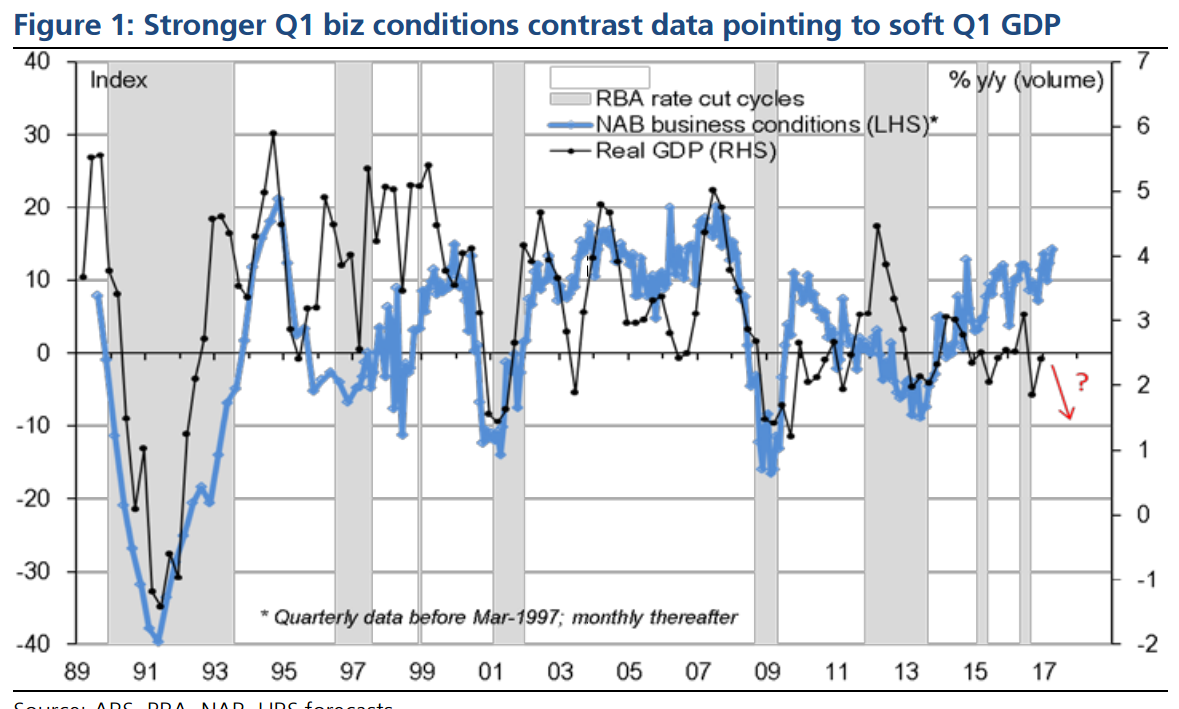

How soft could Q1 GDP growth be? Since around mid last year, we’ve been relatively bullish on a 2017 pick-up in Aussie growth to a 3-handle in 2H17 (from ~2¼% y/y now), as the headwinds of falling commodities, mining capex and fiscal drag fade. This is a view shared by the RBA, and one that has helped deliver steady rates since August last year.

However, our growth optimism has been increasingly tempered by our forecast housing correction from later this year that is seen directly dragging around ½%pt off growth through 2018 (& another ¼%pt indirectly via the consumer), returning growth back to 2½% y/y by end-18, only a little above its current pace. Historically soft wages growth and elevated consumer debt strengthens the likely feedback of housing via both slower household goods purchases as well as the fading of an arguably modest – but still evident – wealth effect from recent house price gains.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.