The ABS last week released dwelling construction data for the December quarter of 2016, which has once again allowed me to track how quarterly approvals, commencements and completions are tracking against population growth across the major markets.

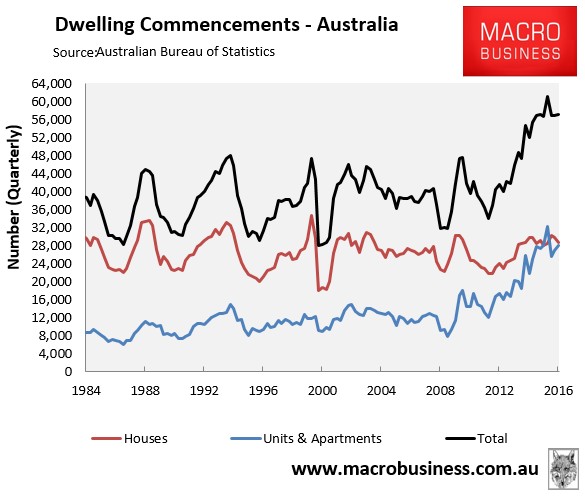

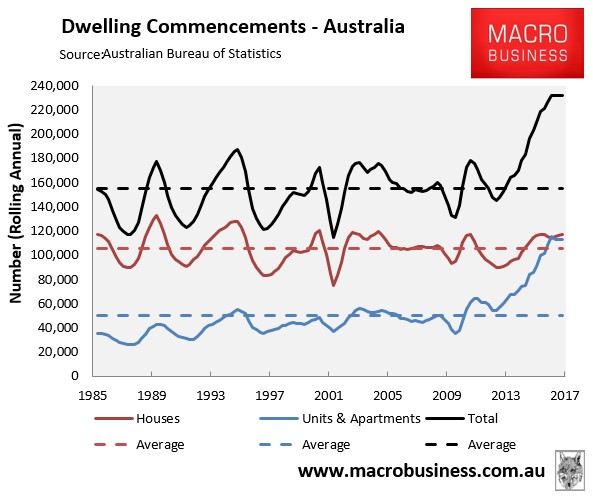

But first, the number of dwelling commencements rose by a seasonally-adjusted 0.3% over the December quarter and were up just 0.8% over the year. Detached house commencements fell by 3.4% over the quarter but were up by 2.5% over the year, whereas unit commencements rose by 3.9% over the quarter and were up by 2.4% over the year (see below charts).

As shown above, annual house commencements ran moderately above the long-term average in the December, whereas apartment commencements continue to boom.

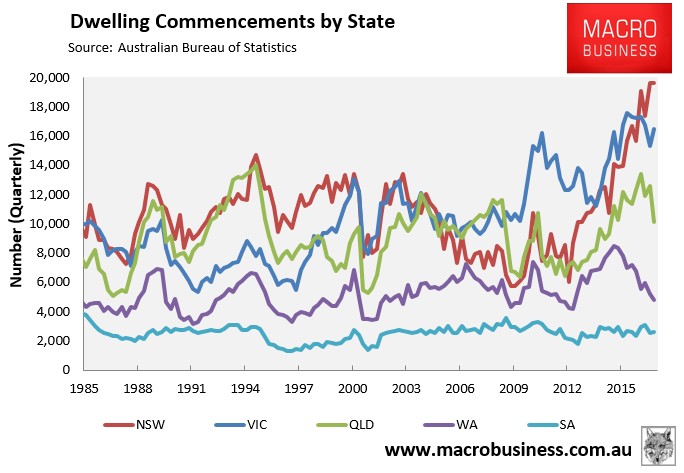

At the state level, the quarterly rise in commencements was driven by VIC, where apartment construction surged by 24.1% over the quarter (see next chart).

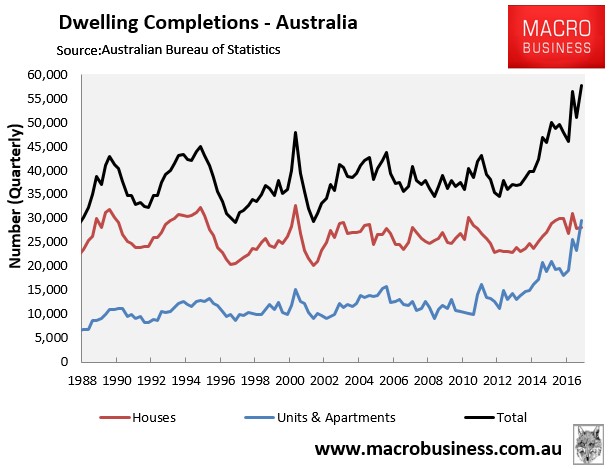

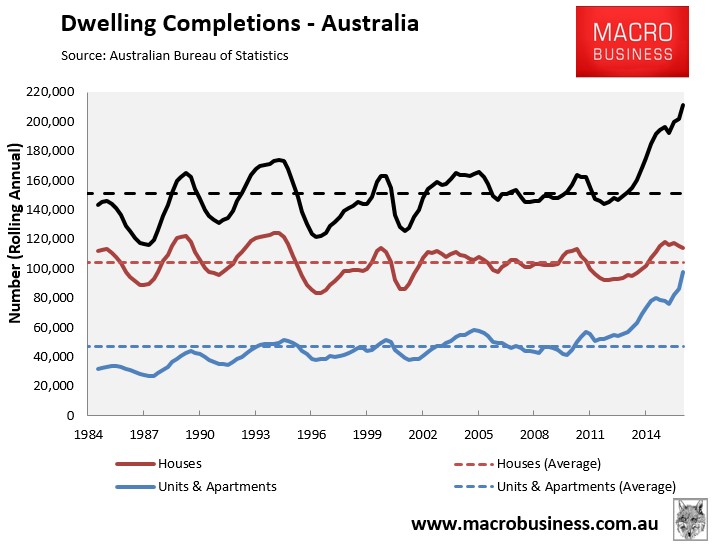

Actual dwelling completions (which lag commencements) surged over the December quarter, jumping by 12.8% to be up by 20.1% over the year. Detached house completions rose by just 0.7% over the quarter but were down 6.2% over the year, whereas apartment completions surged by 27.3% over the quarter to be up by 64.0% over the year (see below charts).

As shown above, apartment completions overtook house completions for the first time ever in the December quarter – a sign of the times, with the population ponzi and ridiculously expensive housing forcing Australians to live in highrise shoe boxes!

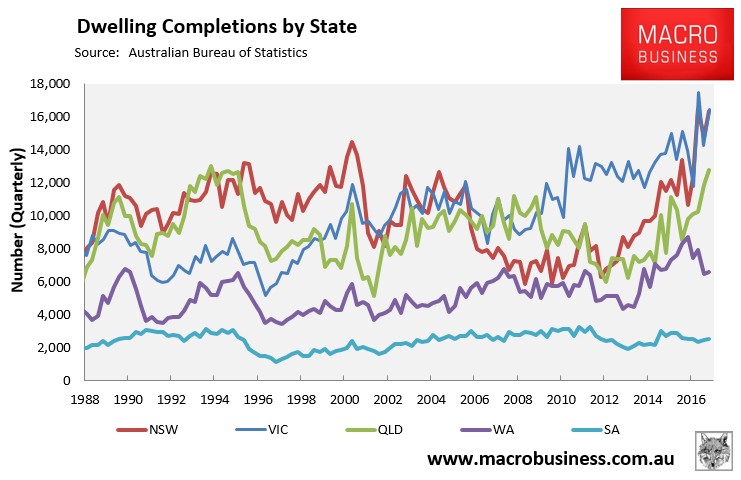

At the state level, the overall quarterly surge in completions was driven overwhelmingly by apartments in VIC (+35.7%), NSW (+14.2%), QLD (+12.5%) and WA (+21.1%):

The below charts track the following, which are based on the latest available quarterly data:

- Dwelling approvals to December 2016;

- Dwelling commencements to December 2016;

- Dwelling completions to December 2016; and

- Population growth to September 2016.

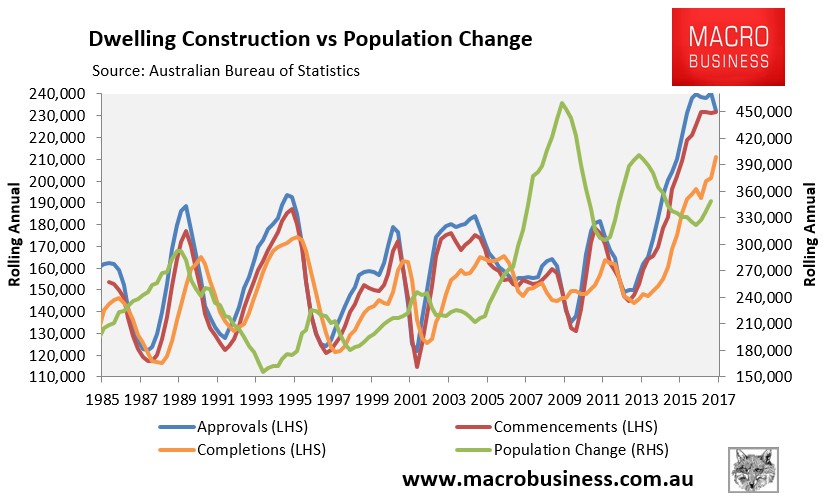

First, the national picture shows that dwelling approvals have fallen from recent all-time highs, whereas commencements look to have peaked after playing catch-up. Completions surged recently as they have played catch-up with commencements, but they still remain way behind, thus suggesting there is still a large pipeline of dwellings currently in the construction phase. However, population growth has accelerated and is now well above the GFC low:

Given that approvals and commencements are still close to record highs, and a large gap still exists between them and completions, the overall construction pipeline remains huge and dwelling construction nationally will likely remain at boom-time levels for the rest of this year. But the acceleration in population growth mitigates the potential oversupply risks.

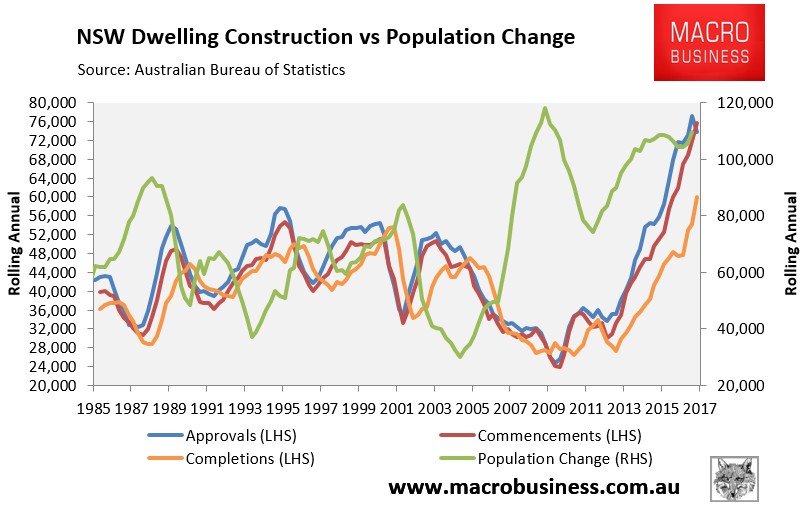

Next is NSW, where after a decade of sluggish construction, approvals and commencements have lifted to unprecedented levels, although approvals are now just past their peak. Completions have also surged but remain way below commencements, thus suggesting a huge construction pipeline still exists. But population growth is picking-up from an already elevated level:

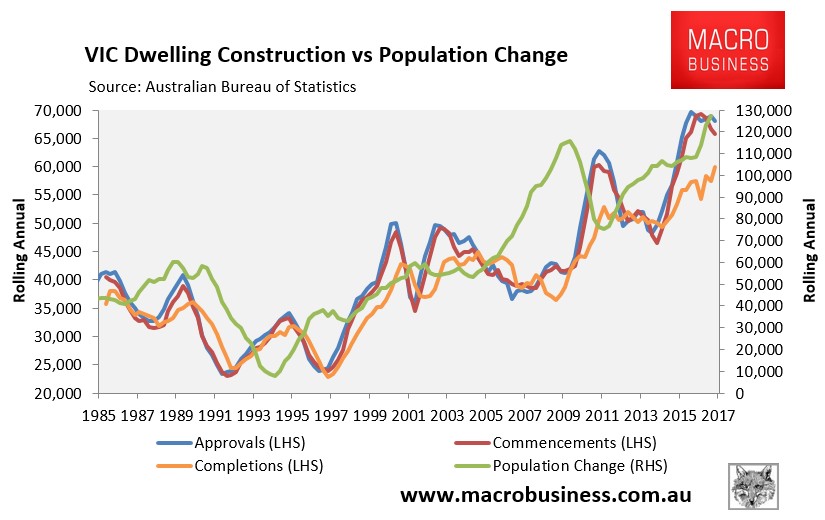

In VIC, which has long been the construction leader, dwelling approvals and commencements are both levitating near historically high levels; although the latter retraced in the latest quarter. Completions are yet to play catch-up with commencements, again suggesting a large construction pipeline exists. Population growth, however, has rocketed to easily the highest level on record:

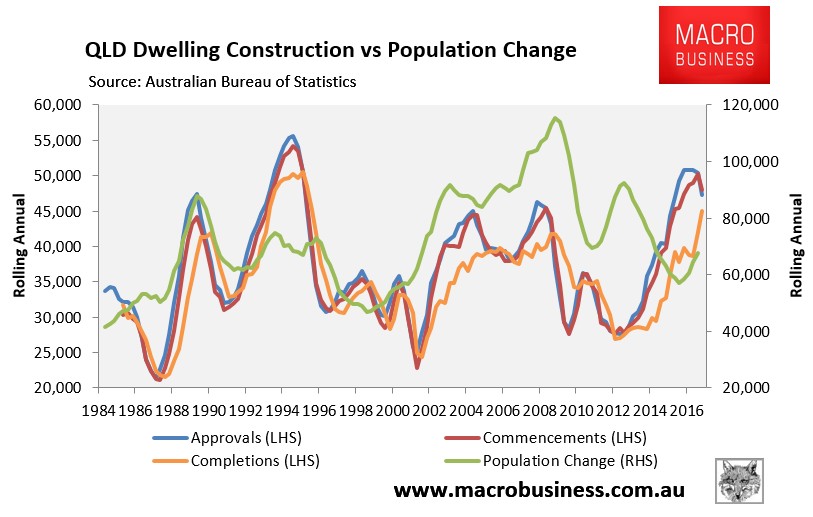

QLD’s apartment glut is coming online now. Although dwelling approvals have retraced significantly from recent highs (commencements to follow), completions are catching up fast. By contrast, population growth is running at relatively low levels (compared to the mid-2000s), despite turning up recently:

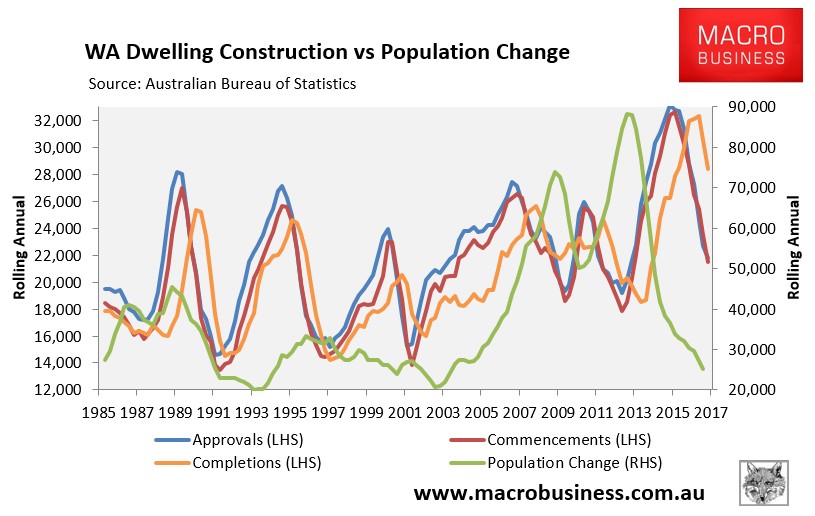

The construction cycle in WA continues to unwind abruptly. Approvals and commencements are way past their peak, whereas completions have also begun falling from record levels. Meanwhile, population growth continues to crash through the floor, suggesting the supply-demand imbalance in Western Australia will continue to get worse and remain in oversupply for a long time yet:

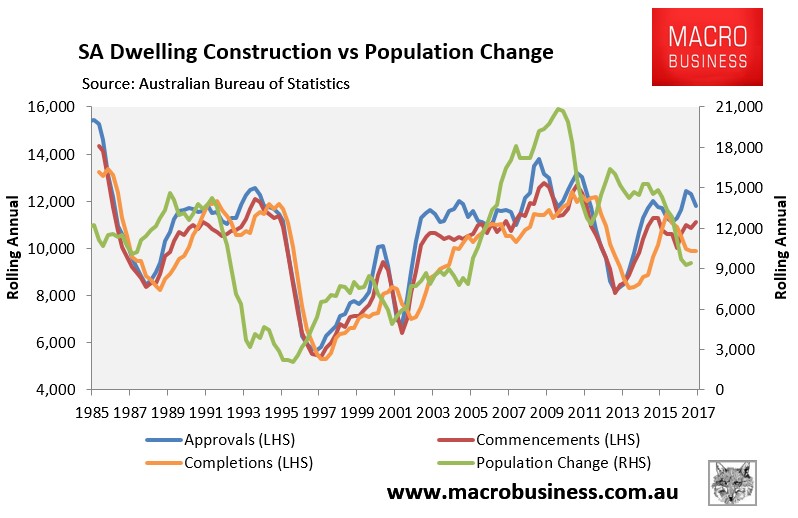

While SA’s housing market remains reasonably balanced at present, dwelling approvals and commencements have picked-up over recent quarters as population growth has crashed, whereas dwelling completions have slumped. This suggests an oversupply could develop in the near future, assuming completions play catch-up with commencements:

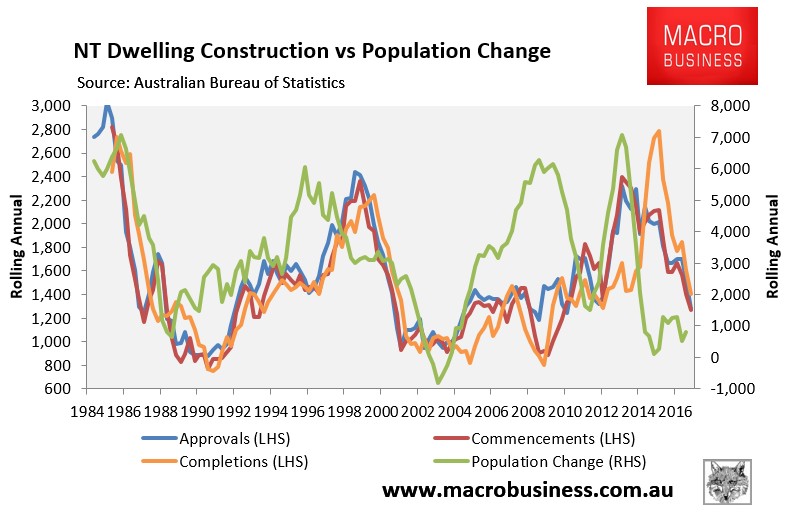

After a big increase in supply relative to population growth, construction continues to unwind briskly in the NT. Supply has fallen back to earth although population growth continues to bounce around close to zero. Overall, dwelling additions continue to easily outnumber population additions, suggesting any oversupply will worsen:

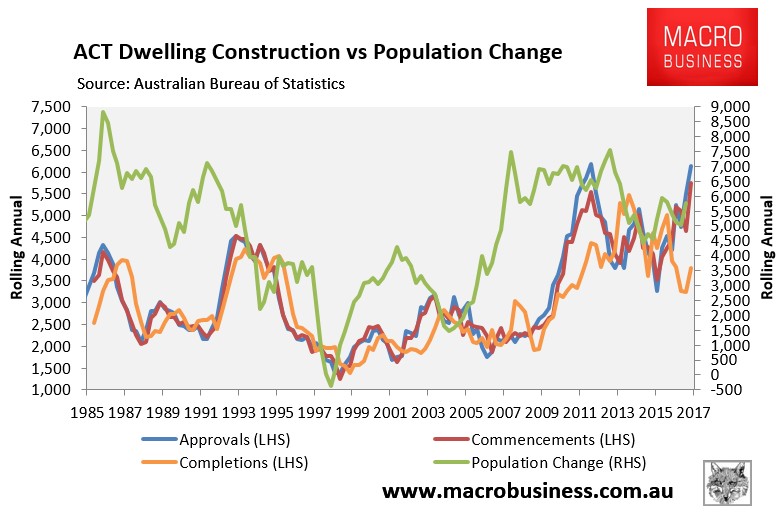

Finally, in the ACT, population growth is running just above the long-term average. However, dwelling construction is looking to accelerate with approvals commencements rocketing and completions lagging way behind:

To summarise, there are still large gaps between dwelling approvals/commencements and completions nationally, driven by the major east coast markets of NSW and VIC, whereas QLD’s completions are now catching up. In the two major markets, in particular, there is a huge pipeline of projects that have been commenced but are yet to be completed.

However, VIC (Melbourne) has also experienced a big surge in population growth, whereas NSW and QLD have also experienced meaningful increases, which together should help to mitigate any pending apartment oversupply.

Elsewhere, housing gluts appear to be developing across WA, the NT, SA, and the ACT, although they are at different stages of the cycle.

With approvals nationally only recently retracing from record levels, and the long (2+ year) lag time between highrise approvals and completions, the dwelling construction boom will likely run hot for the rest of this year and possibly into early 2018.

unconventionaleconomist@hotmail.com