problem in Sydney and Melbourne. Both have been the primary destination of migrants, which has seen Melbourne add a ridiculous 1 million people (a 27% increase) over the past 12 years, whereas Sydney added 821,000 people (a 20% increase):

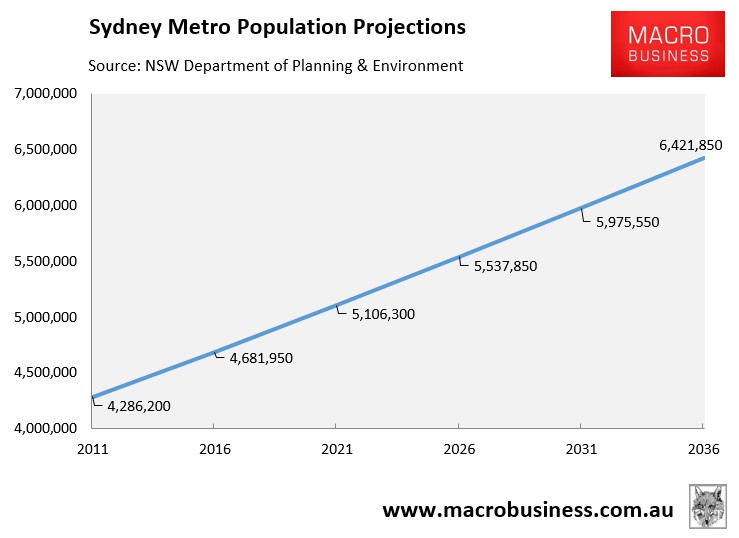

Because of mass immigration, Sydney’s population is projected to grow by 87,000 people per year (1,650 people each week) to 6.4 million over the next 20-years – effectively adding another Perth to the city’s population:

Advertisement

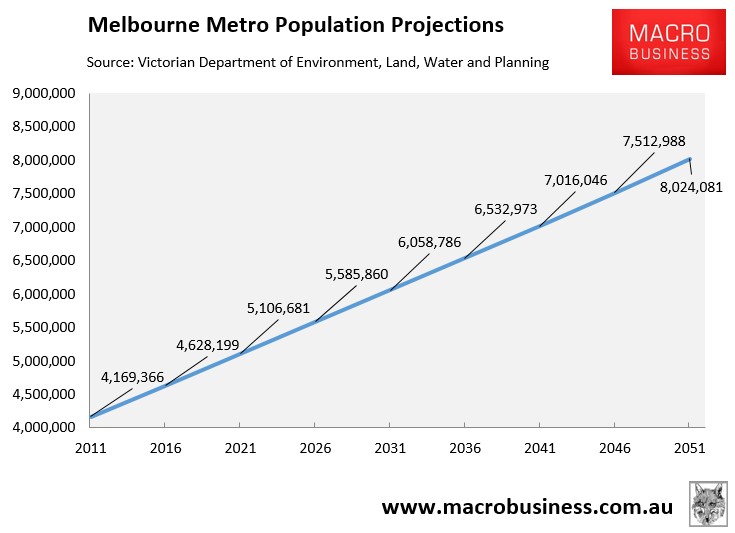

Whereas Melbourne’s population is projected to balloon by 97,000 people per year (1,870 people each week) over the next 35 years to more than 8 million people – effectively adding 2.5 Adelaide’s to the city’s population:

Advertisement

Yet, despite these startling figures, Phil Lowe, the Turnbull Government, and others continue to pin the blame for Sydney’s and Melbourne’s housing crisis on dwelling supply not keeping up with demand – completely ignoring mass immigration’s preeminent role in the matter.

The fact remains that it is a direct policy choice how ‘big’ Australia becomes, not a fait accompli.

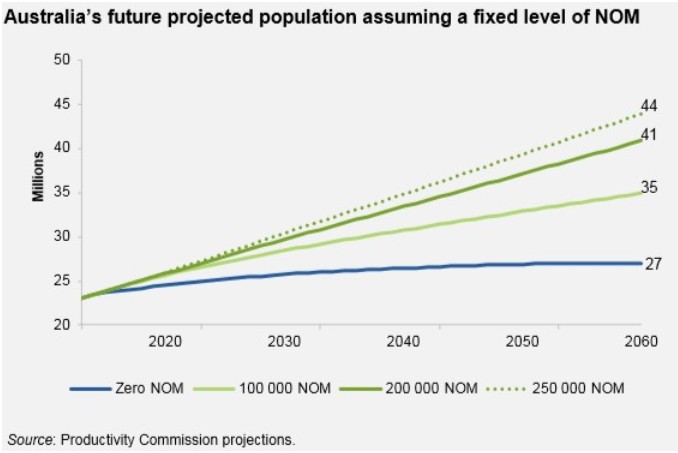

As shown in the next chart, which comes from the Productivity Commission, Australia’s population will reach more than 40 million mid-century under current immigration settings, at least 13 million more than would occur under zero net overseas migration (NOM):

Advertisement

That’s a helluva lot of extra people to build infrastructure and housing for versus a lower or zero NOM policy.

Instead of hand-wringing over Australia’s housing crisis and inadequate infrastructure investment, how about Phil Low, our politicians, policy makers and the media instead question Australia’s mass immigration settings, which are the demand-driver causing the problems in the first place? Why not include as a solution reducing immigration back to the long-run norms?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.