By Gareth Aird, Senior Economist at CBA

Key Points:

- Employment rose by a solid 37.4k in April following a massive lift of 60.0k in March.

- The unemployment rate dropped by 0.2ppts to 5.7% and the participation rate held firm at 64.8%.

- Hours worked fell in April and the data looks at odds with the reported gains in employment over the past two months.

Once again the ABS has published an employment report that has left us scratching our heads. Employment is reported to have lifted by a very strong 37.4k in April (consensus +5k) after increasing by a massive 60.0k in March. To put these numbers in perspective, it’s the equivalent of a 1.2 million increase in US non-farm payrolls over two months! To further add to our concerns over the data, total hours worked is reported to have fallen by 0.3% in April and is down by 0.1% over the past two months despite employment having risen by 97.4k. These are the official labour force statistics, however, so we go through the key components in the usual way.

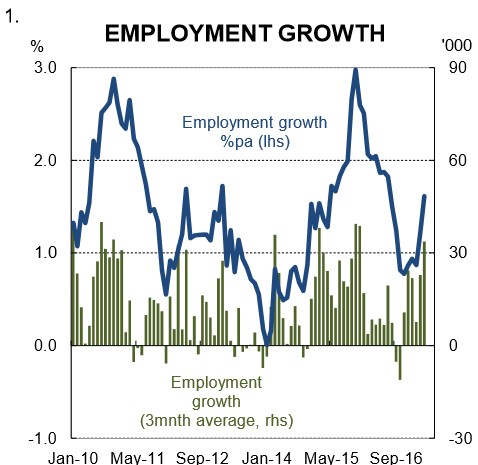

Employment: The trend pace of jobs growth has accelerated further on today’s figures. The average of the last three monthly prints suggests that net job creation is a solid 34k a month (chart 1). Annual employment growth is running at 1.6%, a touch above population growth (1.5%). Full-time jobs fell by 11.6k after a reported massive 73.9k lift in March. Part-time employment rose by 49.0k.

Unemployment and participation: The unemployment rate dropped by 0.2ppts to 5.7%. The trend unemployment rate, which we consider the best barometer of the jobless pulse, held flat after inching higher in late 2016 and early 2017 (chart 2). The recent movements, however, are very small and the trend unemployment rate has basically moved in a narrow 0.1ppt range over the past year.

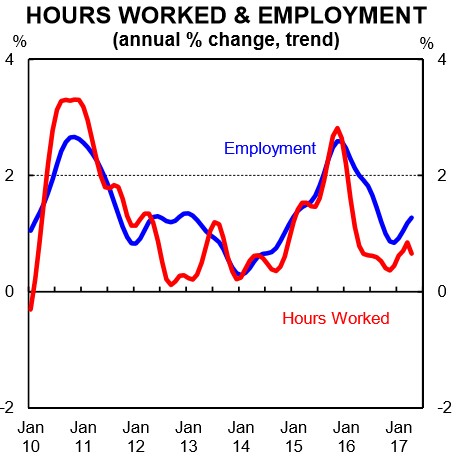

Hours worked: Very much like last month, it’s hard to make sense of the hours worked figures. These numbers are usually volatile, but they look odd again today. It was reported that hours worked fell by 0.3% in April despite employment rising by 37.4k. And in March total hours work lifted by just 0.2% despite the huge lift in employment that was driven completely by full-time jobs. In trend terms, hours worked is up by just 0.7% through the year while trend employment growth is running at 1.3% (chart 3).

States: The data shows that job gains were spread across Australia’s four biggest states in April: Vic (+20.3k), WA (+14.4k), QLD (+12.1k) and NSW (+9.7k). In annual terms Vic (3.8%pa) leads the pack, helped along by very strong population growth. The unemployment rate fell by 0.3ppts in NSW to 4.7% and by 0.6ppts to 5.9% in WA. It was unchanged in Vic (6.1%) and QLD (6.3%).

Implications: The April RBA Board Minutes, published on Tuesday, contained a detailed discussion on recent trends in the labour market. In particular, a few paragraphs were devoted to the Board’s assessment of the composition of employment growth. Members concluded that, “the distinction between full-time and part-time work had become less important in assessing labour market conditions.” We beg to differ. And as luck would have it, we published a detailed research piece back in August 2016 which explains why.

It is true that the distinction between full-time and part-time employment is arbitrary and the line in the sand is drawn at 35hrs. But it is no coincidence that the upward trend in underemployment over the past few years has coincided with an acceleration in the trend towards part-time employment.

There is often a perception that full-time jobs are “good” and part-time “ok” when it comes to the employment data. But in our view, both full-time and part-time jobs are equally as “good”, provided that workers in part-time employment don’t want to work full-time. If a worker chooses part-time employment they are not underutilised – they are simply displaying a preference to work fewer than 35 hours a week. However, growth in part-time employment, rather than full-time work, becomes a problem (and indeed undesirable) when there is growth in the number of workers who are not working as much as they would like. This is captured in the underemployment rate which is at its highest level on record.

The monetary policy dial is unaltered by today’s numbers. The cash rate remains on hold unless the labour market falters or there is a material slowing of activity in the housing market (i.e. credit and dwelling price growth).