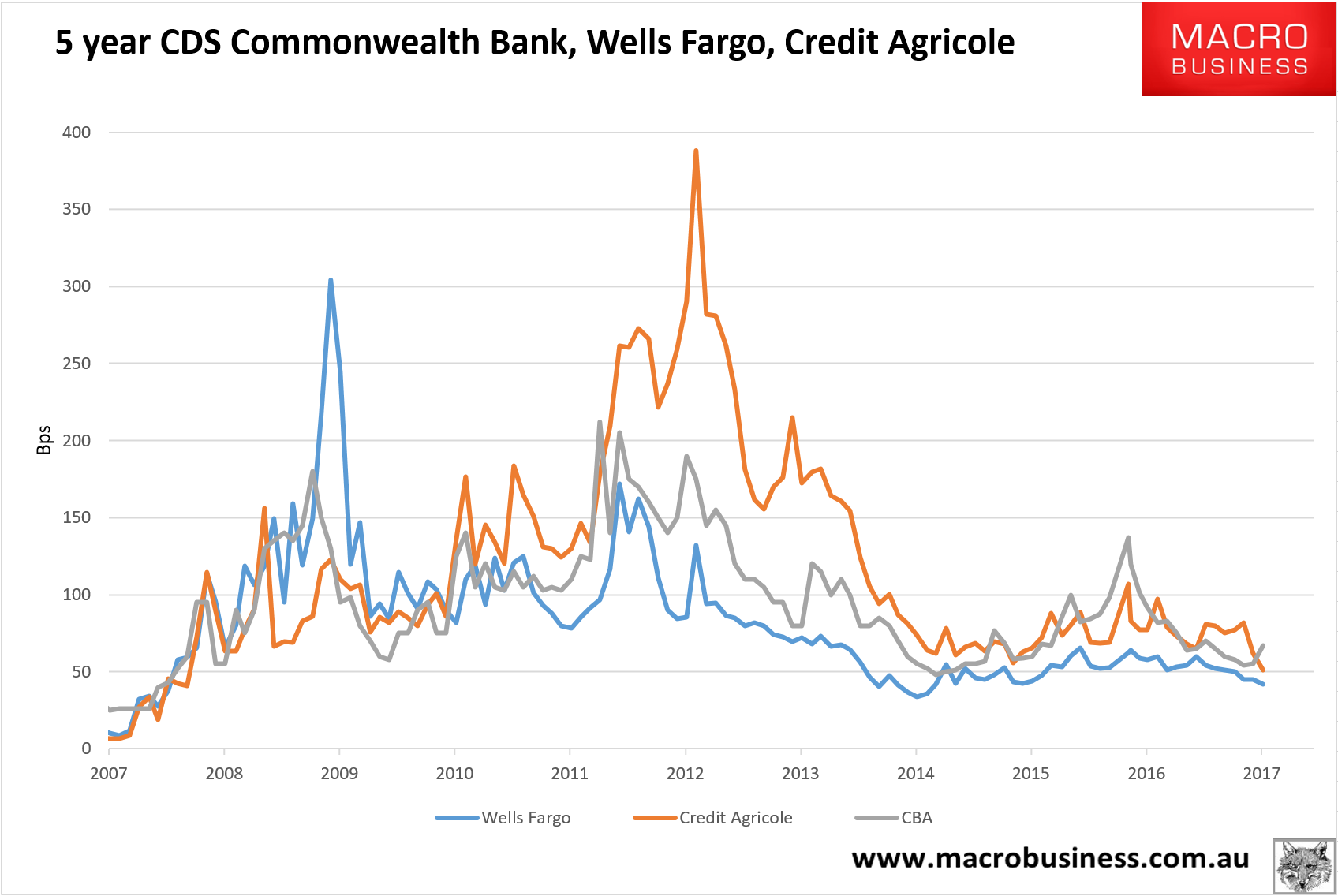

Aussie bank funding costs break higher

While the fake debate over this guarantee or that levy persists, one thing that is happening for real is that Aussie bank funding costs appear to have passed the low point of the cycle and are climbing. The outright low for CBA CDS of the recent cycle was just above 50bps in February this year as the terms of trade rebound soared. As of Friday that price had risen 32% to 66bps, unusually, even as European and US costs of funds keeps falling:

The trigger, oddly enough, was the S&P downgrade of smaller banks, which did not include CBA but appears to be costing it anyway, no doubt owing to the perception of rising bad loans losses as S&P points a pin at the bubble. The now collapsing terms of trade can’t be helping either given they will lead directly to a sovereign and major bank downgrade soon as the Budget falls apart.

We remain a long way from panic stations at these levels with prices needing to nearly double to cause real systemic dyspepsia, first for the RMBS market at around 120bps and then majors at more like 150bps.

The full text of this article is available to MacroBusiness subscribers