China’s banking regulator ordered owners of the nation’s 68 trust companies to be prepared to provide funding or sell their stakes as the risk of defaults rises in the $1.9 trillion industry for high-yield investment.

The China Banking Regulatory Commission told trust companies to either restrict their businesses and reduce net assets or have shareholders replenish capital when the firms suffer losses, according to an April 8 notice that was seen by Bloomberg News. The regulator will also impose a “strict” approval process on trust firms’ entry into new businesses and products starting this year, according to the document.

After a brief crackdown, the trust business was up and running again.

The China Banking Regulatory Commission’s guidance covered real estate and other industries facing overcapacity, according to people familiar with the matter. The CBRC will take action against disguised property financing by the 20 trillion yuan ($2.9 trillion) trust industry, including lending through partnerships, asset management plans or related businesses such as suppliers, the people said.

This crackdown is now underway after it revived in the first quarter.

China Securities Journal reporter was informed that the recent CBRC to the banking regulatory authorities issued “2017 trust company on-site inspection points.”

01 Whether through the combination of equity and debt, partnership business investment, the proceeds of receivables and other modes of disguise to the real estate development enterprise financing to circumvent regulatory requirements, or to assist other institutions to carry out real estate trust business.

02 Whether there is a real equity or creditor’s rights in the project of “stock + debt”, whether there is a situation where the real estate enterprise acts as a beneficiary of the shareholders’ borrowing, whether or not it is disqualified in the name of the shareholder’s loan.

…Industry sources said that as other financing channels are limited, the trust company to become an important channel for real estate developers to finance. But this document issued after the trust company to carry out the current financing business is facing tightening. This means that real estate financing and an important channel is being tightened.

This means that after overseas bonds were halted, developers through the trust company financing this important channel also suffered tightening.

Wall Street on Monday mentioned that trust financing is the main financing of housing loans in addition to bank loans, with the main financing channels have been limited real estate, real estate trust business quietly warming.

“Economic Reference” quoted data pointed out that this year, 68 trust companies issued a total of 326 real estate trust products, the cumulative financing for housing enterprises 100.55 billion yuan; May real estate trust issue is still “increasing.” Up to now, May housing prices through the issuance of collective trust fundraising project has reached 11.37 billion yuan. May 13 to May 19 of the week, a total of 24 trust companies issued 39 sets of trust products, the number of shares increased by 11, an increase of 39.29%. Among them, 10 for the real estate projects.

…Wall Street.cn mentioned at the beginning of the month, since the beginning of the year, Vanke and R & F and other housing prices have canceled the debt, involving the amount of at least 50 billion yuan. The two companies in the cancellation of the announcement said that in view of the recent changes in the market, decided to cancel the issuance of medium-term notes, Vanke more twice to cancel the issue of medium-term notes.

In fact, the plight of developers emerged in the fourth quarter of last year. Hai Tong Securities analyst Jiang Chao, Zhou Xia and Zhu Yixing in the report pointed out that the quarterly real estate bond issuance and net financing was only 30% of the third quarter, mainly due to the tightening of corporate bonds. From November last year to the end of February this year, real estate corporate bonds issued only 29.

Tightening of credit revived the trust sector loans to real estate, hence the crackdown.

“There are indications that regulatory measures to curb system-wide leverage show unintended consequences; specifically, in reviving ‘core’ shadow banking activities that had previously been constrained by regulation,” said George Xu, Associate Analyst at Moody’s Investors Service.

Moody’s said borrowers in sectors such as property, local government financing vehicles and industries struggling with overcapacity faced reduced access to traditional bank loans and were being driven to trust loans.

We’ve seen this all play out before, in 2013 and 2014. Right after the Taper Tantrum in the U.S. came China’ cash crunch. From June of 2013 through all of 2014, there was an attempted deleveraging. The result was falling home prices, panic, and the final massive monetary emission in early 2016. Now we’re back to seeing a crackdown, complete with signs of periodic cash crunches such as in March. What’s different from 2013 is the scale of the problem and the severity of the crackdown. The commodity, real estate and currency market declines from 2014-2016 will be dwarfed by what follows.

Meanwhile, Bankers are reigning in lending and hoarding capital as banks’ cost of capital exceeds loan rates. Bankers are even delaying loan disbursement unless customers accept punitive hikes in loan costs. Banks are hoarding capital, with tight credit expected in June (MPA assessment), July (WMPs coming due) and even as far out as September (quarter end).

The article below interviews bank president Mr. Zhang, who has approved 2 billion in loans but refuses to release the funds. He tells the customers wait a little longer, but the funds are never coming unless the customer takes his hint that the cost of funds will soar.

Zhang is a member of the assets of 200 billion yuan level of the city branch of a branch of the vice president, in charge of corporate finance. It is his duty to maintain a good group of companies with a high profile contribution, but now that the loan business has given way to the second quarter of the macro-prudential assessment system (MPA) Has been dubbed the “debt shortage” of the tight liquidity trend, so that the price of capital is steep rise in the spread, so that the head office “under the death order” liquidity control.

“Bringing in capital is the top priority.” Zhang told the first financial reporter, the head office has just released what they call the “history’s most stringent” liquidity control program. All business units, all branches should defend themselves.

Bankers are refusing to lend to big real estate borrowers even if loans are approved. They’re also telling them they can rollover their debts, but after collecting payments, refuse to lend. Later in the article, Zhang says he’s received a loan quota and cannot exceed it. Effectively he cannot loan, and if the number drops, he needs to find some way to raise capital or cut lending.

If there are still funding gaps, but have to give the loan, how to do? Zhang is not frustrated to tell the first financial journalists, in accordance with the spirit of the head office, the cost of this loan will be “punitive” to add 200 basis points.

“If the cost bank capital is 5%, and this goes up again by 200 basis points to 7%, now a one-year loan was 4.35%, even if rate is hiked 50% I’m still losing money.”

SHIBOR rose higher on Tuesday, climbing above the prime rate, and it’s now approaching the central bank’s 1-year rate.

Money isn’t very tight at the moment, but bankers are hoarding capital in preparation for the MPA in June, and expect tight conditions in July and again at the end of September.

Originally, Xiaopeng they are only in the row of assets and liabilities positions under the baton, ahead of hoarding money. In other words, the tight is not the moment, but for the future will be “lack of food” is expected – 6 at the end of the year to deal with the MPA assessment, in July Xiaopeng where the bank has a group of financial maturity, the end of September liquidity Gap is not small.

You can imagine, to each point in time assessment, overnight, 7 days the price of the species is certainly more cost-effective, or even grab not, of course, Xiao Peng they will now have the first medium-term funds locked up.

And all this foreshadowing, that is, the first two years, with a number of small and medium banks as the backbone of the expansion of the table.

Waterfall is coming out. A joint-stock bank strategy researcher told the first financial journalists, from a number of bank off-balance sheet assets and liabilities, due to the existence of time mismatch, when the lever from the capital side, and the asset side “continued leverage” and strong Of the inertia, so the industry “shrink table” two pressure, this period will be mismatched.

It is also worth noting that “some banks have a long period of long-term bond assets Fukui, because the report is still in the ‘hold expired’ item, the outside can not be observed.” For such assets, banks also need funds Continued

“To talk about it, or just against the pressure, or asset quality problems.” “Debt shortage”, the funds from the tight, watching the financial management (mainly refers to the non-guaranteed financial management) is about to expire, South China an industry business developed a small bank head office management said that this is he will face the “chest broken stone.”

The following second section is from Capital Economics:

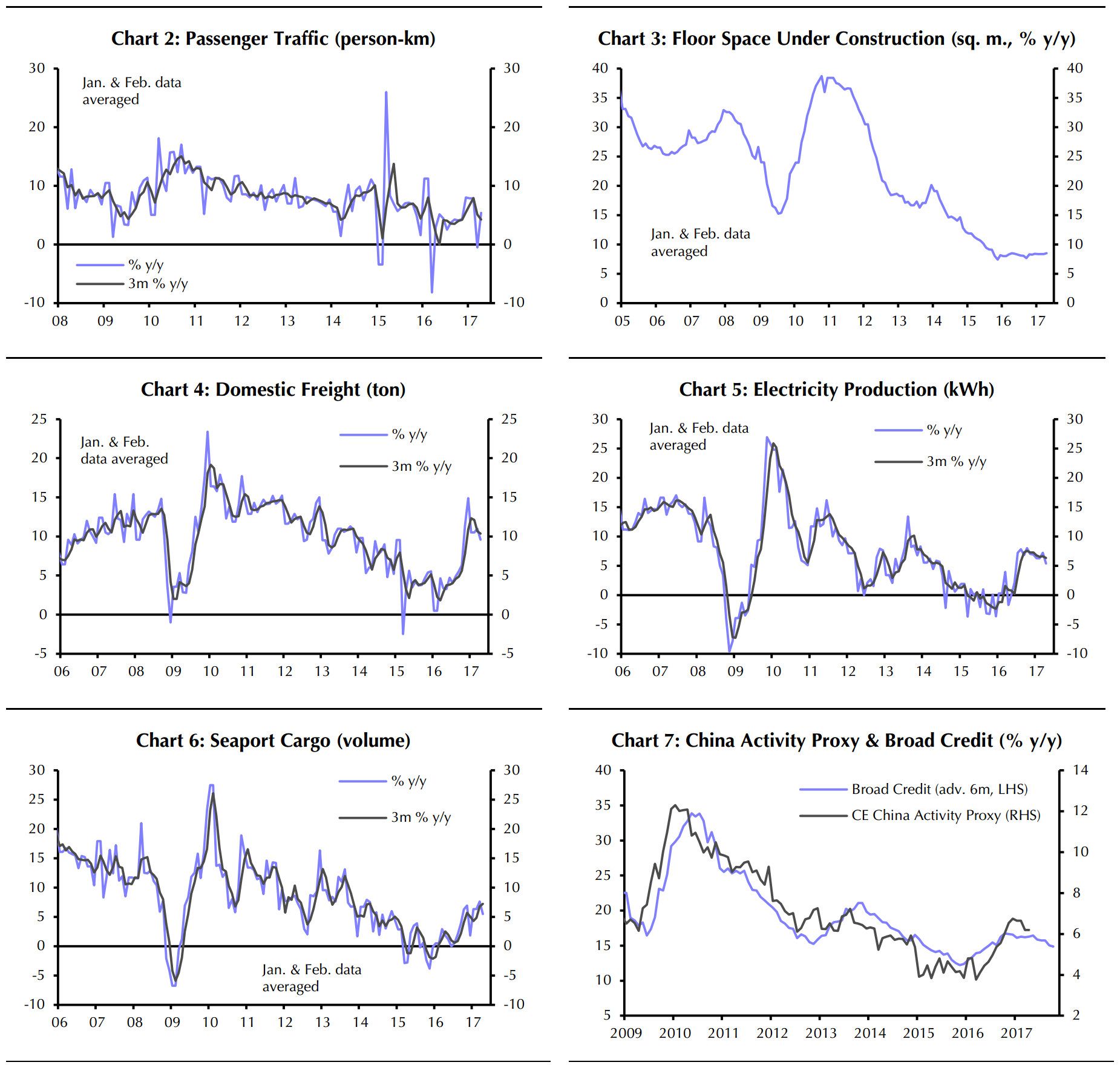

Our China Activity Proxy (CAP) shows growth stayed in April at the slowest pace in half a year. Looking ahead, as officials continue their efforts to rein in credit risks, we think activity will slow further in the quarters ahead.

The CAP is our attempt to track the pace of growth in China without relying on the official GDP figures. It is based on a set of low-profile indicators chosen to reflect activity across a wide section of the economy. (Details available on request.) Following a sharp rebound last year from a downturn that was never reflected in the official figures, the CAP and GDP were broadly in agreement in Q1. Our CAP shows the economy expanded by 6.5% y/y last quarter, close to the 6.9% on the GDP data.

But on a monthly basis, growth on our CAP peaked in December at 6.8% y/y. Our latest estimate shows output increased in April by 6.2%, unchanged from March and the slowest pace since last October. (See Chart 1 & Table overleaf.)

A closer look at the breakdown of the CAP data reveals that, although headline growth was stable last month, more of the proxy’s components slowed in April than in March. A seasonal rebound in passenger traffic (a measure of service sector activity covering business and leisure travel), which had slumped in March, was the only reason growth did not fall further last month. (See Chart 2.)

Property construction growth continued to hold broadly steady. (See Chart 3.) But all three of the CAP’s other components slowed in April. After picking up in March, growth in domestic freight volumes (a broad measure of economic activity) slowed last month to a six-month low.

Electricity output growth also fell in April to the slowest pace in nearly a year. (See Chart 4.) And the volume of cargo moving through China’s ports decelerated last month too, albeit only a little. (See Chart 5.)

Stepping back, at above 6%, growth in China remains strong and above what we estimate can be sustained over the medium-term (4.5-5%). So some further slowdown is probably inevitable. (See Chart 7.) What’s more, officials have been tightening monetary conditions and regulatory controls on non-bank credit since October in an effort to contain financial risks.

The property sector may also become a headwind to growth in the coming quarters. There are already signs that property sales are cooling due to recently imposed curbs on residential purchases. If this continues, developers may begin to slow the pace of construction.

Given their current focus on tackling financial risks, officials seem willing to tolerate a further slowdown in growth during the coming months provided that it remains gradual, as we expect. But they are likely to shift course on policy tightening if signs of a sharper slowdown emerge, particularly given the desire for stability ahead of the leadership transition scheduled for the Party Congress this autumn.

And this on the Moody’s downgrade also from Capital Economcs:

We are not surprised that the market reaction to Moody’s downgrade to its rating of Chinese sovereign debt has been limited. To recap, Moody’s downgraded China’s credit rating from Aa3 to A1 on Wednesday. There was no particular trigger for the move, other than ongoing concerns about the lack of reform momentum in the country’s financial markets. (See our China Economics Update, “Downgrade underlines fiscal risks in debt build-up”, published on Wednesday.)

Ultimately, as is often the case with such downgrades, the announcement contained little, if any, “news”: China’s struggles to bring down leverage, while maintaining rapid economic growth are well-documented, and Moody’s had lowered its outlook for China in March 2016.

Bond prices barely moved. Most are purchased overwhelmingly by domestic, state-owned banks, and held to maturity. There was therefore little chance of a spike in yields. And in any case, an A1 rating still puts China well within “investment grade” status.

Admittedly, excessive credit growth raises the risks of a government bailout out of the financial sector in the event of a severe downturn, which could plausibly add around 35%-pts to the debt ratio. But with only a tiny fraction of China’s debt denominated in dollars, there is little chance of an outright default: the People’s Bank of China (PBOC) can theoretically inflate away the debt. Moreover, while we expect a slowdown in GDP growth, we do not expect a “hard-landing”.

Equity markets dropped initially – the Shanghai Composite fell by about 1% on the news – but had recouped their losses by the end of trading. We have long argued that Chinese equities might face a downward correction once the economy starts to slow, and as the crackdown on leverage begins to bite. But there is little chance of a slump, as P/E ratios are nowhere near the levels reached just during the bubble in the first half of 2015 and not particularly high relative to levels seen at other times in the past. (See Chart 1.)

Finally, there appears to have been little pressure on the renminbi. While it might weaken a little this year, we then see it rising again to ¥6.8/$ in 2018, and ¥6.5/$ in 2019, as the dollar starts to come under pressure against the other “major” currencies, and as the authorities in China permit some appreciation of their currency in trade-weighted terms.

No change in my view. The cycle has peaked and that is going throw up curly questions for the banks pretty fast. We shall see where that leads us in time but for now China is going to slow.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.