By Gareth Aird, Senior Economist at CBA:

Key Points:

- A second estimate of 2017/18 spending plans of around $85bn would imply no change to investment intentions compared to the first estimate.

- We expect the sixth estimate of 2016/17 spending plans to come in near $113bn.

- Our forecast is for the actual volume of QI capex to fall by 1.5% which would leave annual growth 12% lower.

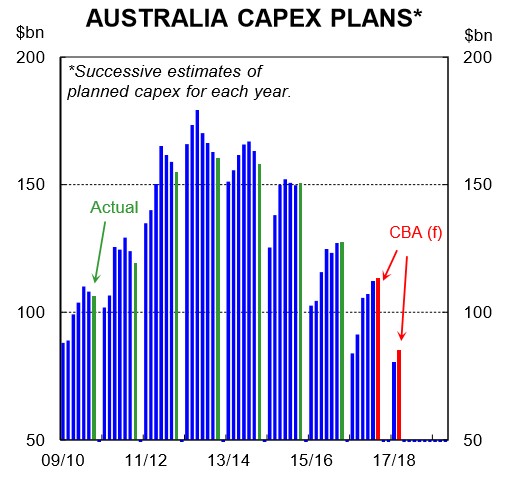

There are three key figures in next week’s capex survey: (i) QI 2017 actual spending; (ii) 2016/17 expectations (6th estimate); and (iii) 2017/18 expectations (2nd estimate). Markets will focus on the forward looking expenditure plans, particularly the second cut of 2017/18 spending intentions. As usual, we note that the capex survey only captures around 60% of business investment as per the national accounts. The survey excludes a number of large and important industries which include agriculture, health and education. We preview each component below.

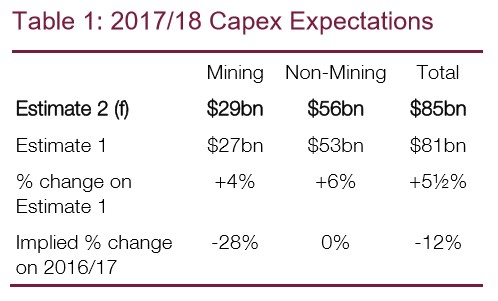

2017/18 expectations (2nd estimate) – see Table 1.

The first estimate of 2017/18 capex plans came in at $80.6bn. The figuring implied a fall in mining capex of around 28% when compared with 2015/16 and a broadly flat non-mining outcome.

Second estimates for spending plans can vary significantly from actual spending. A comparison of previous second estimates with actuals shows that non-mining firms will almost always underestimate their capex plans at both their first and second stabs. But the magnitude of the miss can vary greatly in any given year.

We consider a second estimate that comes in larger than $85bn as an upgrade on the first estimate. Less than $85bn would imply a downgrade (see Table 1). Policymakers will be looking, in particular, for a lift in non-mining spending intentions in 2017/18 (more than $56bn). We are yet to see a meaningful lift in non-mining private capex.

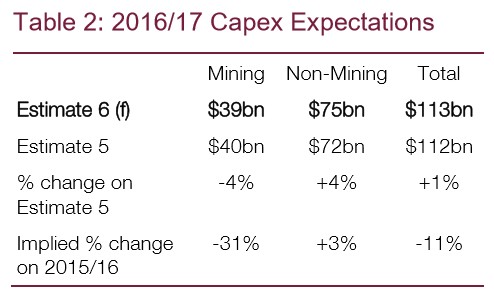

2016/17 expectations (6th estimate) – see Table 2.

The last reading from three months ago implied an 11% fall in nominal capex this financial year. The detail suggested a fall in mining capex of 31% and a modest but respectable 3% increase in non-mining investment.

The historical experience suggests that in the sixth estimate we need to see a slight downgrade to mining capex plans and a small upgrade to non-mining capex plans relative to the fifth estimate for spending intentions to remain broadly unchanged. We consider a sixth estimate that comes in larger than $113bn as an upgrade on the fifth estimate. Less than $113bn is a downgrade.

QI 2016 actual

We expect the actual volume of QI capex to decline by 1.5%. Such an outcome would leave annual growth 12.0% lower. The actual spending data will help us to firm our estimates of QI GDP growth. At this stage a soft print is likely.

Risks

The improvement in the NAB Business Survey coupled with strong employment reports over the past two months suggest the risk to our call on 2017/18 nonmining investment plans is to the upside. Risks to our mining call look evenly balanced.