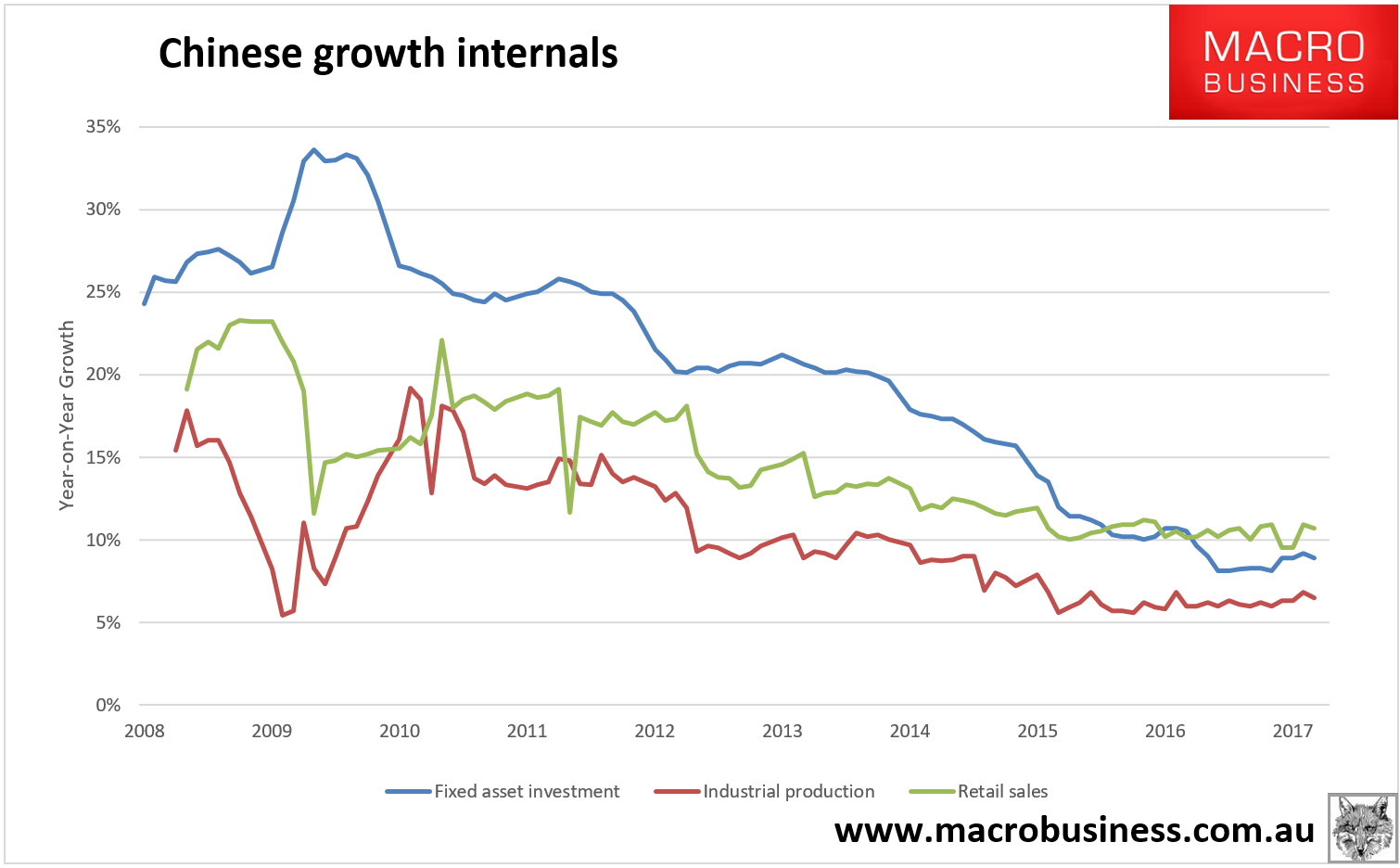

Right on cue, Chinese data is out and slowed more than most expected. Industrial production dropped materially to 6.5% from 7.6%. Fixed asset investment fell to 8.9% versus 9.2% and retail sales slowed from 10.9% to 10.7%:

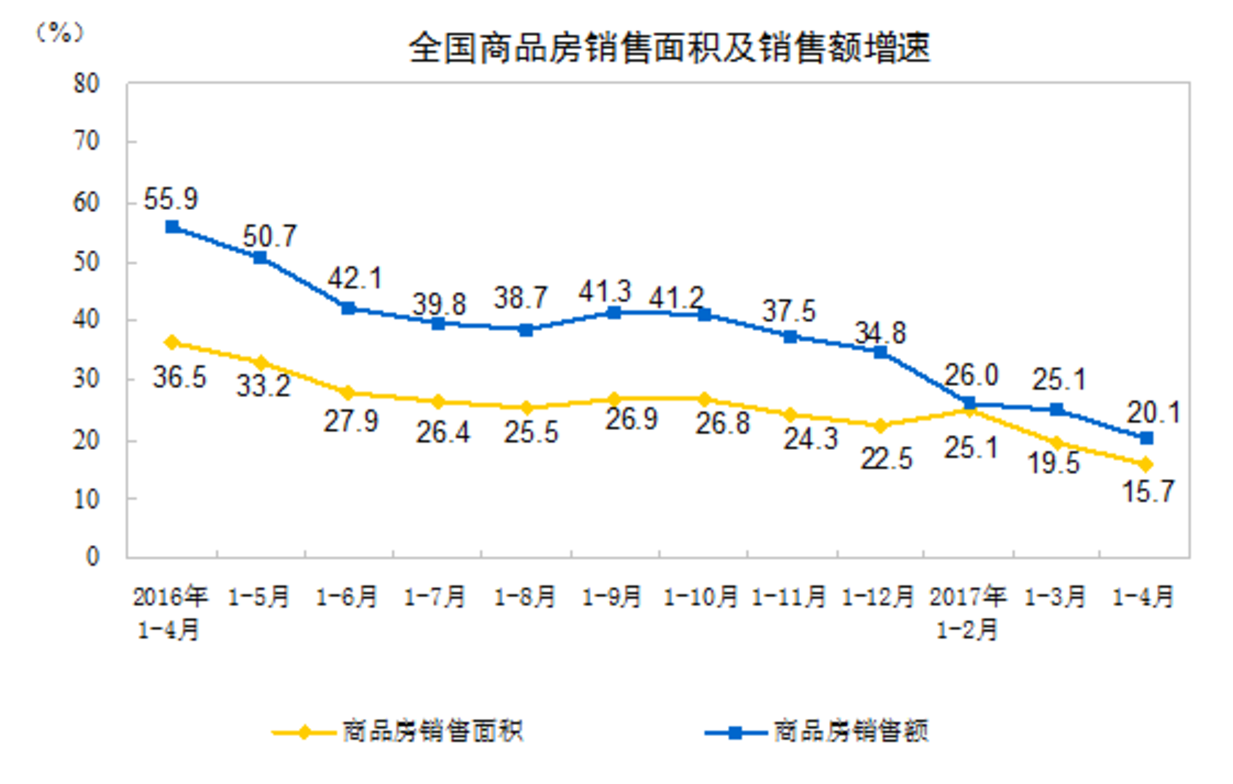

More Australia focused dimensions were mixed. Property sales by floor area are pulling back fast though still up 15.7%:

I expect this to fall to zero over the next few months.

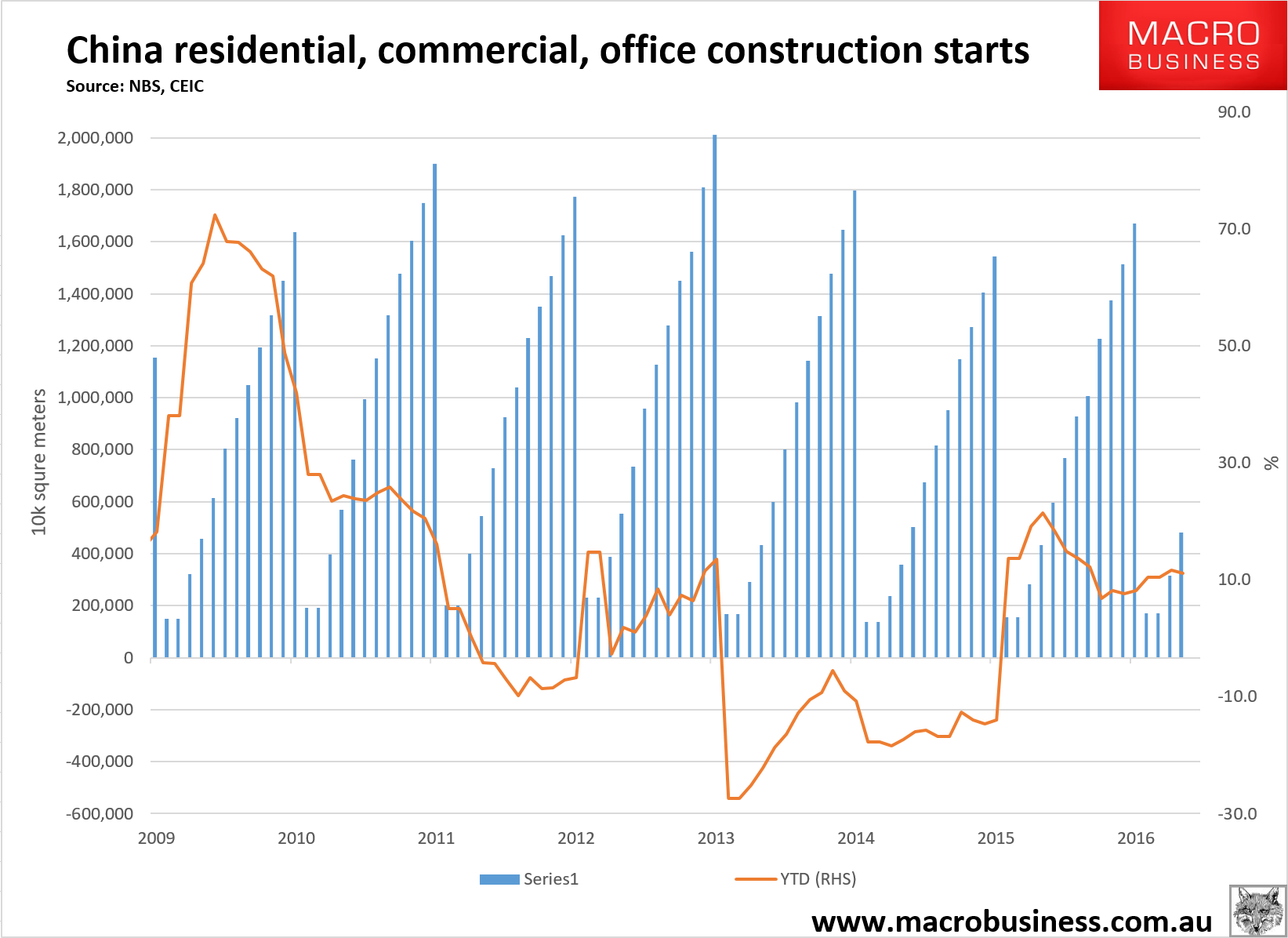

New construction starts growth fell to 11.1% from 11.6% and, likewise, I expect a march lower to zero over coming months:

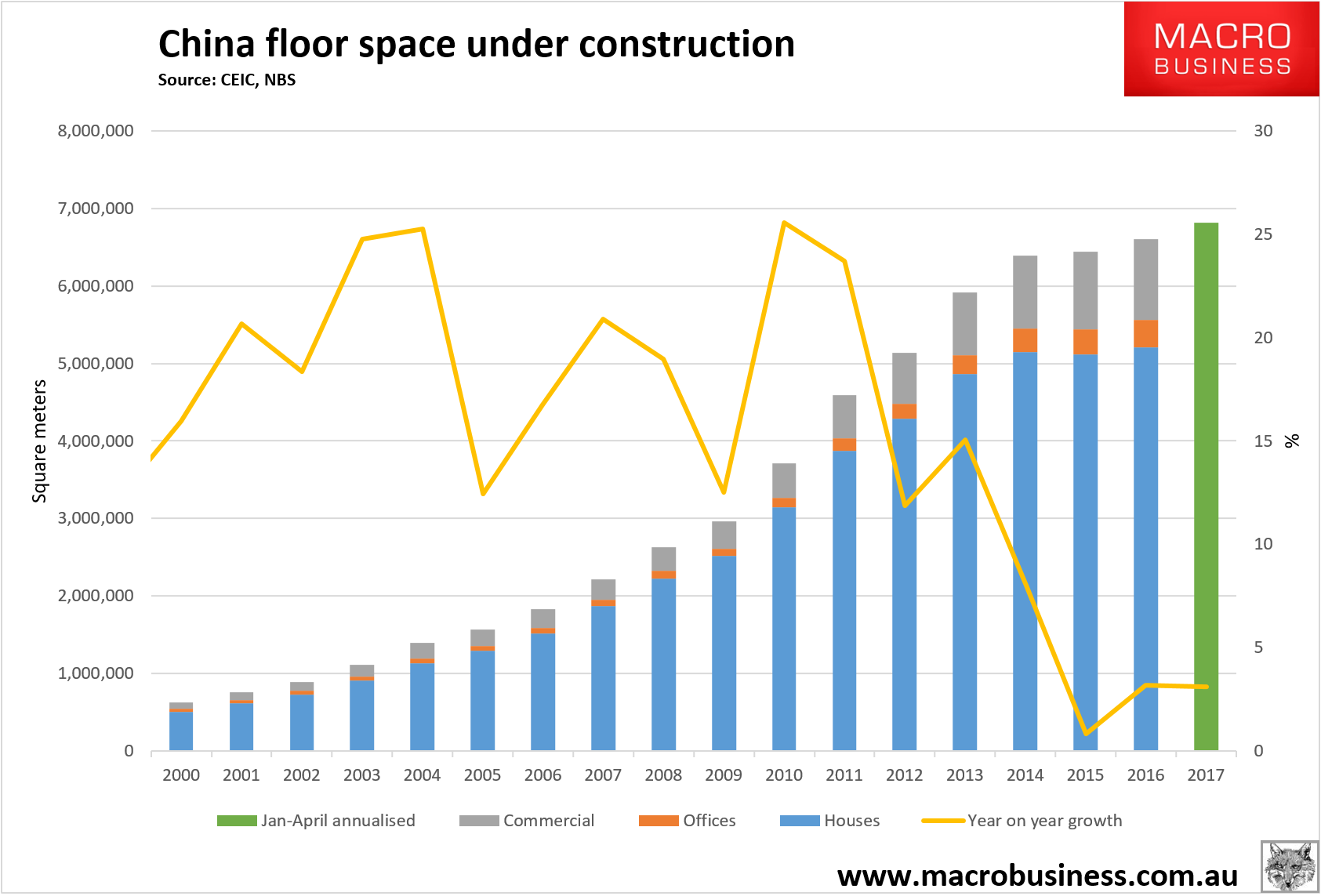

Total floor space under construction remained up 3.1% year to date but should also plateau by year end:

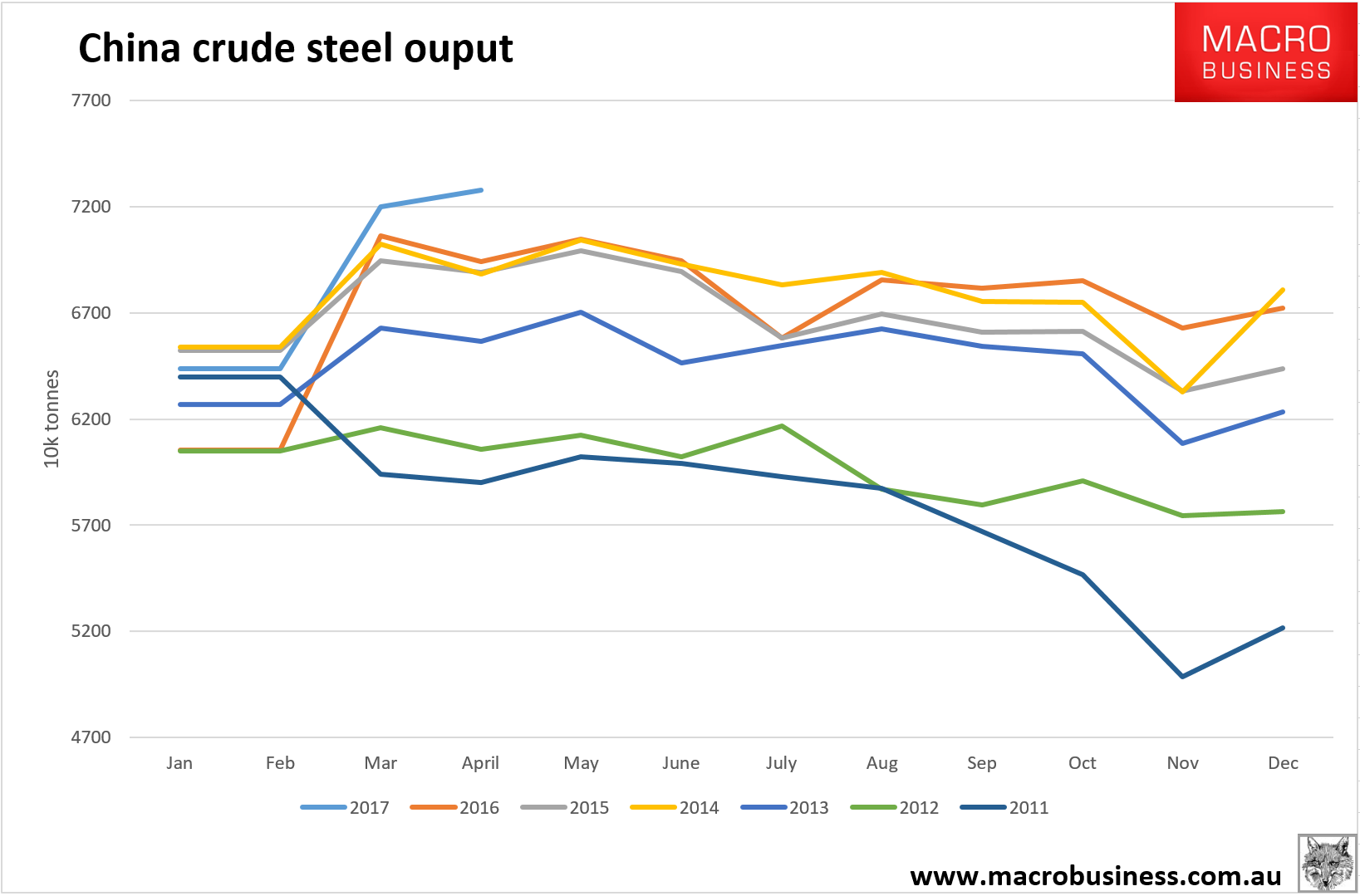

Steel output was absolutely off the hook at 72.78mt, easily an all-time record:

I reckon this is blast furnaces absorbing the illegal and now closed induction furnace output which was not recorded previously. It looks good but remember that the scrap formerly used by induction furnaces is now being used in blast furnaces as well as being exported so the net impact on iron ore across the region is zero.

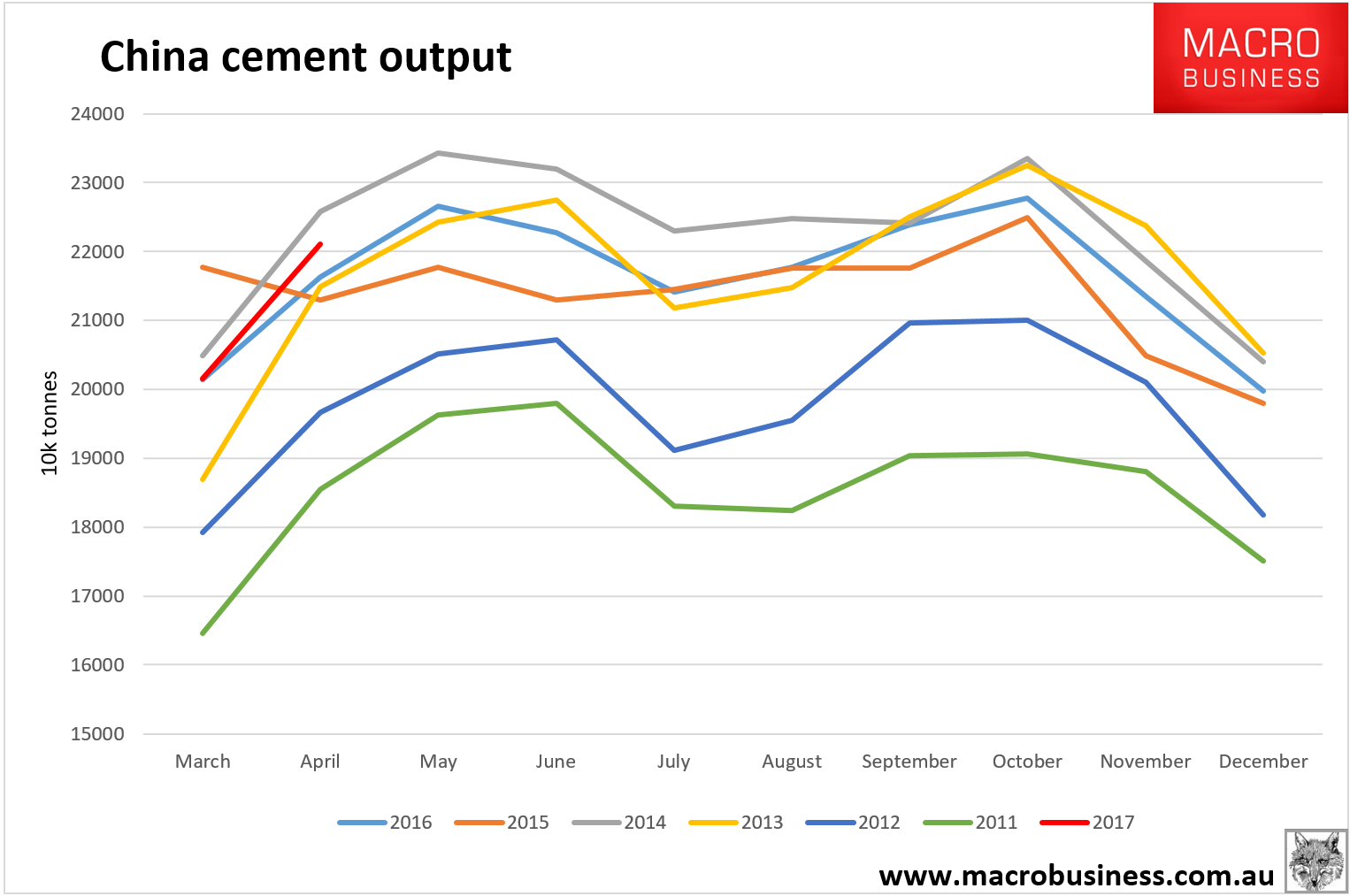

Finally, cement is a better guide to underlying demand and it shows strong activity but no records:

Still solid data but the China slowdown is here and will keep going all year. Capital Economic agrees:

The activity and spending data for April all came in below consensus expectations, continuing the recent trend of disappointing Chinese data.

Industrial production expanded 6.5% y/y in April, down from 7.6% in March. Most had expected a fall given the weak PMI readings for April, but the outturn was even weaker than anticipated (the Bloomberg median was 7.0%, our forecast was 7.2%). As usual, the underlying data on the output volumes of individual products was mixed. Surprisingly, growth in steel, cement and glass output all picked up, suggesting that construction activity is holding up for now. At the same time, however, electricity output growth declined markedly and the production of key consumer goods such as automobiles and mobile phones slowed, pointing to weaker activity in the broader manufacturing sector. Softer foreign demand appears to have played a role, with growth in industrial sales for exports declining from 12.9% y/y to 10.8%.

Investment growth also undershot consensus expectations. Fixed investment expanded 8.9% during the first four months of the year (Bloomberg 9.1%, CE 9.0%), down from 9.2% in Q1. This implies a slowdown from 9.4% in March to 8.3% last month. The breakdown is consistent with the picture painted by the industrial output volume data – the slowdown in fixed investment was concentrated in the manufacturing sector, with growth in infrastructure and property investment holding up well.

Finally, retail sales growth also slowed, from 10.9% to 10.7% (Bloomberg 10.8%, CE 10.5%). Higher vehicle taxes continued to weigh on car sales but sales of white goods and renovation materials also slowed, consistent with the recent deceleration in property sales.

The upshot is that slowing domestic consumption growth and softer external demand appear to have driven the slowdown in China at the start of Q2. For now at least, infrastructure and property investment are holding up, helping to stave off a sharper deceleration. But we doubt the current strength in these areas can be sustained given that policy is being tightened and the property market is starting to cool.